Energy Markets Stabilize As Diesel Rallies And Inventories Tighten

Diesel futures are leading the energy complex higher for a 2nd straight day, wiping out Tuesday’s big losses, despite new claims that the U.S. Navy now controls traffic through the Strait of Hormuz and Presidential musings that the war will soon be over. Equity markets seem more optimistic about the outcome, creating a rare up day for both stocks and petroleum complex so far.

Yesterday’s DOE report helped give another boost to refined products after selling earlier in the week as more inventory draws, particularly on the East Coast while the ongoing SPR releases help to keep the country’s oil stocks in healthy territory. See below for more detail.

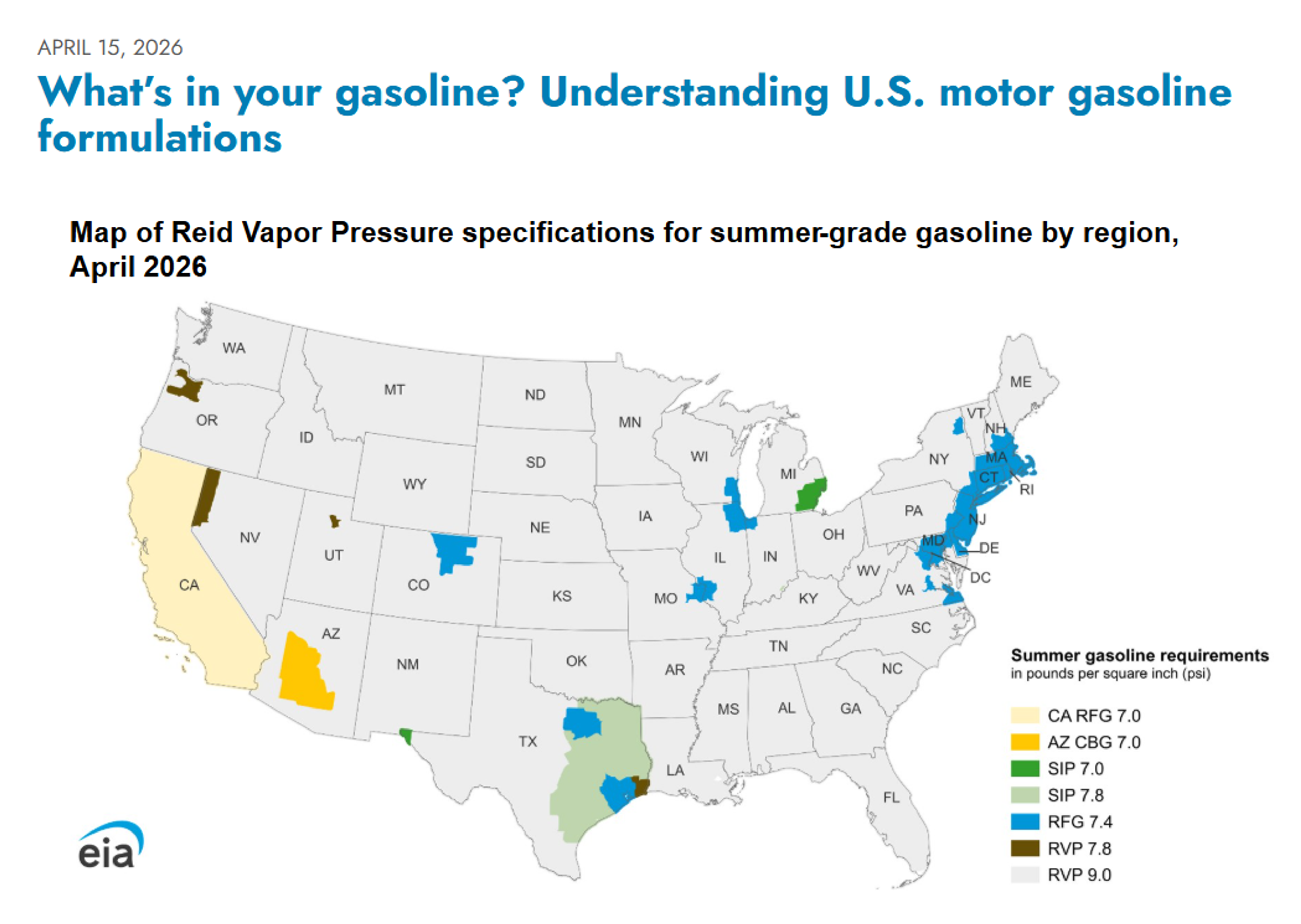

The EIA took a deep dive into RVP and boutique gasoline grades Wednesday, highlighting the nuances that almost no-one outside the industry understands, and many even in the industry still struggle to keep up with. Meanwhile, the EPA continues to do its best to make most of these seasonal grades irrelevant this year with its push to a 10lb RVP standard and waivers on boutique grades until the war disruptions [and the mid-term elections] end although most states remain reluctant to jump on the bandwagon.

The San Francisco spot market for traditional diesel continues to struggle with a complete lack of any bids or offers since April 1. Due to the lack of activity, pricing agencies have left their basis differentials unchanged for more than 2 weeks at 75-80 cent premiums, even though neighboring markets, Renewable Diesel and Bay-area rack prices have all dropped sharply during the month. If you’re not a basis connoisseur, just know that this means some consumers in the region are paying somewhere between 30-50 cents too much for diesel because the old spot index of choice for many deals has now apparently become obsolete with only 2 sellers left in the region and most supply converting to renewables, but the pricing agencies haven’t yet caught up to that reality. The rack vs spot chart below highlights this phenomenon, with diesel posters at the terminal racks pricing nearly 20 cents less than the obsolete spot market posting.

We saw a similar slow-to-react response from one of these agencies last year when CARB was forced to delay their LCFS rule changes, but the agency continued to post prices that reflected the higher level for months and chose not to issue a correction.

Ukraine continued its attacks on Russian energy assets overnight, striking the 240mb/day Tuapse oil refinery, and nearby fuel export terminal in on the Black sea.

Notes from the DOE’s weekly status report.

Crude stocks dropped after a 7-week stretch of builds as the SPR release nearly doubled week over week while imports and exports hit their respective low and high levels of the year, although a large positive increase in the adjustment limited the headline draw. US refinery runs slowed for the third week in a row, declining across all PADDs except 1 with the largest coming out of PADD 2. Alongside lower run rates, capacity increased everywhere but PADD 5 (with the Midwest hitting a record high), slightly exaggerating the impact on utilization and sending it back below 90%.

Diesel stocks shed 3 million barrels across PADDs 1-3 despite lower demand, although exports remain elevated. PADD 1’s drop was driven by a large decline in PADD 1C but inventories, while on the low end, are still a couple million barrels ahead of year ago levels. PADD 3 is also above the same week last year but fell below average for the first time since the end of last summer. PADD 4 is the only region still holding above average, but it only makes up about 4% of total U.S. inventories which are now about 6 million barrels shy of their 5-year average.

Gasoline stocks dropped for the 9th straight week, dipping below 2025 levels for the first time all year. Demand ticked up to a seasonal high while imports plummeted with PADD 5 slowing gasoline arrivals as PADD 1 fell to a 5-year low. Although West Coast imports dropped significantly, they’re still at a seasonal high and helped push inventories up after bottoming out about a month ago. All other PADDs drew, led by a huge decline in PADD 3 to join diesel at below average for the first time this year. Ethanol stocks increased on the year’s largest week to week decline in exports as production holds steady at 5-year highs.

Latest Posts

Gasoline Surges As Global Energy Risks Return

Week 28 - US DOE Inventory Recap

Oil Extends War Premium Gains Amid Ongoing US-Iran Hostilities

Energy Rally Gains Steam As Global Supply Chain Pressures Mount

Energy Markets End A Wild Week With More Questions Than Answers

Middle East Tensions And Russian Export Ban Rock Energy Markets

Social Media

News & Views

View All

Gasoline Surges As Global Energy Risks Return

Week 28 - US DOE Inventory Recap