Energy Rally Stalls As Traders Weigh Supply Disruptions And Global Signals

Energy markets are taking a breather to start Wednesday’s session, a brief pause after 3 straight sessions of strong gains, as we sort with the data deluge of weekly and monthly reports all converging in 24 hours, while the world watches meetings in China for signs of what may come next.

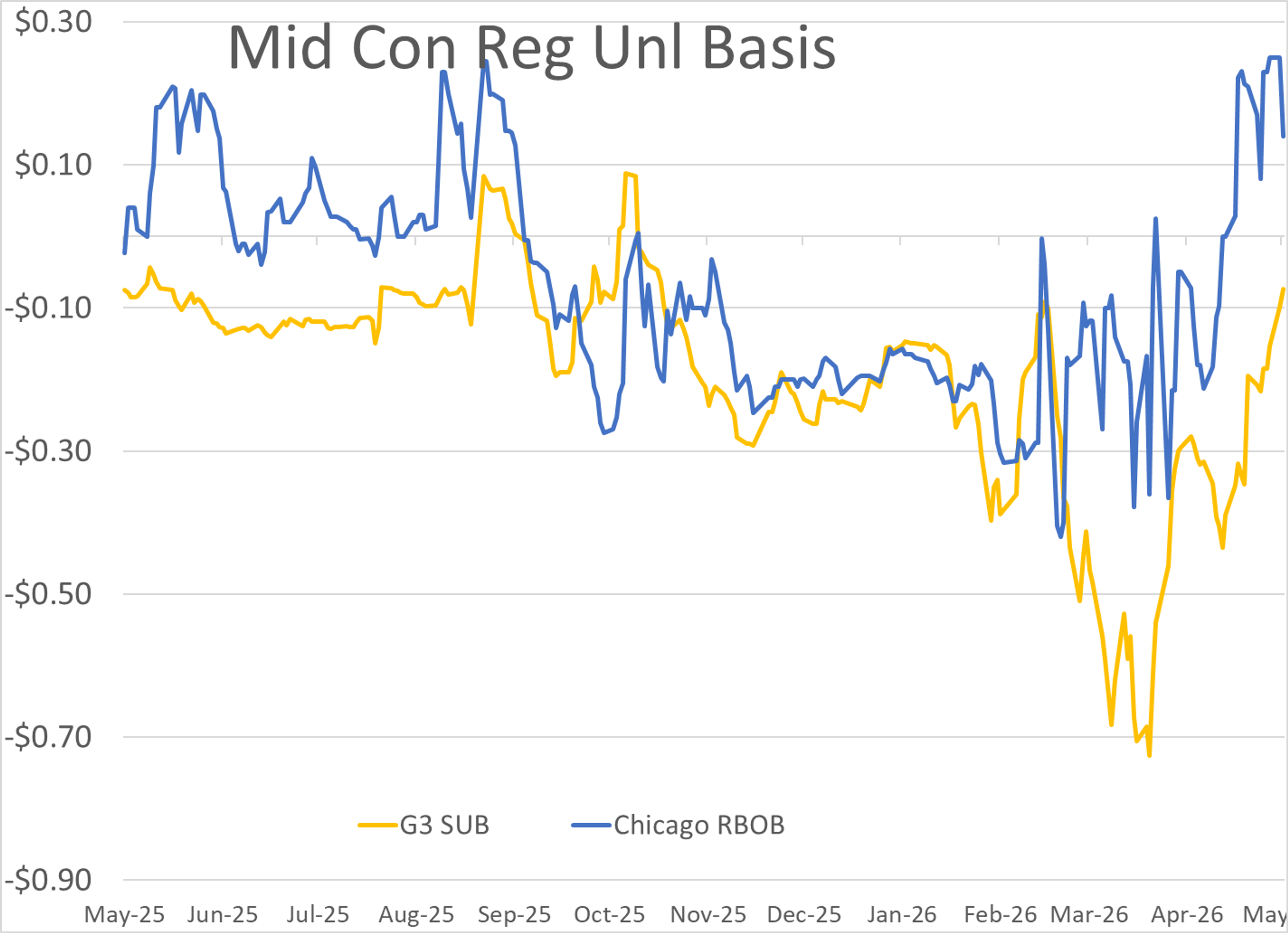

Chicago diesel premiums pulled a Keyser Soze Tuesday with deals done just a penny over futures, after trading at $1/gallon+ premiums just a couple days ago. Gasoline diffs in the region have been much less volatile in the wake of numerous refinery issues, but also saw healthy selling as it appears those facilities are quickly returning to service. While local operating rates appear to be recovering, there’s still no progress on the lockout at BP’s Whiting refinery, with union officials accusing the company of stalling in their negotiations.

Exxon reported a leak in an FCC unit at its 588mb/day Baytown TX refinery that started Monday and was expected to be fixed this morning. The limited emissions associated with the event suggest the unit was not forced offline as a result, and doesn’t appear like this will have a material impact on production.

PBF reported unplanned flaring at its 155mb/day Torrance CA refinery Tuesday afternoon after most traders had wrapped up for the day. The facility was already in the middle of 9 days of planned maintenance announced last week, so this most recent upset may not stem the tide of selling that’s pushed LA differentials sharply lower over the past several days.

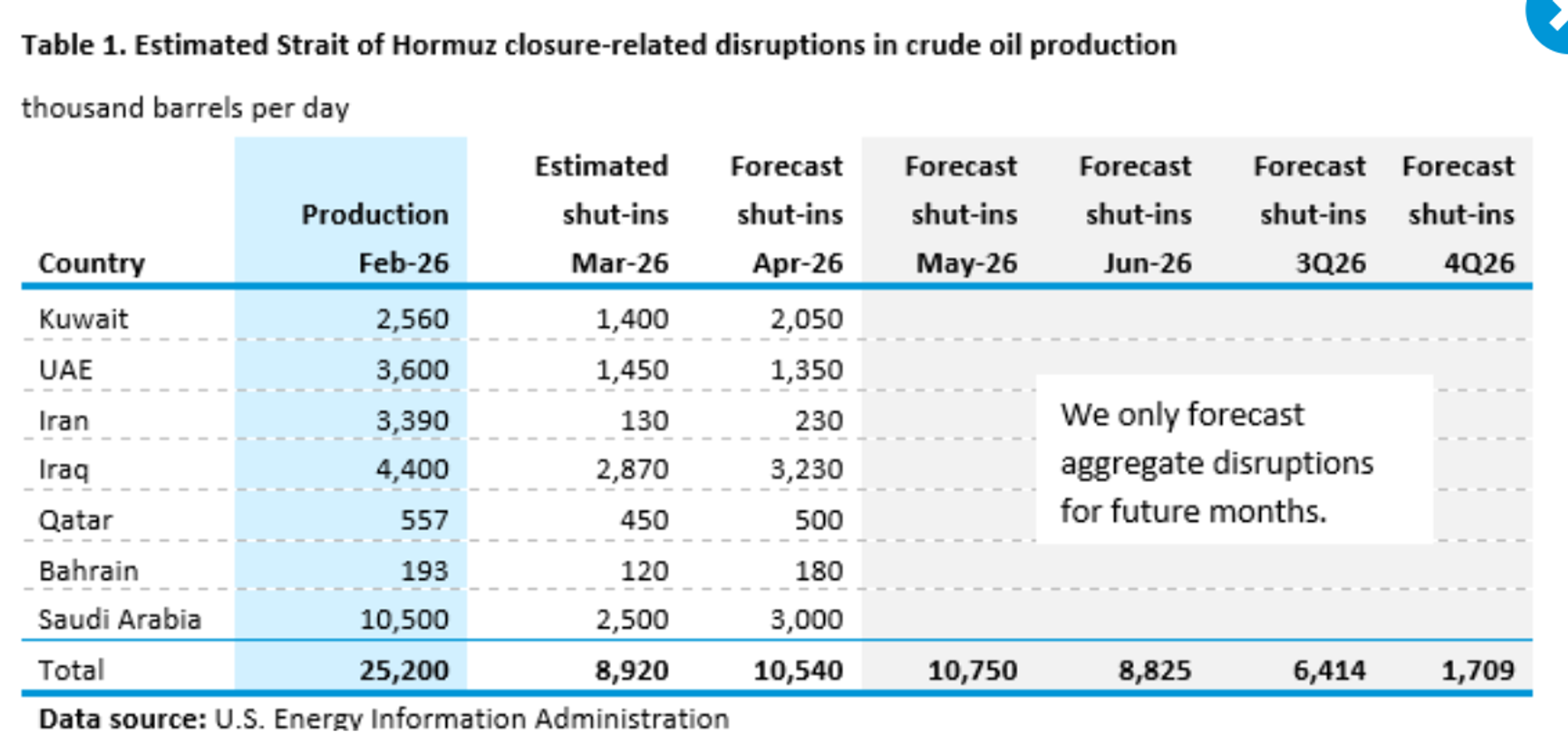

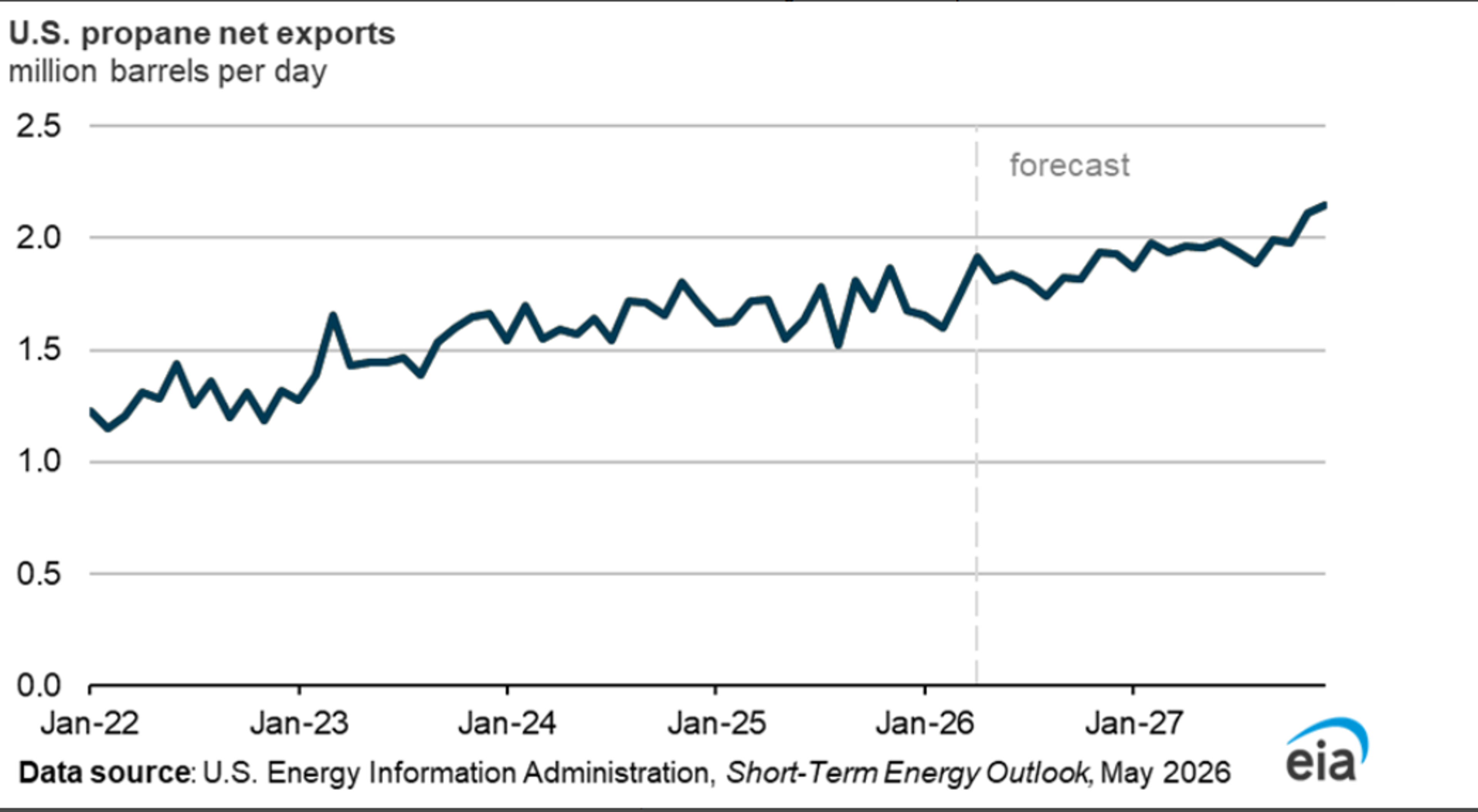

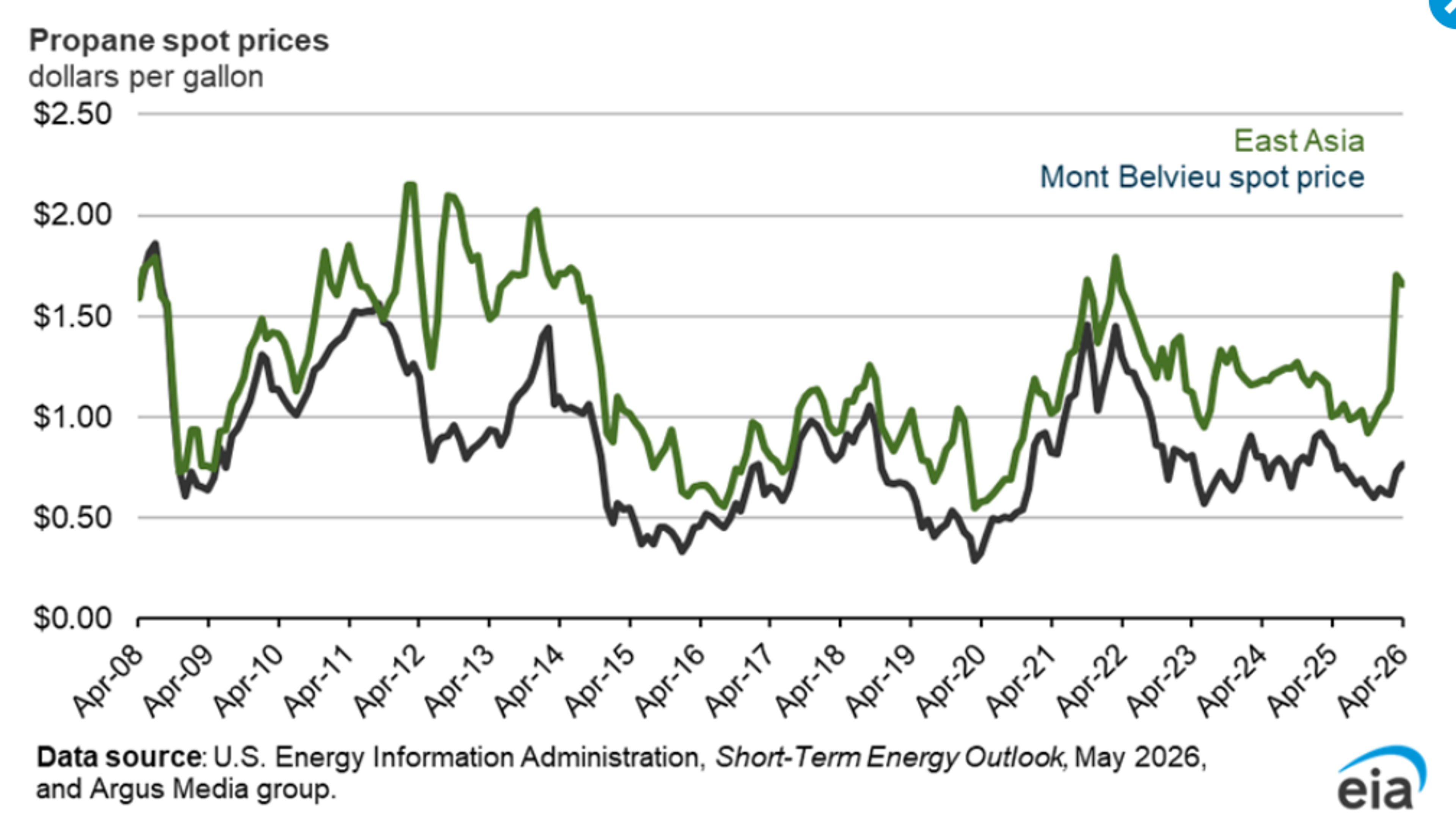

The EIA’s Short Term Energy Outlook estimates that 10.5 million barrels/day of crude oil production was shut-in in April as a result of the war, and projects that even IF the strait re-opens by June, we’ll still see 1.7 million barrels/day of production offline at the end of the year. The agency does predict that U.S. oil production will increase to a record high north of 14 million barrels/day next year as producers will start reacting to the wars impacts, and record export demand. The entire refined product section of this month’s report was focused on propane, which saw inventories reach record levels, despite steadily growing exports, as the byproduct of oil and gas drilling continues to set new records. Unlike propane, LNG exports are grwoing at a very unsteady pace, completely depending on new export facilities to freeze the gas before it can be transported. The agency noted two new facilities that recently came online and allowed a healthy increase in LNG exports in 2026, with more facilities slated to come online next year.

OPEC continues to do its best to talk around the war in its monthly report, choosing to refer to “geopolitical tensions” rather than the ongoing attacks between members of the cartel, and not mentioning the Strait of Hormuz once. The monthly report also made no mention of the UAE’s planned exit from the group. The report did show another large drop in total output during April, bringing the total decline since March closer to the estimates from others just under 10 million barrels/day since the “geopolitical tensions” in the Middle East broke out. Venezuela’s output ticked higher by 46mb/day in April, and is now about 10% higher than it was in January when its President was abducted by the U.S., surpassing 1 million barrels/day for the first time in years. Russia’s output meanwhile continues to decline, with output down 107mb/day during the month, and nearly 300mb/day since the start of the year. Since OPEC is trying to act like the war isn’t a thing, it’s also no surprise that they continue to suggest that the supply disruption and surge in prices is not negatively impacting economic activity, holding its demand forecast steady.

The IEA – who was built to counter OPEC’s influence after the oil embargos of the 70’s – not surprisingly continues to take the polar opposite approach to the war, stating that 10 weeks of war have depleted global inventories at a record pace, which is causing refinery run rates to plunge, and forcing a sharp drop in demand. The IEA’s estimate for shut-in production is much higher than the others at 14 million barrels/day, despite Saudi Arabia and the UAE being able to redirect some of their output. The report also highlights how China has rapidly slowed its oil imports, choosing instead to use up some of the huge reserves it built over the prior year at discounted levels, which is helping to alleviate the supply squeeze. The primary hits on demand so far are coming from reduced petrochemical and aviation activities.

The API reported more drawdowns in crude oil and distillate inventories of 2.2 million and 319,000 barrels respectively, while the industry estimate showed a modest build in gasoline stocks of 502,000 barrels that would snap a 2 month streak of declines if proven true. The DOE’s weekly status report is due out at its normal time this morning.

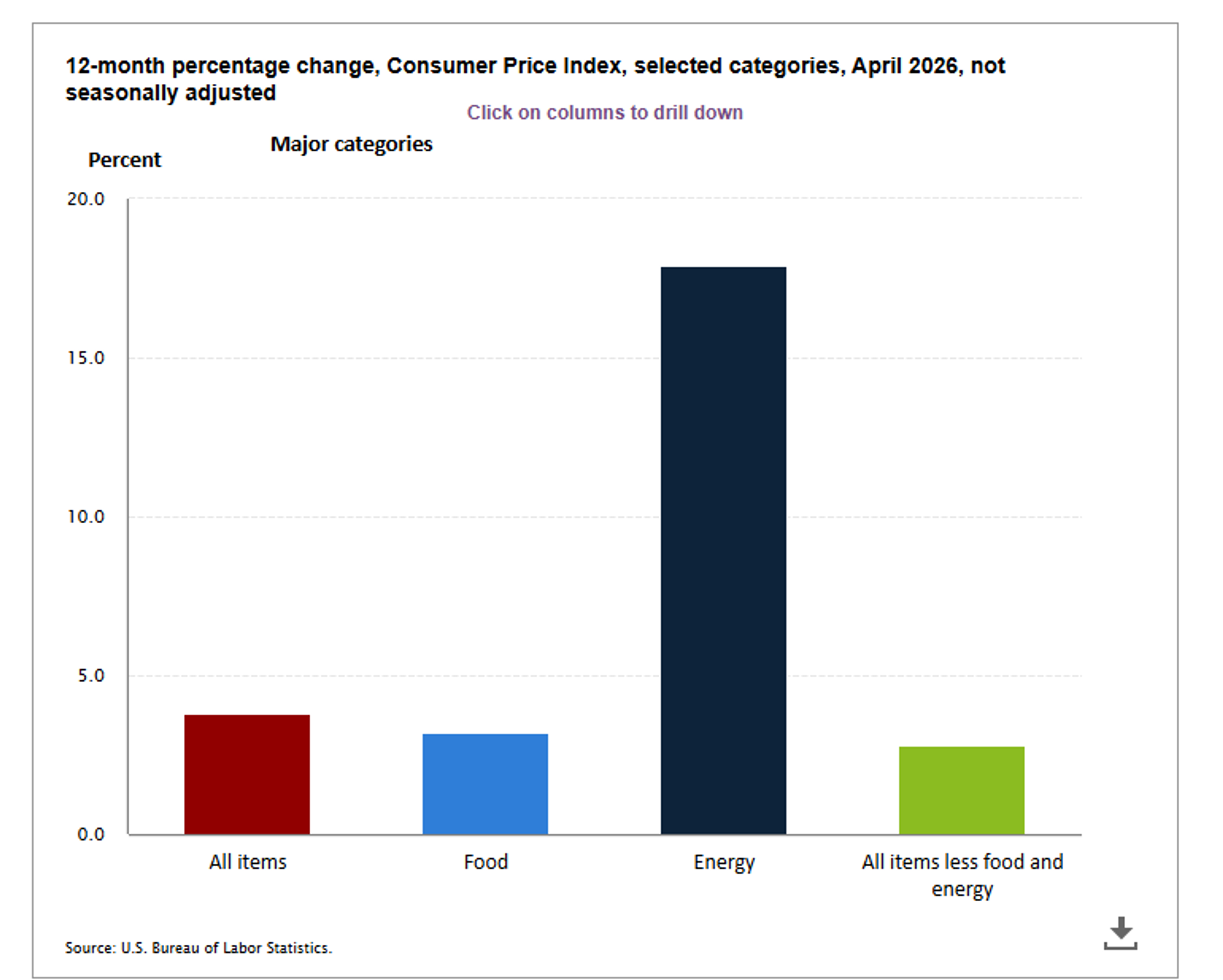

The CPI and PPI reports this week confirmed what everyone already knew: rapidly rising gasoline and diesel prices are bad for inflation, and have trickle down effects on numerous other goods that continue to hold levels well above the FED’s 2% target.

Latest Posts

Oil And Fuel Markets Regain Ground Amid Rising Supply Threats

Distillate Markets Tighten Amid Escalating Global Conflicts

Markets Weigh Economic Slowdown Against Growing Middle East Risks

The Growing Disconnect Between Diplomatic Headlines And Energy Reality

Week 31 - US DOE Inventory Recap

Markets Tread Water As Hormuz Hopes Meet Red Sea Reality

Social Media

News & Views

View All

Oil And Fuel Markets Regain Ground Amid Rising Supply Threats

Distillate Markets Tighten Amid Escalating Global Conflicts