Oil Slides Toward Historic Monthly Loss Amid Supply Uncertainty

Reversal Thursday has been confirmed with the resumption of selling in energy futures so far this morning. WTI futures are leading the way lower, exchanging hands 1.5% lower in pre-market trading, designating yesterday’s buying action as a mere technical quip rather than a shift in fundamental expectation. Gasoline and diesel futures are sagging in sympathy, trading lower by less than 1% to start the day.

Oil prices are on track for their biggest monthly decline since March 2020, as confidence grows that the U.S. and Iran are close to a 60-day agreement that would include reopening the Strait of Hormuz within the first 30 days. Because nothing can ever be simple, it was made abundantly clear that the agreement has, so far, not been approved by the White House.

Today is the expiration day for June RBOB and ULSD futures, with the July contracts trading ‘only’ 9 cents lower for RBOB and 6.5 cents lower for ULSD so far today. Gulf Coast, Group 3, Chicago, and the trio of West Coast physical markets have already rolled to trade against the July contract, but for NYHB market participants, still trading against June, be sure to pay attention to the July price action today for indications on where tomorrow’s rack prices will be.

Lukoil’s Volgograd refinery was struck and set ablaze this morning, according to and EnergyNewsToday report. The 300mbd plant wasn’t likely throughputting at its nameplate capacity, seeing at it was just hit in February by a similar strike, and again a short 16 days ago.

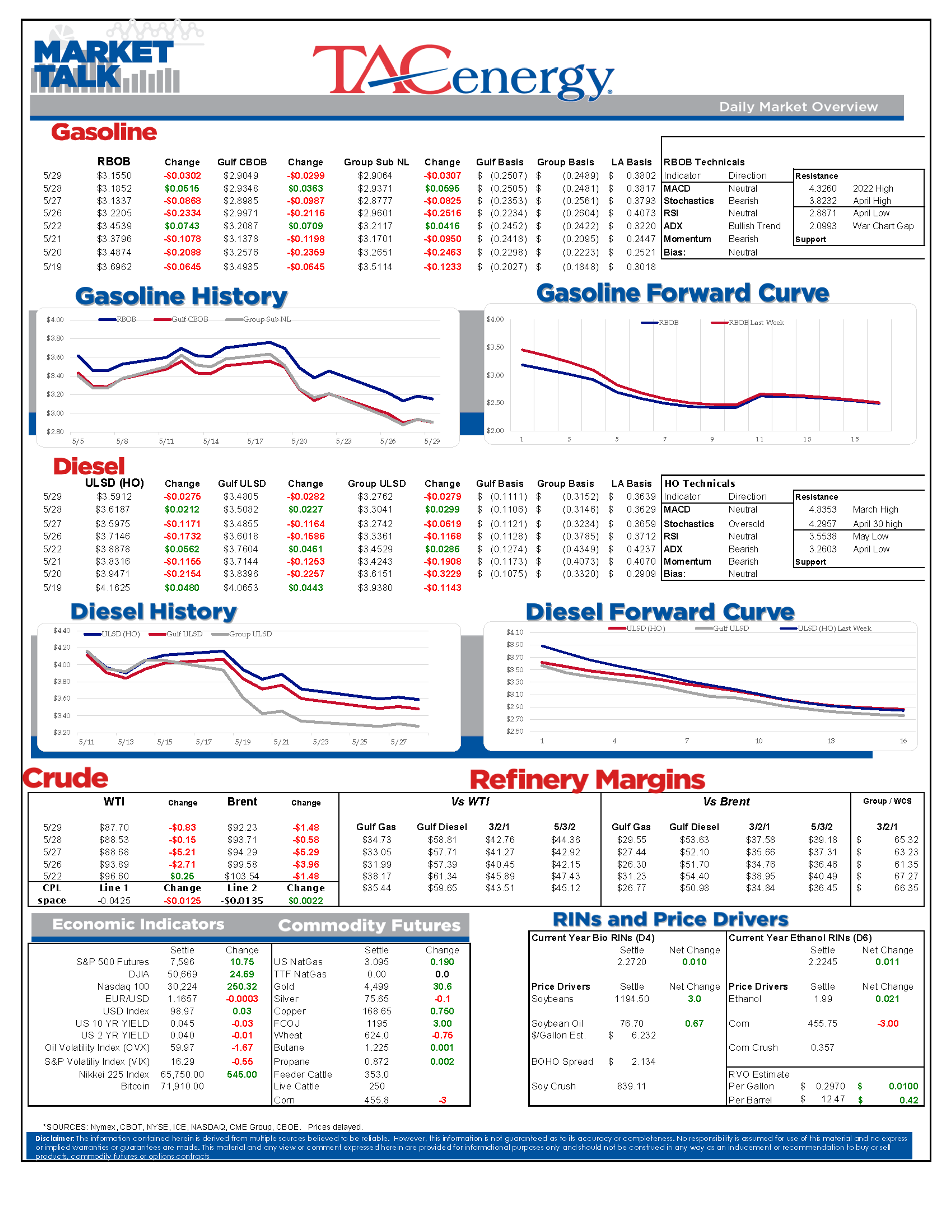

DOE charts attached, notes below:

Crude stocks declined as imports dropped to a 2026 low while exports held above the previous two years, despite last week’s pullback. Total U.S. crude, including the SPR, dipped about 8mm barrels below the 5-year range along with Cushing inventories slipping to a 5-year seasonal low, even as output continued at near-record levels.

Run rates also drew on the crude balance, with utilization hitting its highest level since January as refineries ramped back up across the country. PADD 1 showed the only slowdown last week, falling to the seasonal average after spending all year well ahead. Throughput came back strong in PADDs 2 & 4, particularly in PADD 2 where Marathon Robinson returned from a planned mid-March maintenance shutdown. PADD 3 runs hit nearly an 8-year high at 98% utilization despite ongoing upsets at a few facilities in TX and LA.

Diesel stocks fell across all PADDs as export activity remained high and demand shot ahead of the previous two years, back to its 5-year average. All PADDs are at the low end or under their 5-year ranges, sinking total U.S. inventories to a 23-year low.

Gasoline stocks hit another fresh seasonal low, marking a 15th straight week of declines. Production ramped up substantially, matching increased demand ahead of the holiday weekend, while imports remained at seasonal lows. Low inventories across all PADDs leaves total U.S. stocks around 4mm barrels below the 5-year range and 12mm barrels below average.

Jet fuel stocks increased with the lone build in PADD 3 sending levels back to the top of their seasonal range. Imports fell back below the 5-year range, but exports remain at seasonal highs. Increased production alongside lowered demand led to the build last week, holding total U.S. jet stocks at seasonal 5-year highs.

Latest Posts

Energy Rally Gains Steam As Global Supply Chain Pressures Mount

Energy Markets End A Wild Week With More Questions Than Answers

Middle East Tensions And Russian Export Ban Rock Energy Markets

Week 27 - US DOE Inventory Recap

Energy Markets Face Growing Uncertainty As Conflicts Threaten Oil Flows

Bullish Fundamentals Clash With Bearish Speculation In Global Oil Markets

Social Media

News & Views

View All

Energy Rally Gains Steam As Global Supply Chain Pressures Mount

Energy Markets End A Wild Week With More Questions Than Answers