Energy Markets On Edge: Oil Swings, Strait Uncertainty, And Diesel Disruptions

It’s been another eventful overnight session for energy markets as the world tries to decipher fact from fiction in the barrage of headlines about the U.S. negotiations with Iran and the status of the world’s most vital shipping lane.

After a few days of chaotic selling, futures started rallying Thursday afternoon after the settlement as Iran’s allegedly supreme leader claimed the country was insisting on keeping its Uranium, which would seem to be a deal killer that will increase the likelihood that the fighting will soon resume.

Prices have since eased, with crude oil futures wiping out earlier $3/barrel gains, after reports of “slight progress” in negotiations and news from Iran’s new strait monitors that suggest 35 ships cleared the area in the past 24 hours. If true, that would be the largest movement of vessels since the war began, but still about 100 ships/day shy of normal levels. With ships turning off their tracking devices, and electronic jamming of signals going on, it’s impossible to verify the actual number of ships moving through the strait, but ship tracking websites continue to suggest the real number is much lower than what Iran’s navy is claiming.

Futures will trade in an abbreviated session Monday, although U.S. banks are closed and spot markets will not be assessed. Given how many times we’ve already seen markets have huge swings when futures start trading Sunday night, and the likelihood that we could either see war or peace announced over the weekend, don’t be surprised to see more suppliers making price changes over the holiday weekend.

Despite the 30 cent pullback in futures this week, retail fuel prices remain close to the record highs set back in 2022 as we head into Memorial Day weekend, which kicks off the summer driving season. How much will people travel with high fuel prices is a major question and we’ll get our first glimpse at the real data following the first big travel holiday in the next 2 weeks.

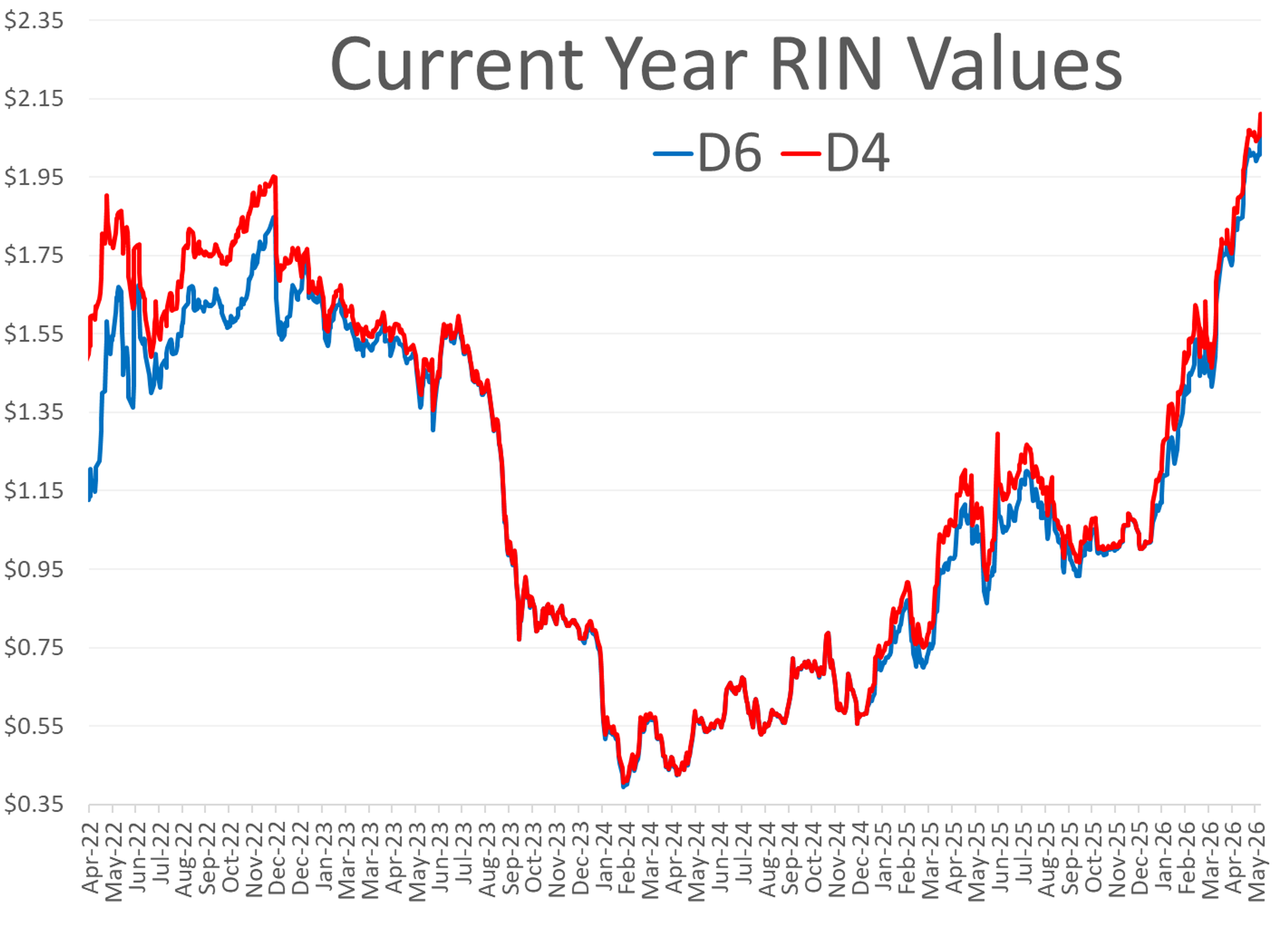

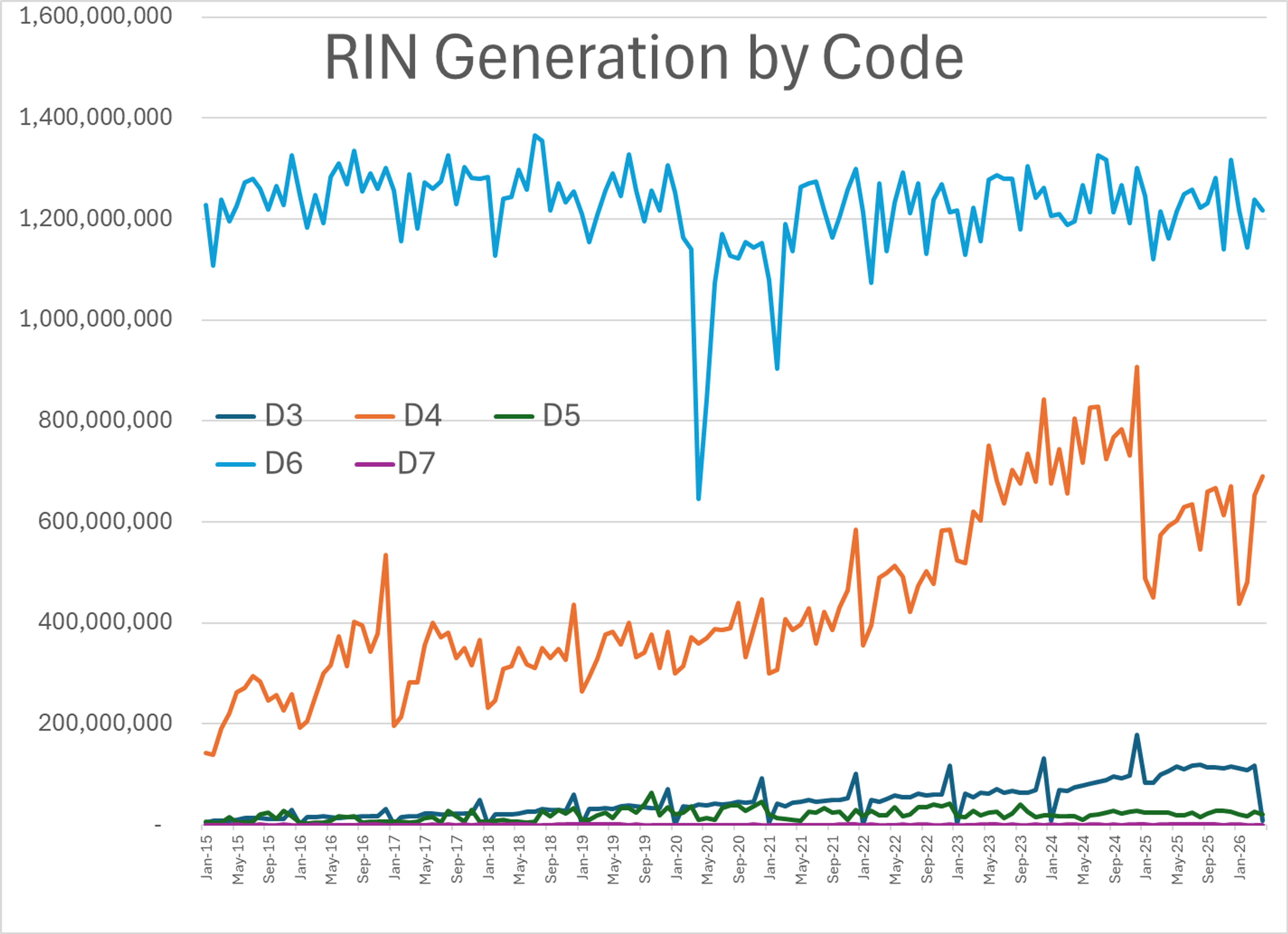

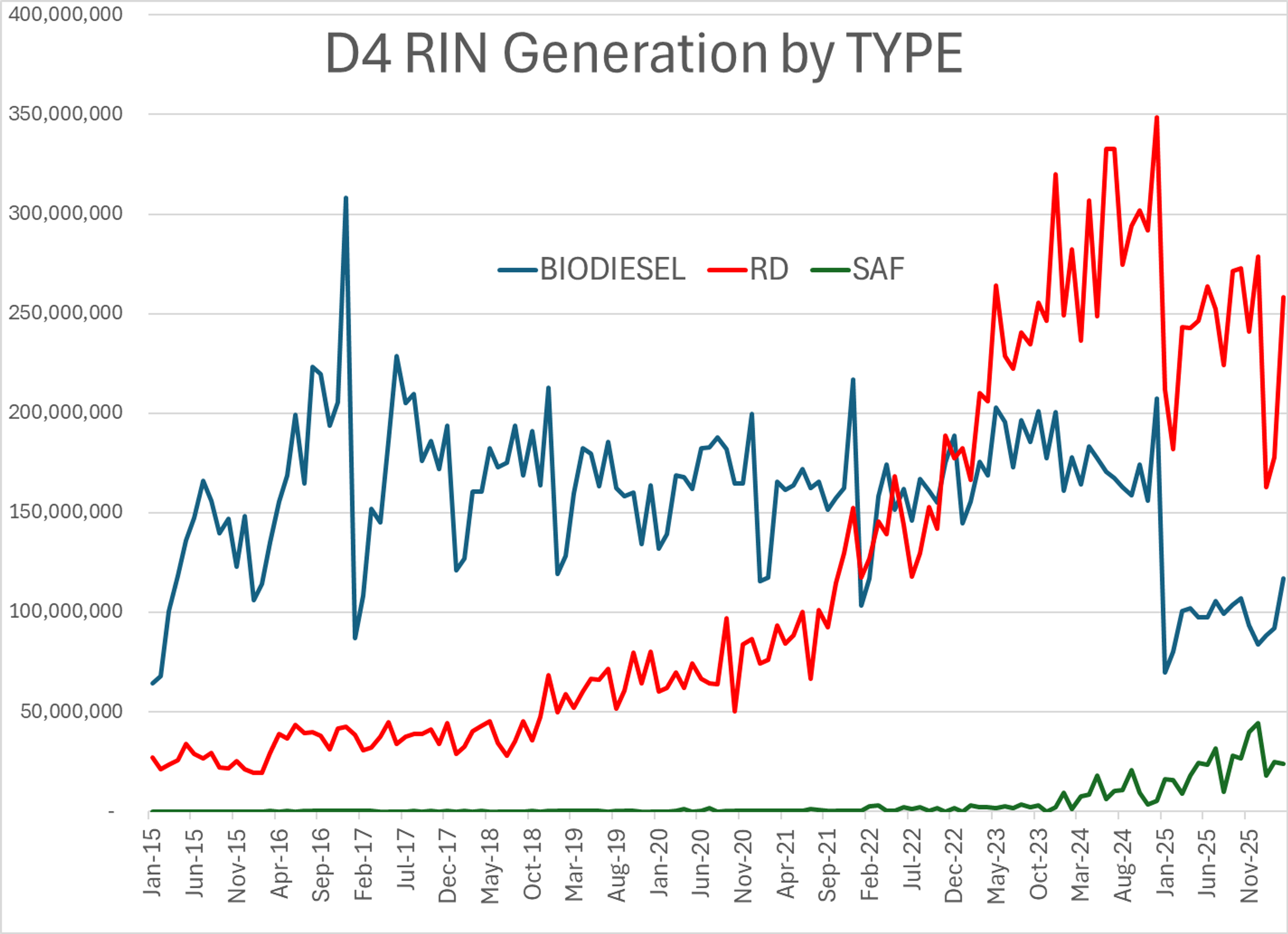

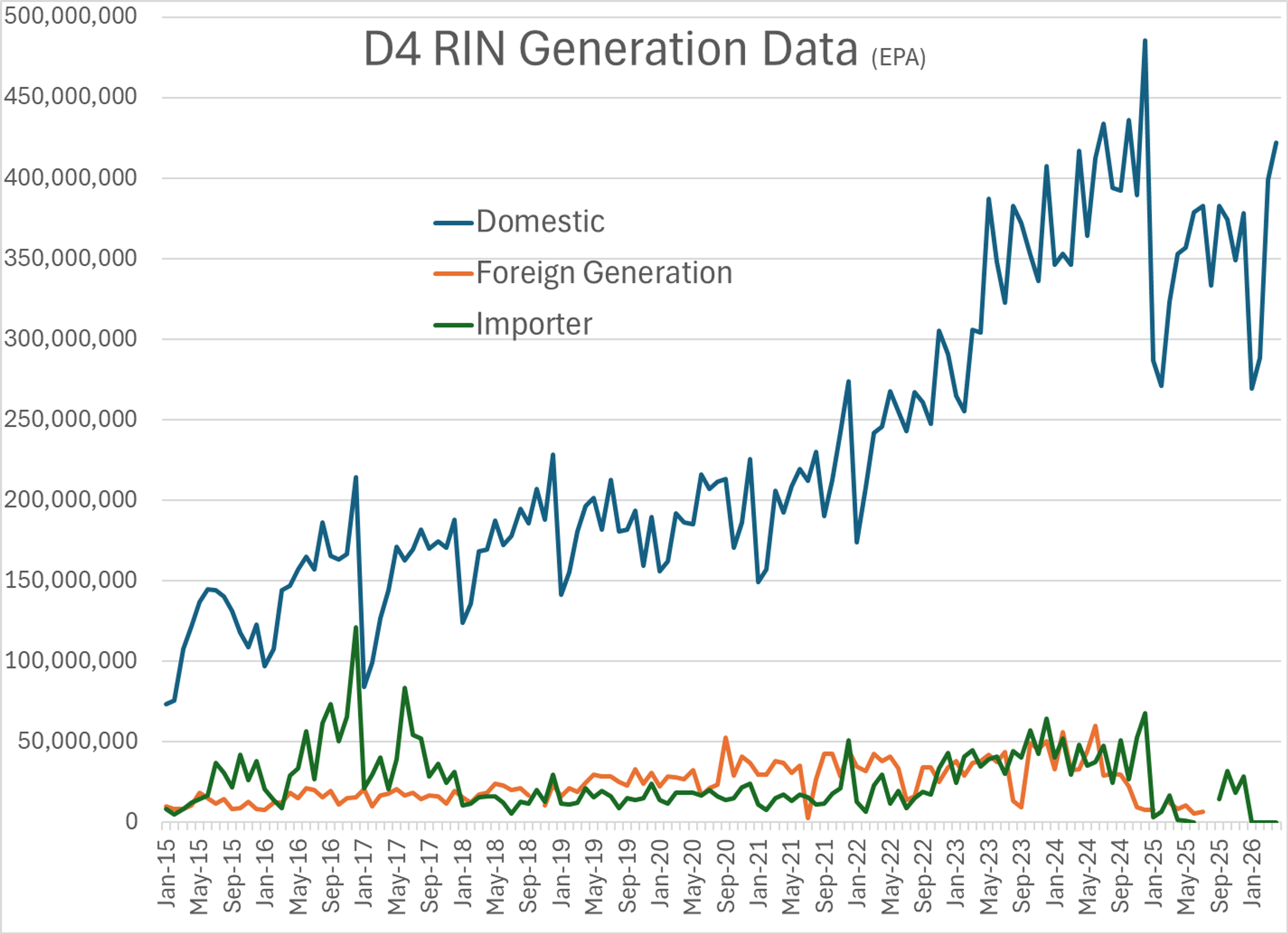

RINs hit a new all-time high for D4 and D6 values Wednesday after the EPA released its April RIN Generation data showing that domestic producers are ramping up production of RD and biodiesel, and yet the volumes are still woefully short of the EPA’s mandate for the year. Imports continue to be non-existent for renewables as high RIN values have not yet been enough to offset the loss of the $1/gallon Blenders Tax Credit at the end of 2024, which is why some in the industry are still lobbying for a return of the BTC in addition to the Producers Tax Credit (AKA 45Z) that offers incentives to domestic producers.

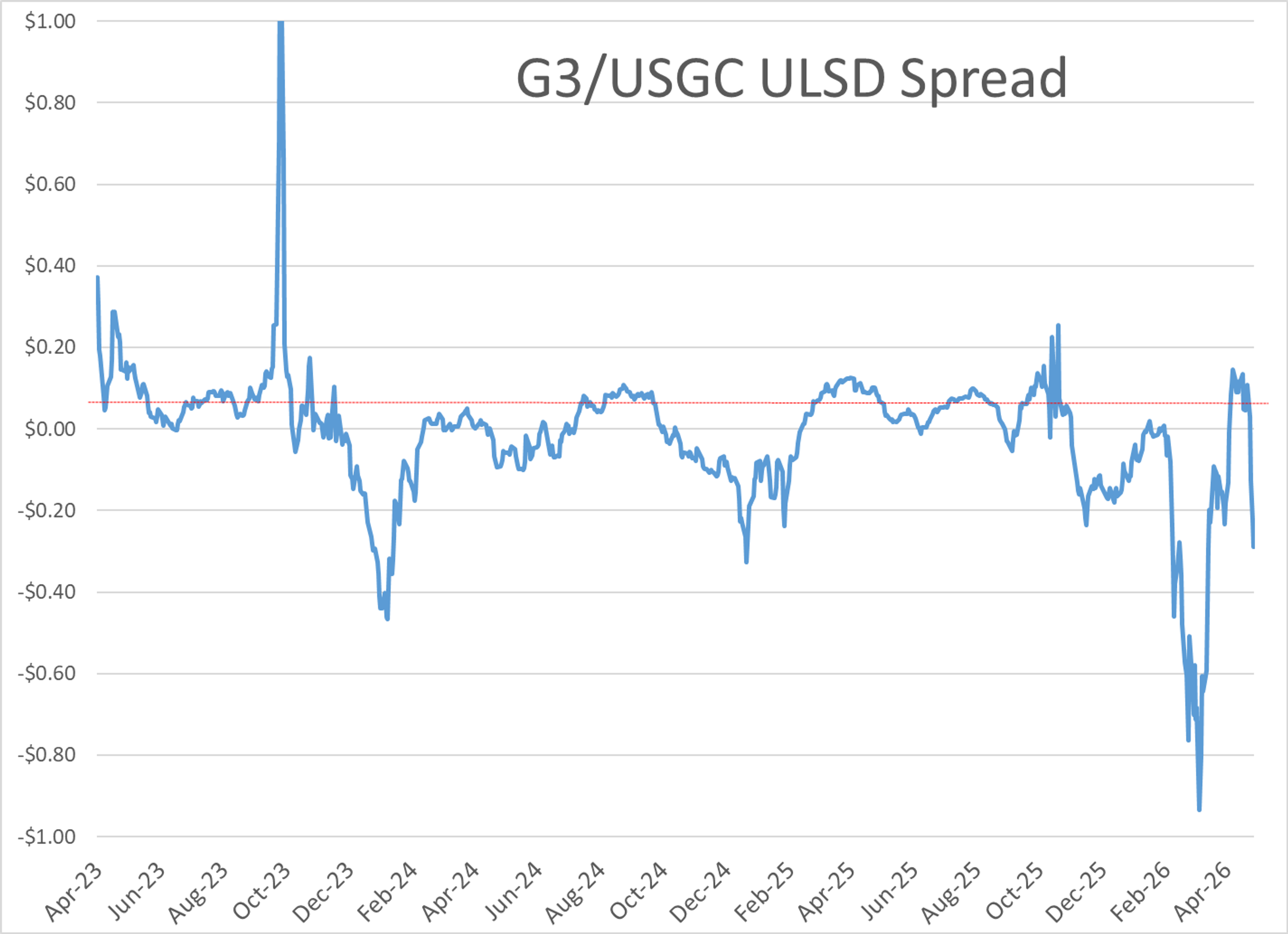

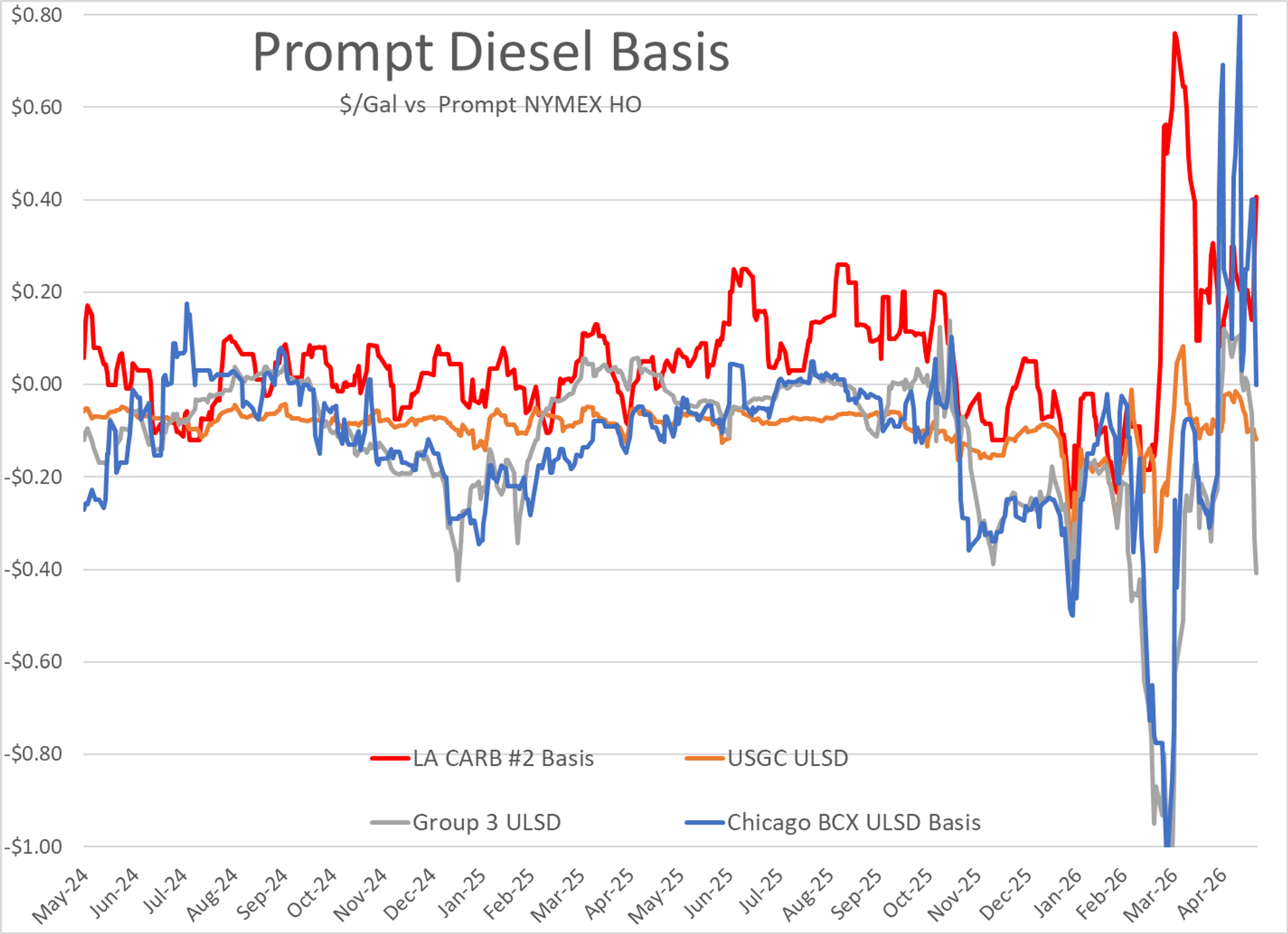

SAF production continues to be left out in the RIN rally, as the updated 45Z rules for the year no longer additional incentive for Renewable Jet vs Renewable ULSD, and the diesel is notably cheaper to produce, so plants are prioritizing RD output. That extra output is creating huge spreads in West Coast diesel markets that see traditional diesel very tight, with premiums of 40-50 cents/futures, while Renewable Diesel has become oversupplied, forcing discounts of 50-80 cents compared to the traditional diesel grades plus their environmental fees.

Marathon and PBF Continue to struggle at their Los Angeles area refineries, with both companies announcing a week of planned flaring at their respective plants starting today in Thursday filings with the AQMD, and then PBF reported yet another unplanned flaring event overnight.

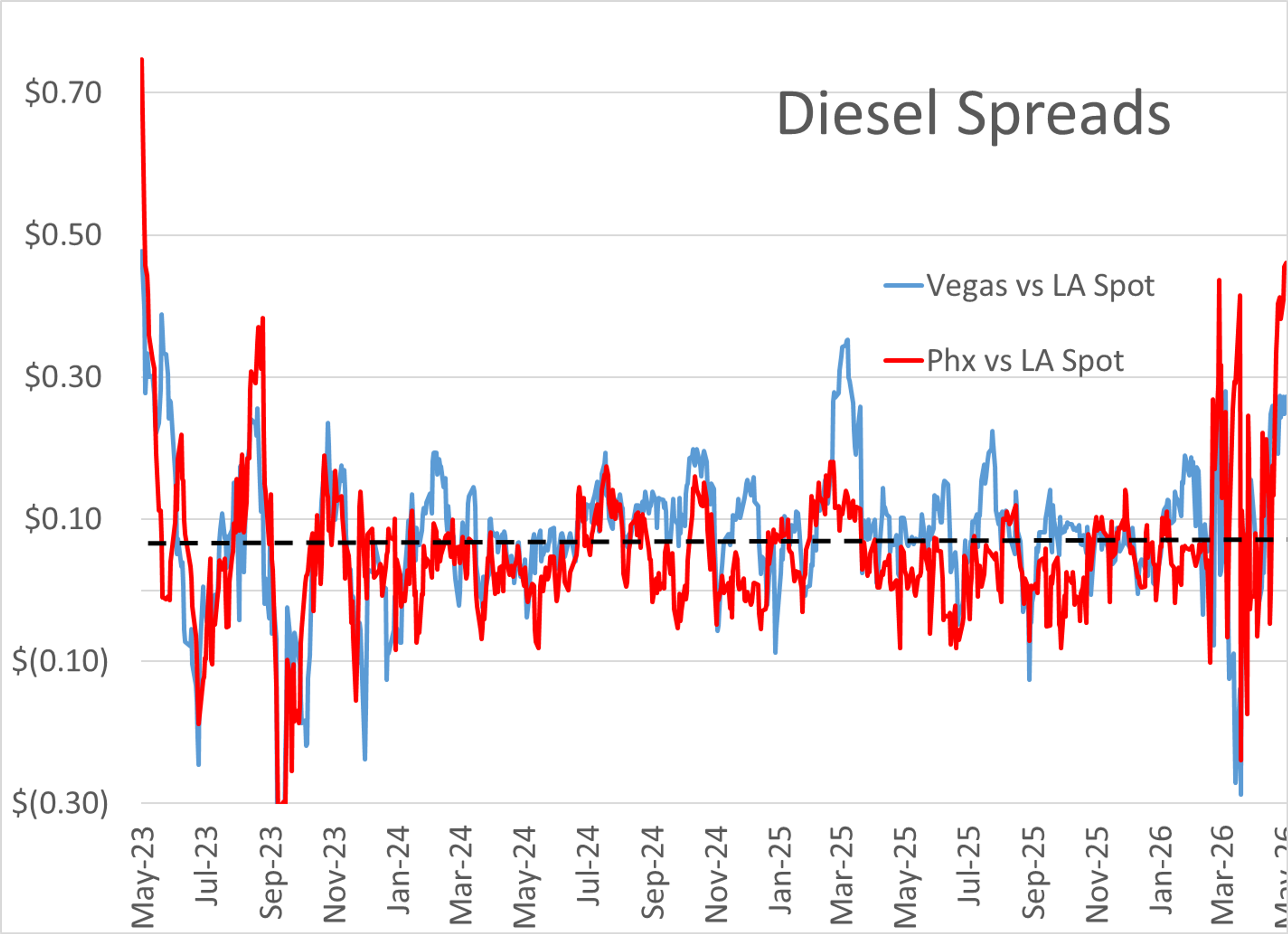

That tight diesel supply is spreading across the southwestern U.S. with rack spreads from El Paso to Phoenix and Las Vegas approaching levels we haven’t seen since the chaotic spring of 2023 when multiple refiners who had delayed maintenance during the huge margin environment in 2022 all went down at the same time. Meanwhile, midwestern diesel values are plummeting as plants return to normal output and the planting season demand has ended, opening up more gaps approaching $1/gallon between markets. In other words, if you’re heading anywhere South West from Oklahoma for Memorial day, bring a can of diesel with you.

Speaking of delayed maintenance, Energy News Today reported Motiva was deferring a major turnaround at its 630mb/day Pt Arthur TX facility from the fall of 2026 to the fall of 2027 to try and capitalize on the exceptional margin environment we’re currently experiencing. This is the latest in a long line of refiners delaying or minimizing work to maximize output, which is likely to make the domestic supply situation next year more vulnerable to upsets.

Latest Posts

Gasoline And Diesel Rally Despite Lower Crude Prices

Crude Retreats Ahead Of Holiday Weekend Despite Tight US Inventories

Gluts, Draws, And Disruptions: A Busy Start To July Energy Markets

Week 26 - US DOE Inventory Recap

Tight Inventories And Outages Push Diesel Prices Higher Into June Close

Oil Climbs On Strait Tensions As Cracks Emerge Beneath The Surface

Social Media

News & Views

View All

Gasoline And Diesel Rally Despite Lower Crude Prices

Crude Retreats Ahead Of Holiday Weekend Despite Tight US Inventories