Energy Markets Caught In The Crosscurrents of Rumors, Risks, And Reality

It’s been a choppy start to the trading week with multiple nickel swings in either direction for refined products so far this morning with numerous conflicting headlines continuing to confound. Diesel prices have swung between gains of almost 10 cents/gallon to 2 cent losses, while RBOB gasoline futures have gone from nickel gains to trading 3 cents lower and crossed the breakeven mark a handful of times along the way.

The headlines roiling markets today include more social media threats from the U.S. President, Iran suggesting negotiations are progressing despite the bluster, reports that Iran allowed 30 ships to transit the strait over the weekend while also attacking a nuclear plant in the UAE, and rumors that the U.S. will lift sanctions on Iranian crude to try and help calm markets during negotiations.

Charts suggest that prices may be stuck in neutral short term, but the potential for another big breakout to the upside exists if ULSD futures can break resistance around the $4.20 mark and if RBOB can climb back above the $3.80 range.

After multiple unplanned flaring events last week, PBF announced 2 different rounds of planned flaring for “Start-up/Shut down” as it apparently works to fix the unnamed units having trouble. The first event announced Friday was set to run Saturday-Tuesday, and the 2nd round announced this morning is set to run from today through May 25th. While the cause of these upsets and units impacted are still not publicly available, the LA spot market continues to shrug off the news.

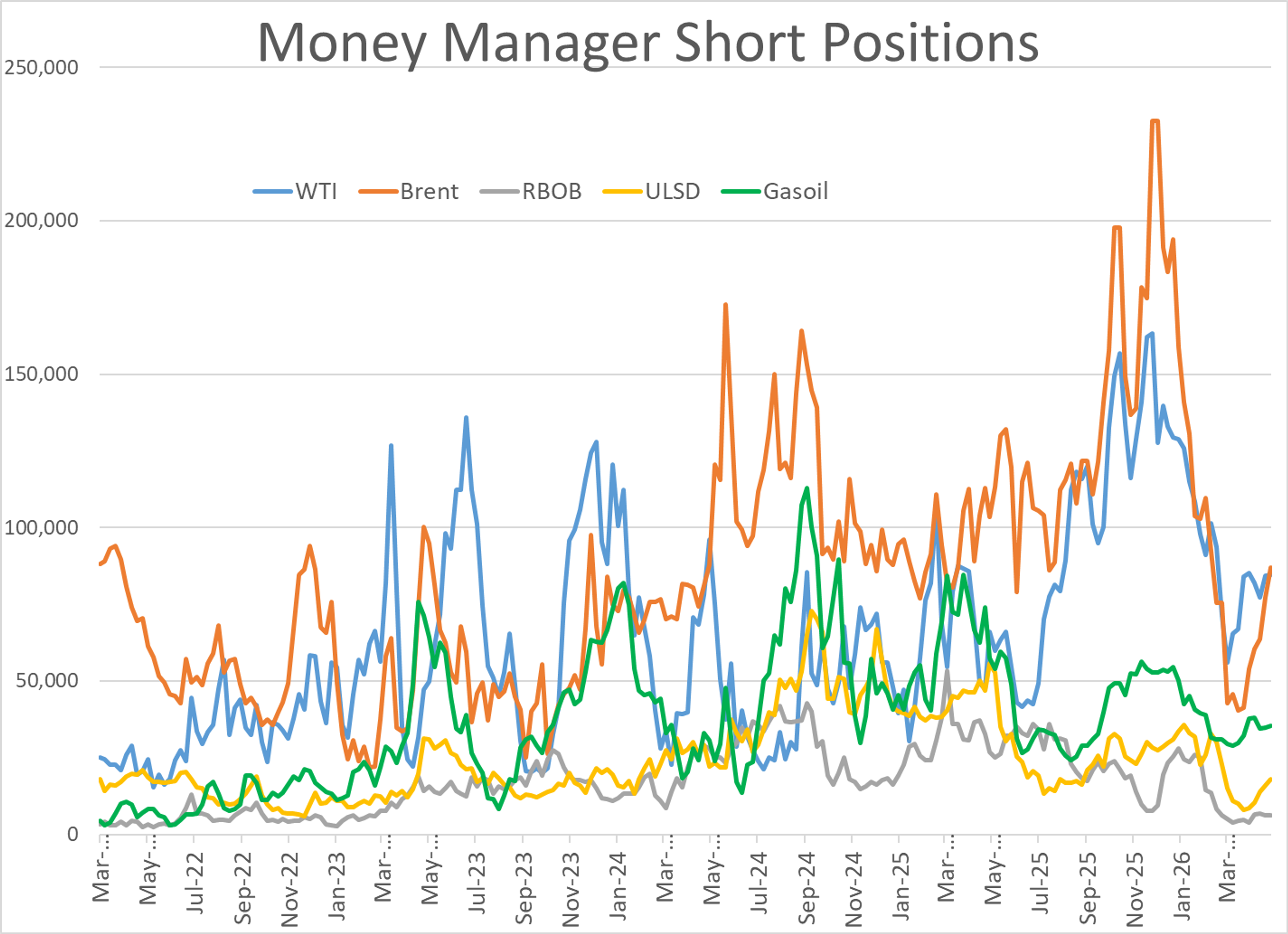

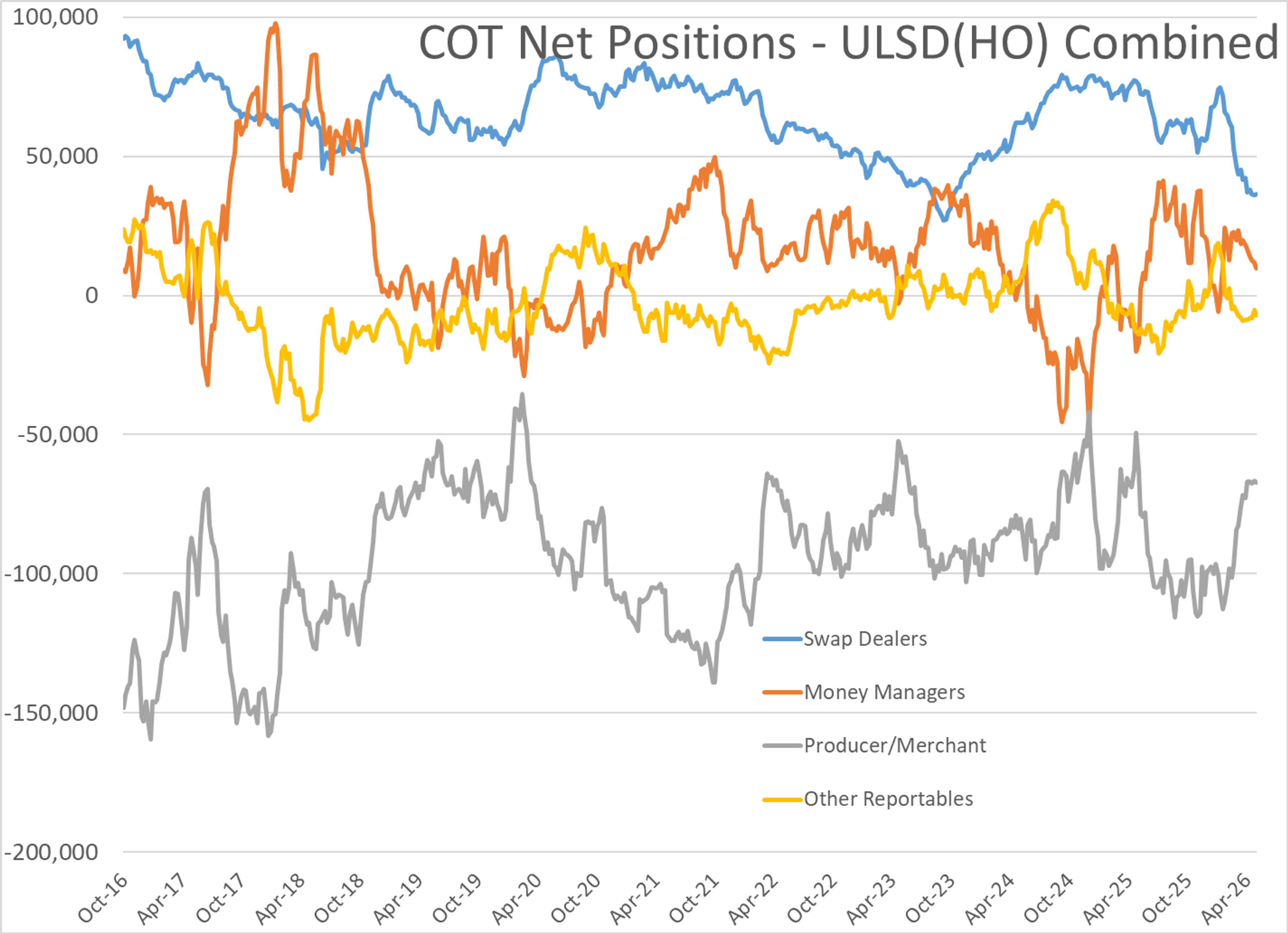

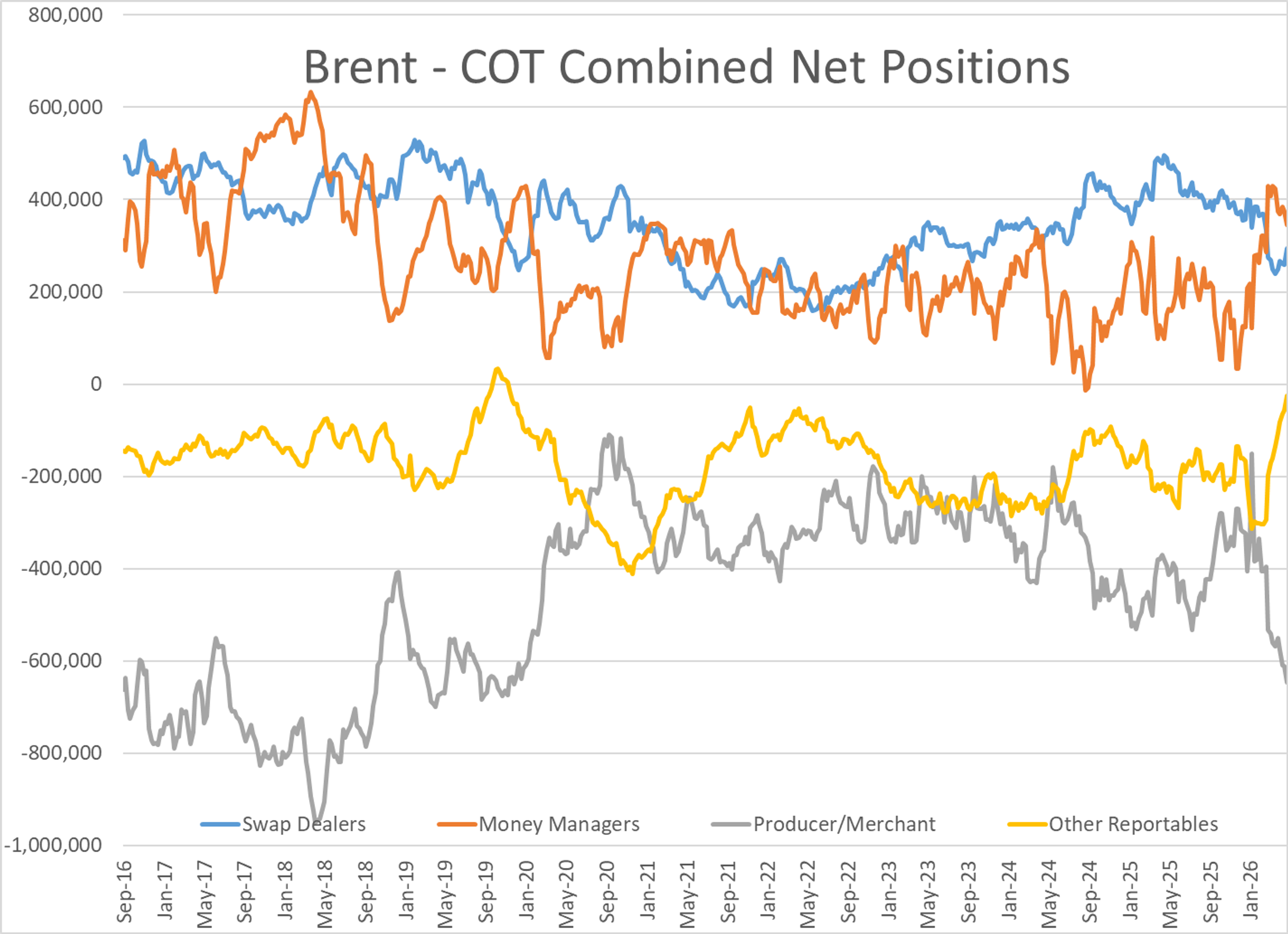

Money managers were making modest reductions in their net length in energy contracts last week with Brent, WTI, RBOB and ULSD all ticking lower. Brent crude saw the biggest change with a net length decrease of 28,000 contracts with roughly 2/3s coming from long position liquidation and the rest from new short positions.

After being run over on the biggest amount of money ever bet on lower oil prices to start the year, big funds are starting to take another swing on lower price bets, having raised their short positions in Brent for the past 4 straight weeks, although the total short interest is still just a fraction of where it was when “there’s a billion barrels of oil at sea” was the dominant market headline just 6 months ago.

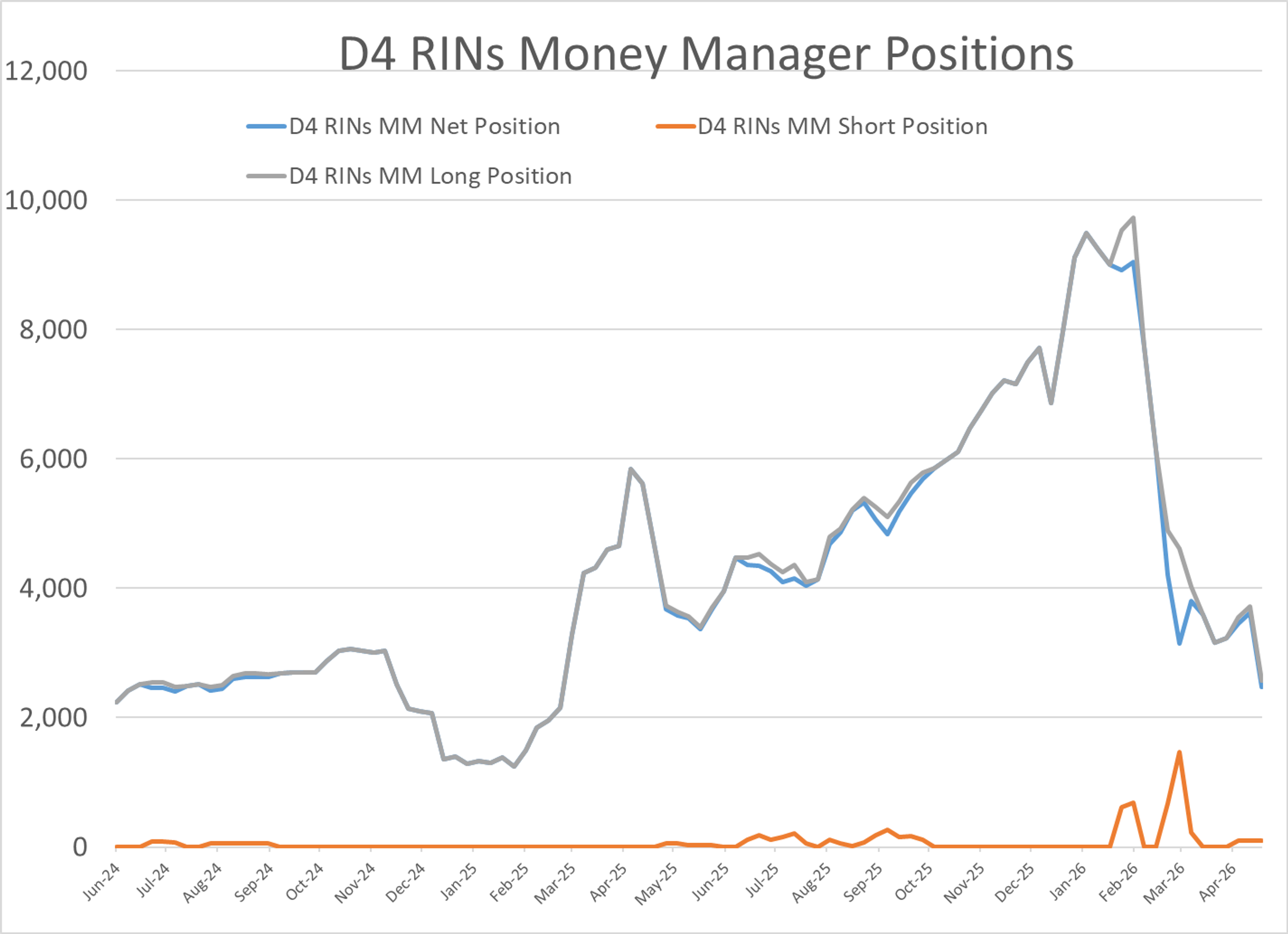

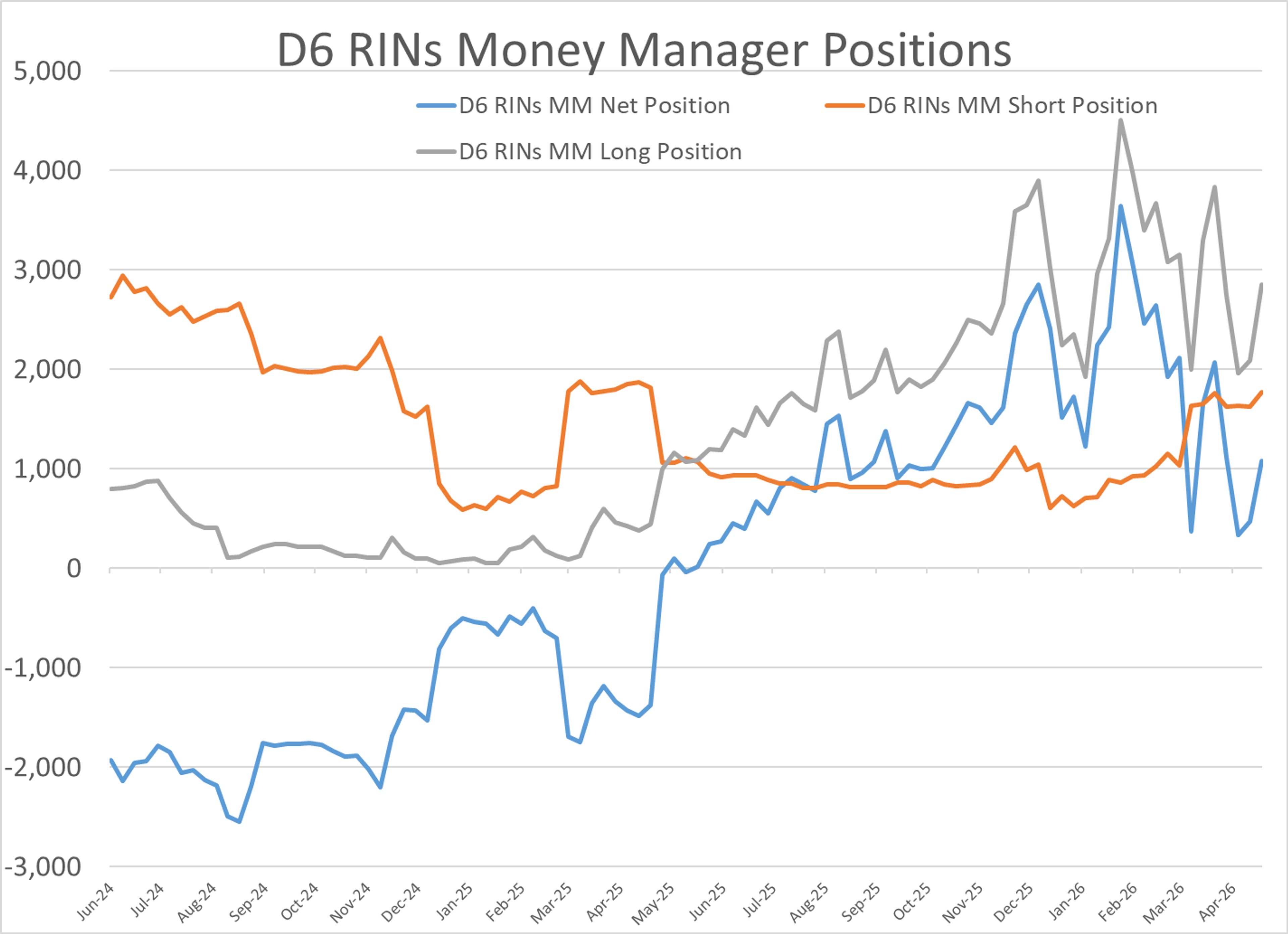

The large speculator trade category increased its D6 RIN length last week, but decreased its D4 holdings at prices moved north of the $2 mark.

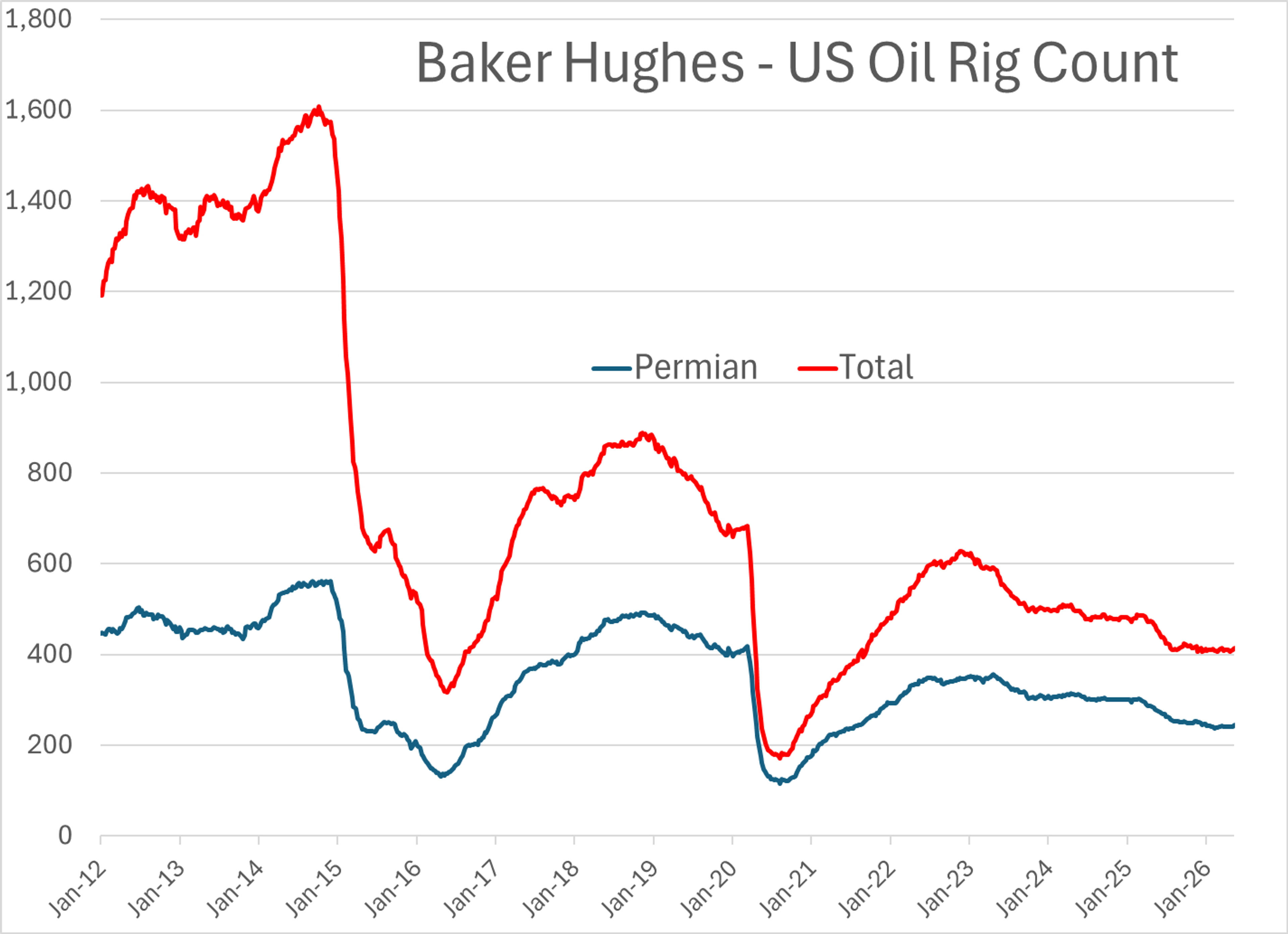

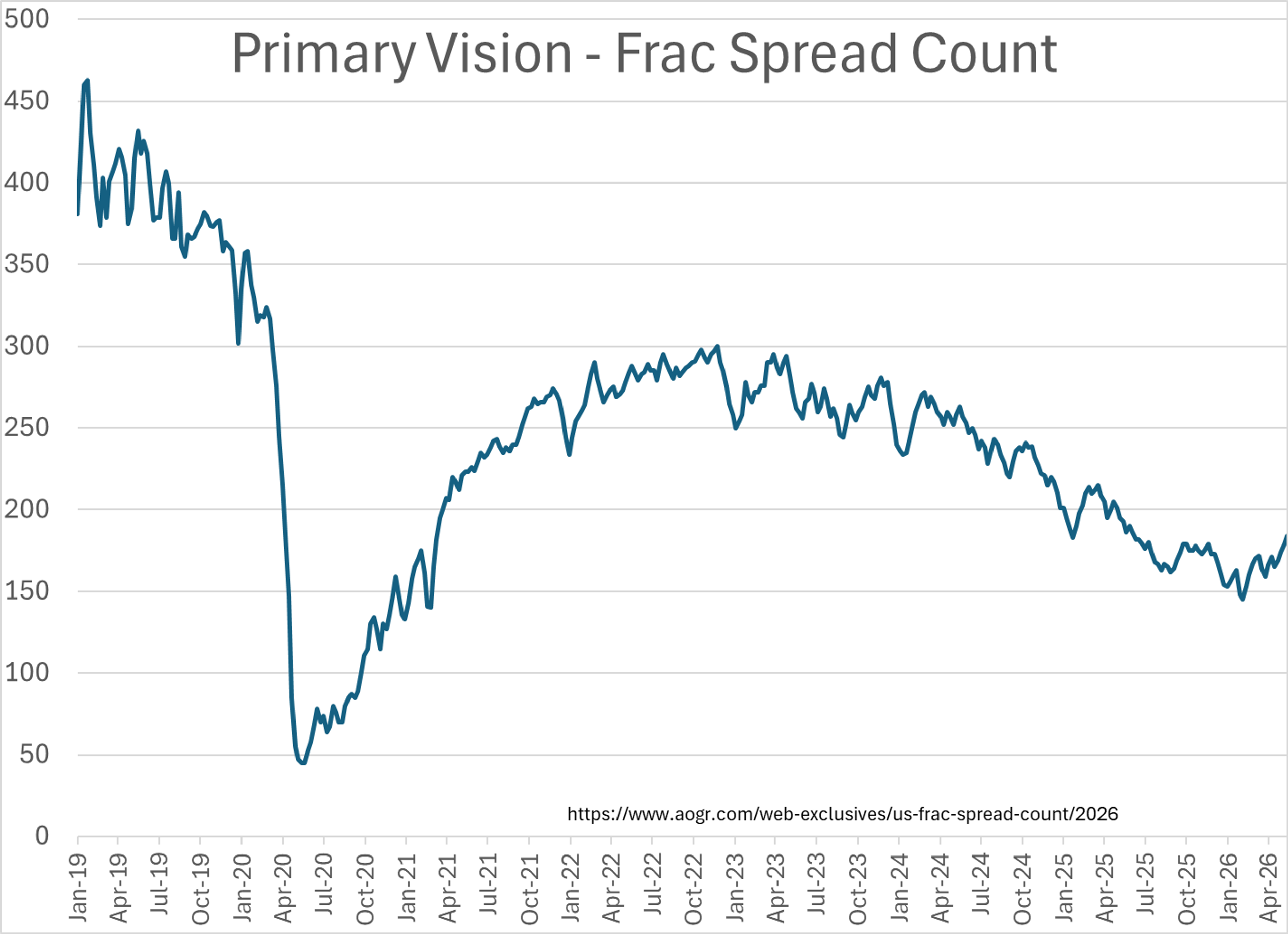

U.S. producers finally seem to be ready to jump on the “higher for longer” oil price bandwagon as there appears to be no quick end in sight for the war, with the Baker Hughes oil rig count and Primary Vision fracking crew count both increasing by 5 last week. The Permian basin accounted for the majority of the rig count increase, while the natural gas rig count dropped by 1 on the week. Fracking crews have increased by 19 (11.5%) over the past month. Last week the EIA estimated that the resurgence of drilling and fracking activity in the U.S. will increase oil production to a new record high in 2027 north of 14 million barrels/day, which means ancillary products like natural gas, propane and other natural gas liquids will also see new record output as they come along for the ride.

Latest Posts

Crude Retreats Ahead Of Holiday Weekend Despite Tight US Inventories

Gluts, Draws, And Disruptions: A Busy Start To July Energy Markets

Week 26 - US DOE Inventory Recap

Tight Inventories And Outages Push Diesel Prices Higher Into June Close

Oil Climbs On Strait Tensions As Cracks Emerge Beneath The Surface

Energy Prices Reverse As Market Shrugs Off Tanker Attack, Focus Shifts To Supply Constraints

Social Media

News & Views

View All

Crude Retreats Ahead Of Holiday Weekend Despite Tight US Inventories

Gluts, Draws, And Disruptions: A Busy Start To July Energy Markets