Energy Markets At A Crossroads: Volatility Surges As Hormuz Shutdown Unfolds

Energy markets are surging to multi-year highs this morning as the “nightmare scenario” of a shutdown of the world’s most vital supply bottleneck plays out. Diesel futures are leading the way up more than 38 cents, briefly trading above the $3 mark for the first time in 2.5 years. RBOB gasoline futures are “only” up 12 cents so far, but thanks to the roll to summer-grade specs on the newly prompt April contract, they’re also trading at a 2.5 year high north of $2.40/gallon.

While these events and price reaction are certainly dramatic, it’s worth pointing out how the world is much different now than it was 50 years ago during the oil embargos and even 15 years ago when the U.S. was still a net importer of refined products, whereas today we’re the world’s largest exporter of refined products. That helps explain why we’re talking about oil in the $70 range not $150 range, and products pricing between $2-$3, not $4-$5.

Daniel Yergin made a simple point on CNBC this morning that this event all comes down to duration. If the Strait of Hormuz comes back online within a week or so this won’t be a major supply crisis, but if it lasts longer than a week the impacts will grow exponentially.

Why this is the biggest threat to oil markets we’ve seen in 50 years:

At least 3 ships have been attacked in the Strait of Hormuz, essentially shutting down tanker traffic for now. The Strait of Hormuz sees more than 30 million barrels/day equivalent of oil, refined products, LNG and NGLs transit every day. Roughly 20% of all oil and LNG shipments globally. While there are some pipeline alternatives for oil to bypass the strait, they can only replace a small fraction (less than 10%) of that tanker capacity, so prices will remain elevated and volatile until the strait is secured. There are lots of smaller impacts like container shipping and nitrogen fertilizer through the strait, but petroleum commodities are by far the biggest concern. Also keep in mind that there are no alternative routes for the LNG, and whenever natural gas gets tight, diesel becomes the supplemental option which we saw play out in dramatic style back in 2022.

Why the biggest threat to oil markets may not become the biggest supply problem we’ve seen in the past decade:

Most of the oil and products transiting the strait go to China, who was stockpiling oil by roughly 800md/day last year. Although China doesn’t publish its oil statistics, it’s believed that they have strategic reserves that should be able to cover up well over 6 months’ worth of imports, so an immediate shortage there can be avoided.

While the U.S. SPR is still far from the inventory levels seen prior to the releases following the 2022 supply squeeze, the U.S. does have more than 200 days of imports on hand in the SPR thanks to the rapid increase in production over the past 2 decades, and less than 10% of our imported oil comes from the Middle East. Canada provides nearly 2/3s of US crude imports unlike 40 years ago when 2/3s of our purchased oil came from the Middle East. If the fighting isn’t winding down in a few days, expect the U.S. to announce plans to use the SPR as needed to try and calm markets.

Iran has tried to close the strait previously, most notably during the “Tanker War” in the 1980s but those efforts were quickly thwarted by the U.S. navy and air force. A system of naval escorts provided safe transit through the strait, and will likely be part of the solution to this situation unless a cease fire or peace agreement is made soon.

It’s also worth noting that Iran has amassed a large amount of oil on ocean going vessels (outside the strait) prior to the attacks with few buyers due to sanctions. Similar to what we’ve seen with Venezuela, whenever diplomacy restarts, expect a bargaining chip to be loosening restrictions on those barrels which could be then be offloaded quickly. Longer term, Iran has spare capacity to bring more oil to market much more quickly than Venezuela, so in a year or so this could be bearish for oil prices, but the peace that will require has to happen first.

Impacts on U.S. Fuel supply network:

The events currently do not directly impact our domestic gasoline and diesel supplies, but the indirect impacts are already being felt. Suppliers across the country made large price increases and tightened down allocations over the weekend anticipating today’s big jump in prices.

East Coast diesel remains the most vulnerable given the low starting inventories in the region which is still recovering from the winter-storm demand surge, and now it’s likely Europe will be looking for more U.S. exports due to Kuwait’s diesel exports being trapped behind the strait. Note that refined product exports don’t count toward OPEC quotas, so several gulf states have ramped up their refining capacity in recent years to effectively increase production without violating the cartel rules.

Other News:

8 members of the OPEC cooperation agreement agreed to increase their output target by a combined 206kbd starting in April, citing healthy market fundamentals and steady global economic growth for continuing to unwind its voluntary output cuts. Actual output levels will vary from the target levels since countries like Iraq and Kazakhstan are still supposed to lower production to make up for previous quota violations, and obviously production levels could be impacted if the world’s key oil artery remains blocked for a sustained period of time.

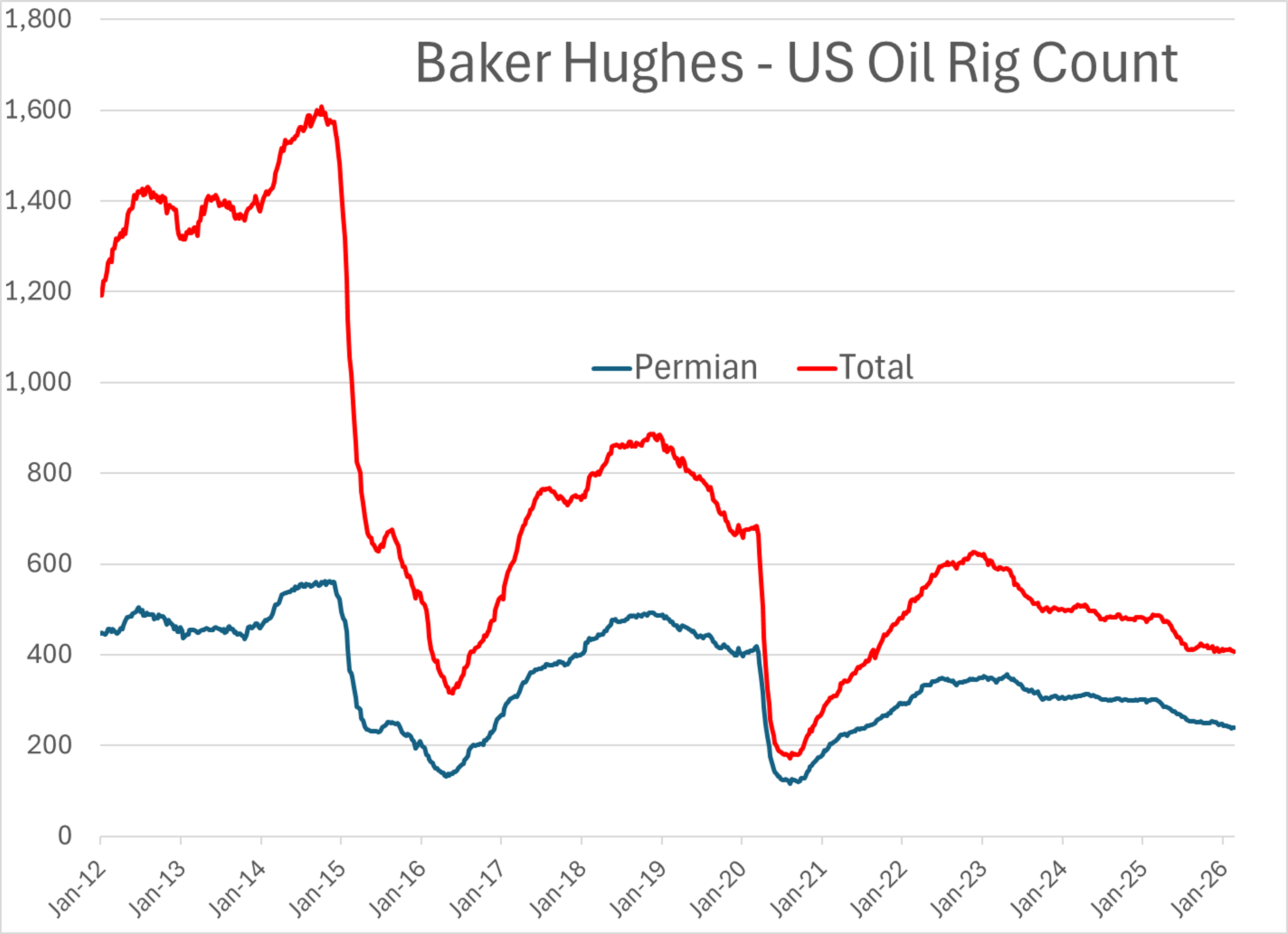

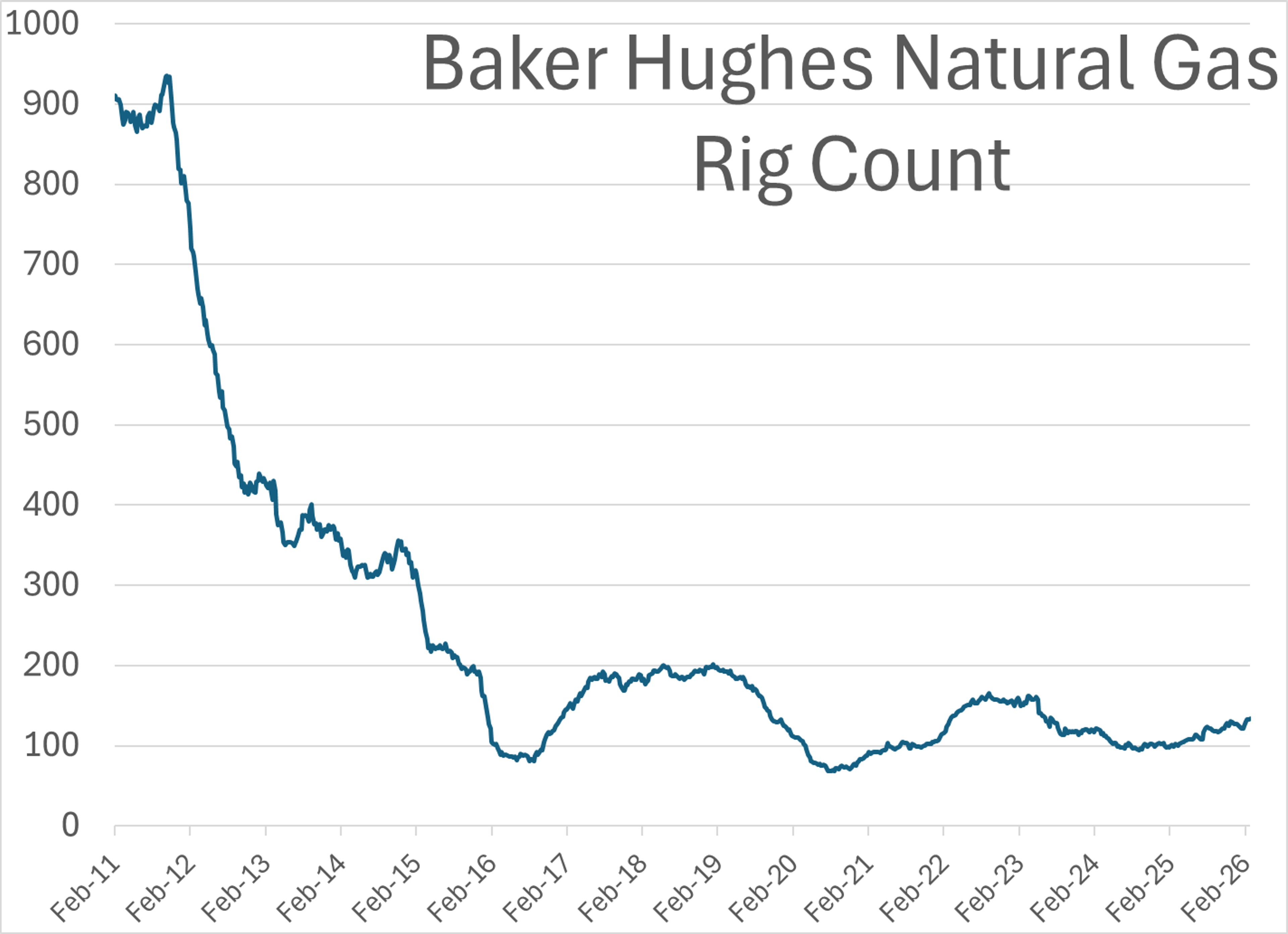

Baker Hughes reported the U.S. Oil rig count declined by 2 last week, just 1 rig away from a fresh 5 year low, while the natural gas rig count increased by 1.

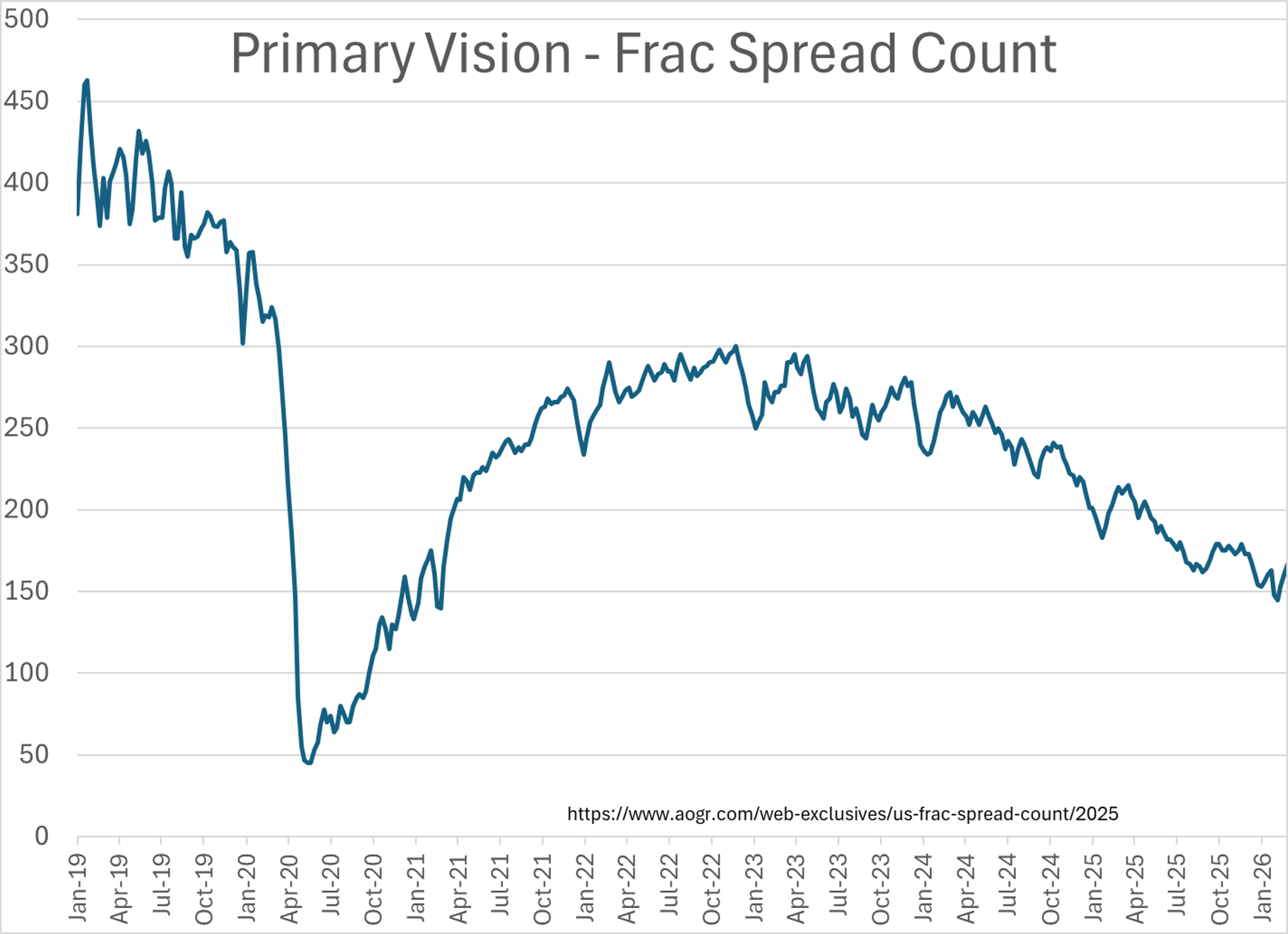

The Primary Vision count of fracking crews active in the U.S. increased by 7 last week to 167, which marks a 2.5 month high as crews return from their winter hiatus.

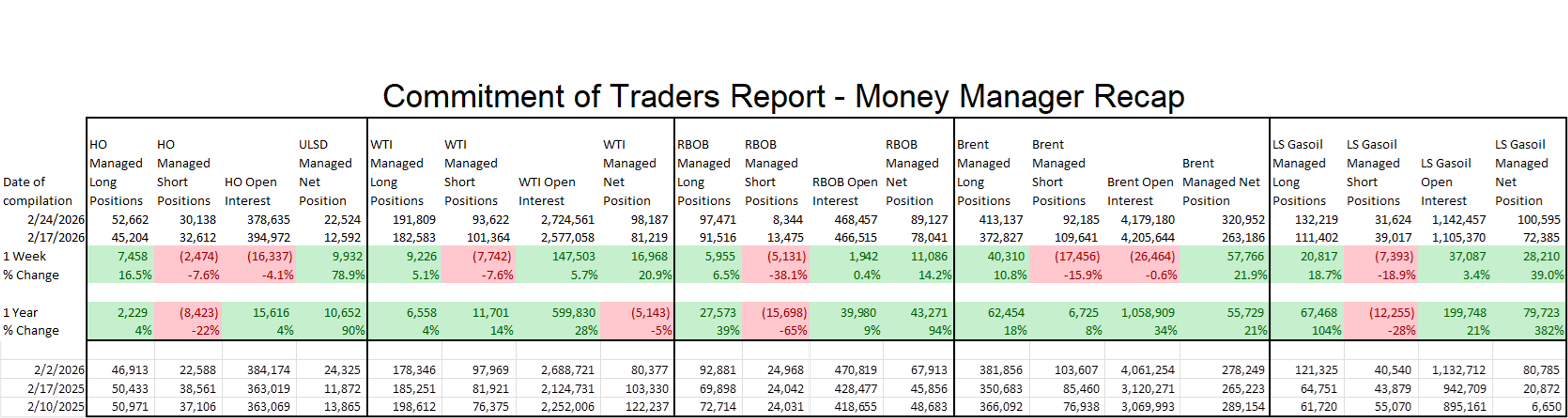

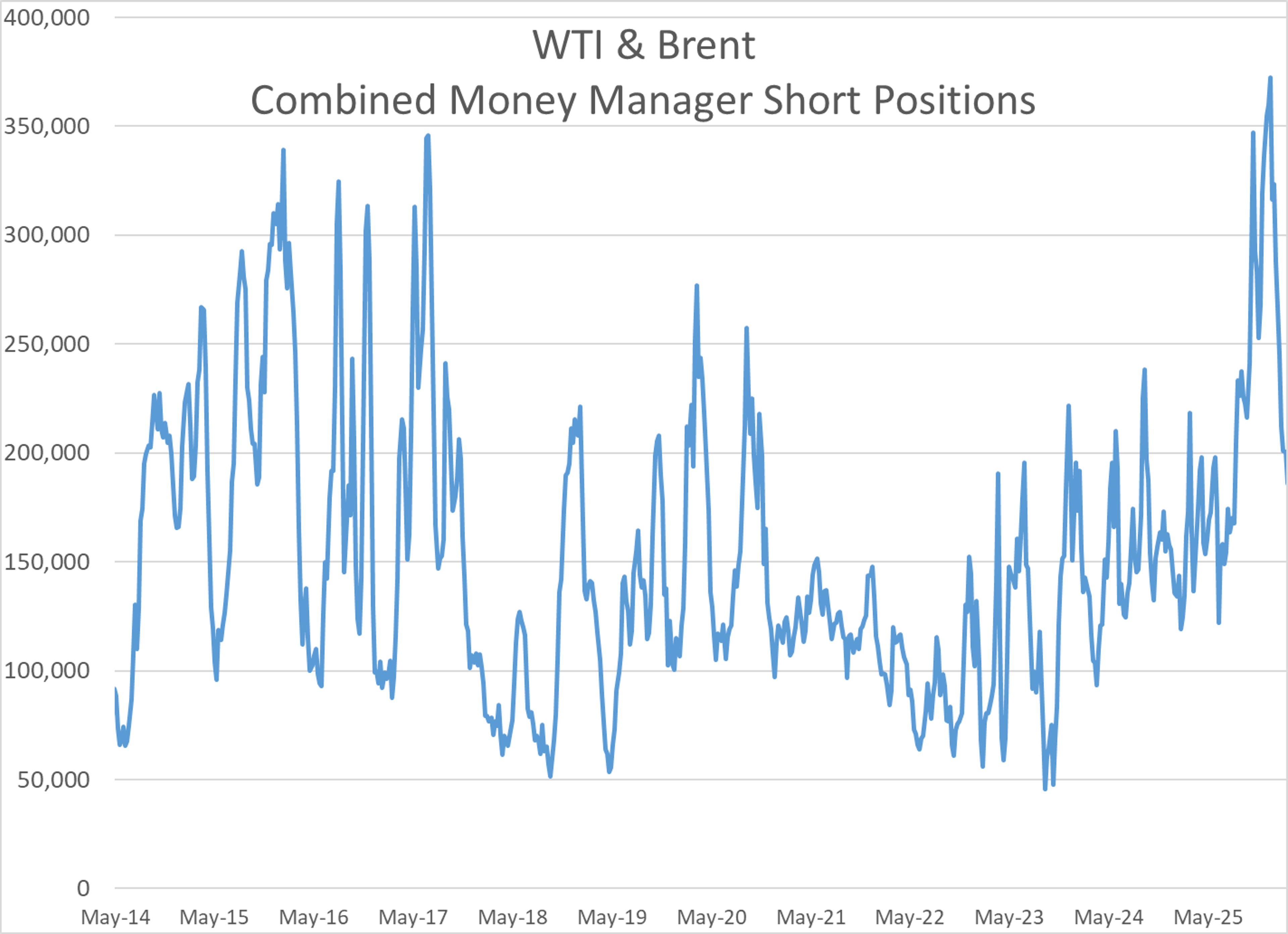

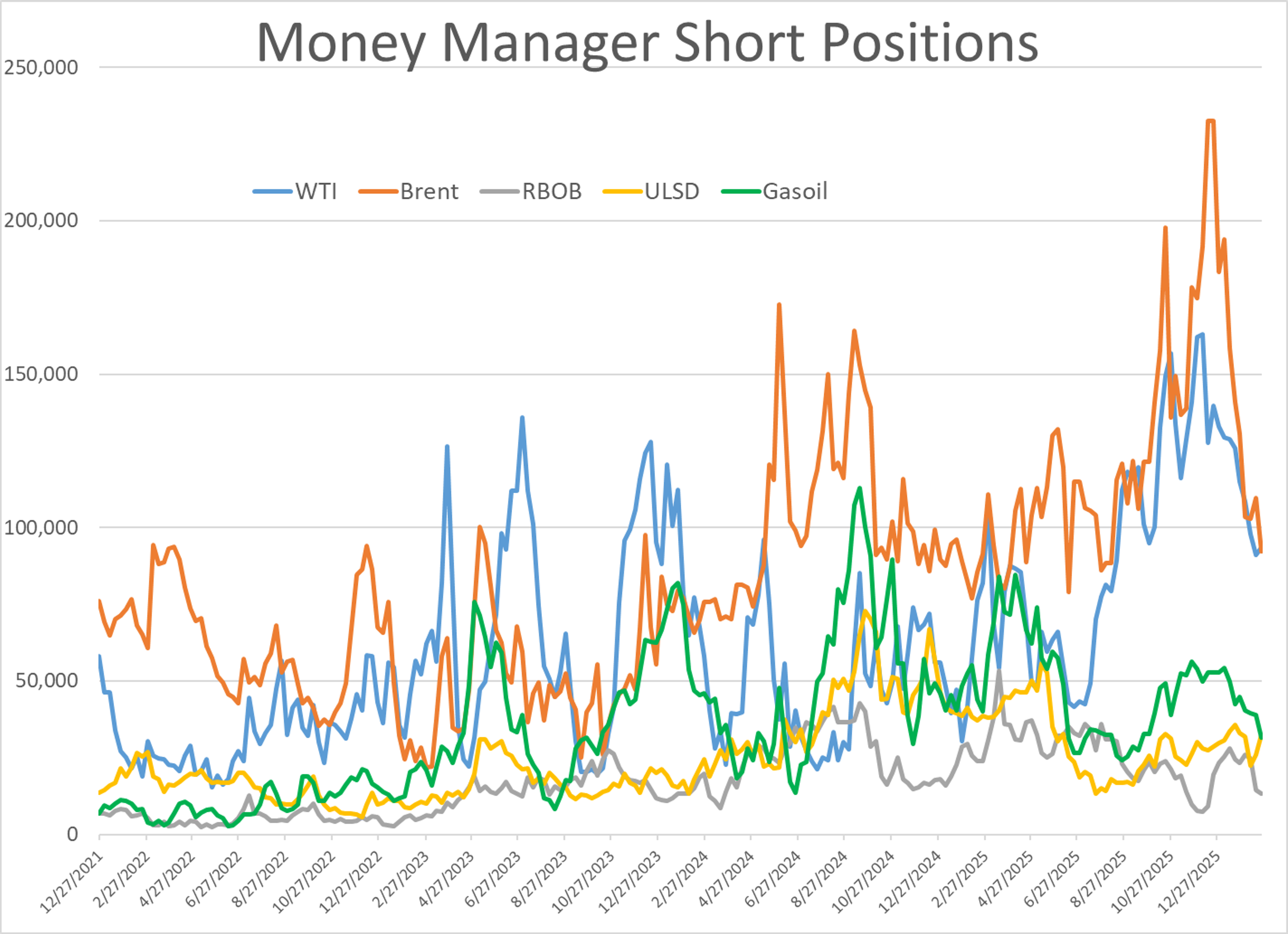

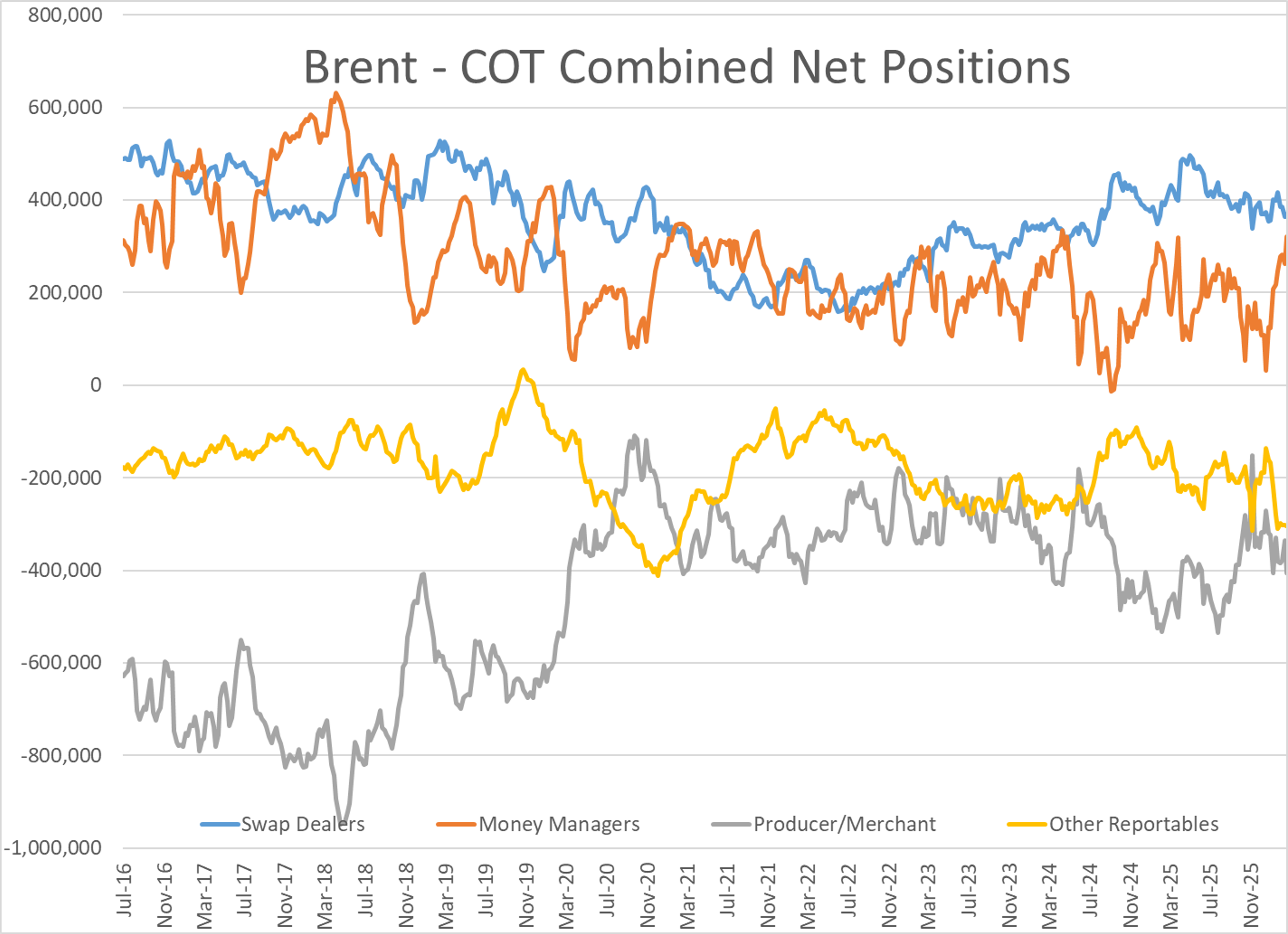

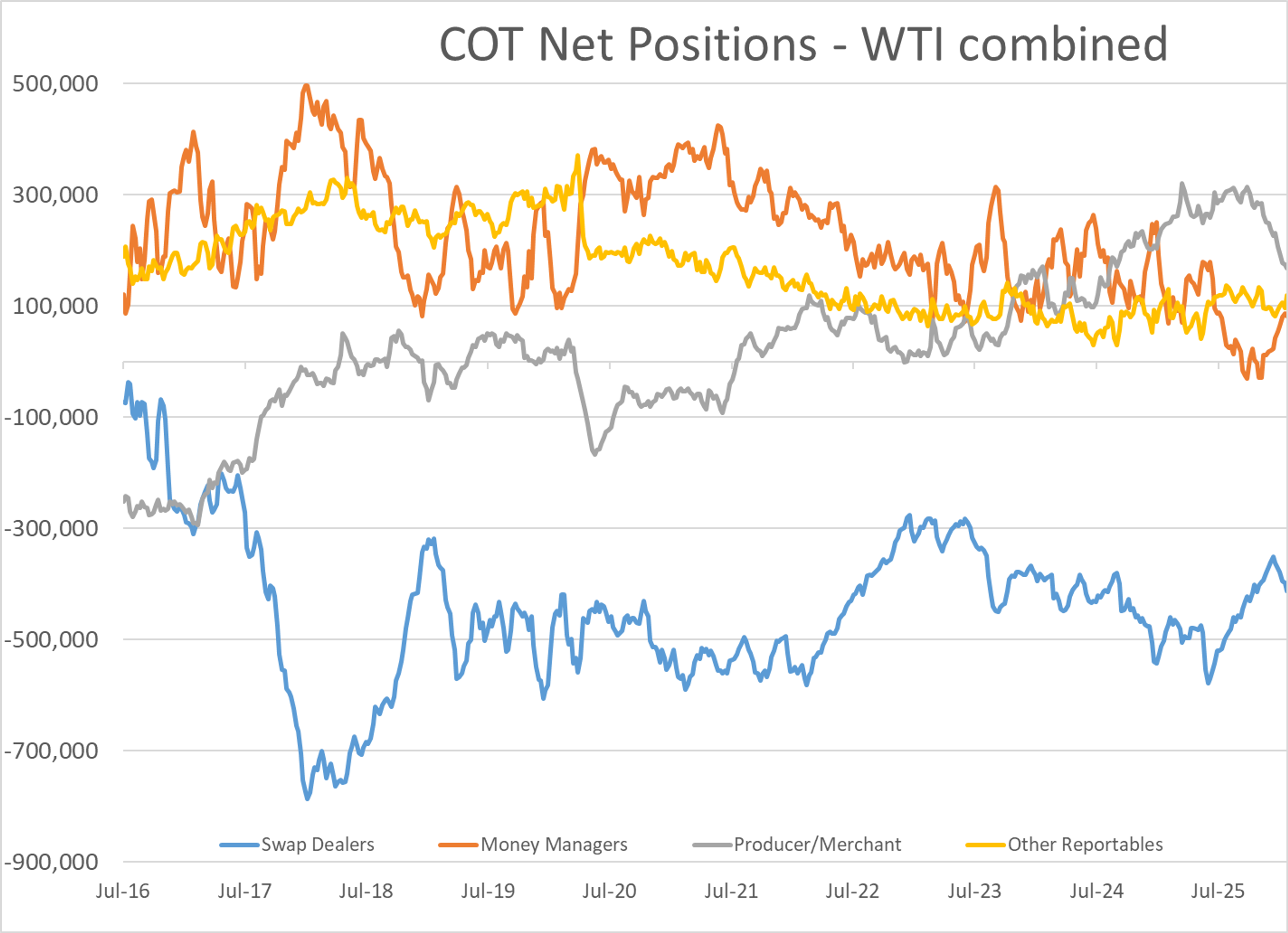

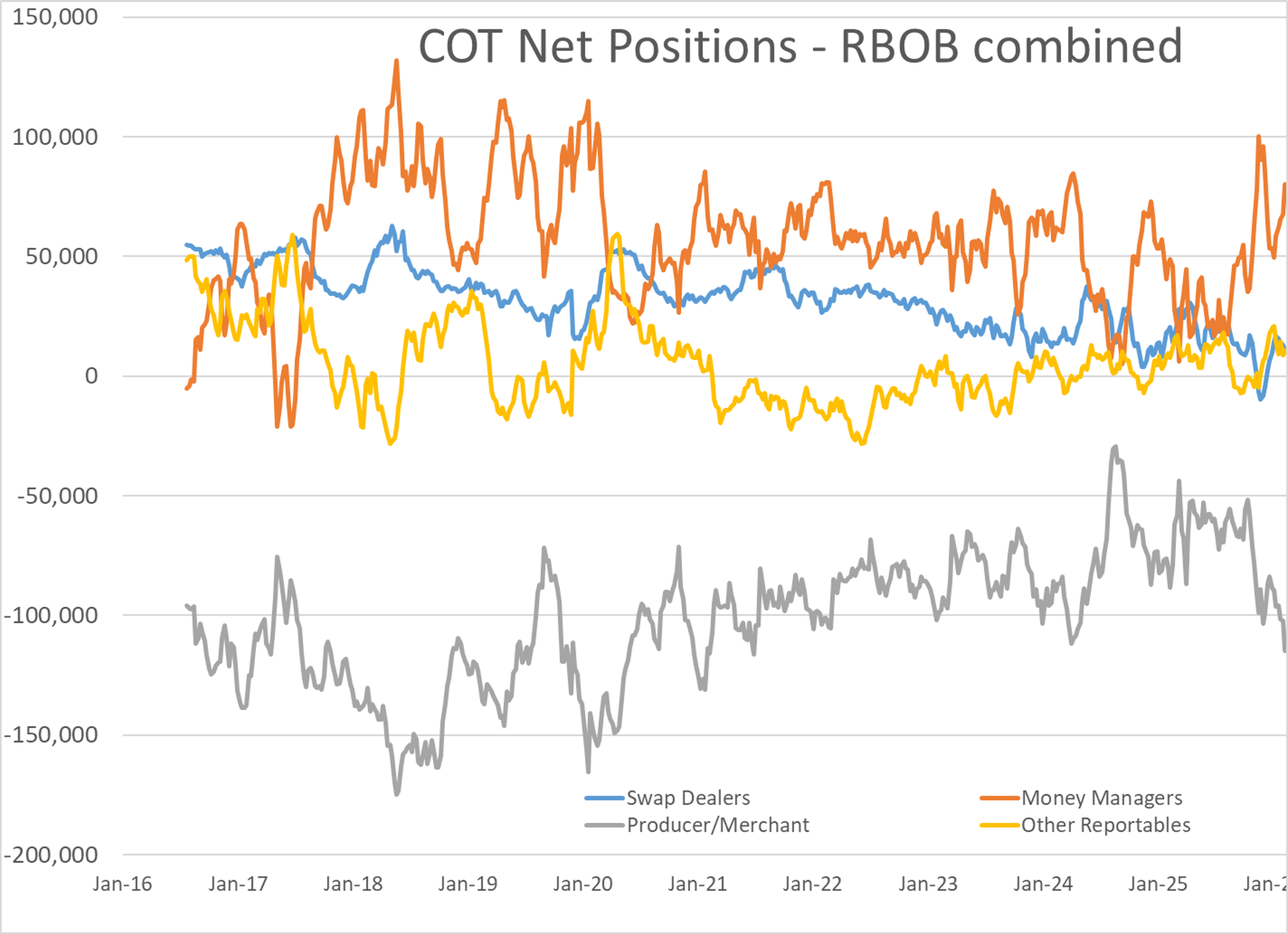

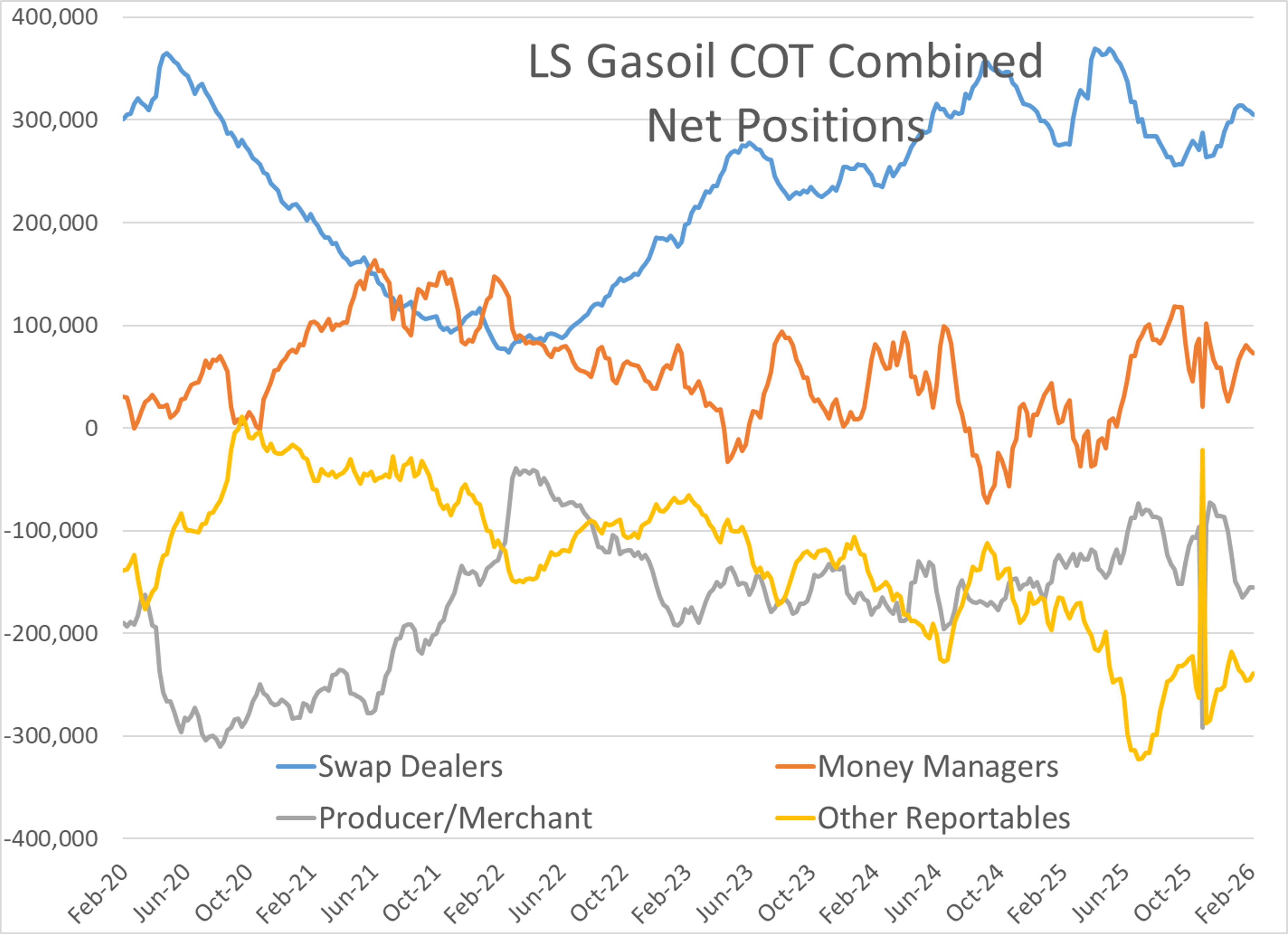

Money managers seemed to have gotten the hint that war was inevitable over the past week, adding to long positions, and continuing to unwind out the “big short” bets on lower oil prices they made late last year as prices reached multi-year lows that had proved a big mistake so far this year. In total across the big 5 petroleum contracts, nearly 124,000 contracts of net length were added to large speculative positions last week, the equivalent of 5.2 billion notional gallons, although overall net length remains modest compared to historical levels, thanks in part to prediction markets allowing Hedge Funds to bet directly on these events, rather than indirectly via the commodities arena with its pesky rules and regulations.

Latest Posts

Gasoline Surges As Global Energy Risks Return

Week 28 - US DOE Inventory Recap

Oil Extends War Premium Gains Amid Ongoing US-Iran Hostilities

Energy Rally Gains Steam As Global Supply Chain Pressures Mount

Energy Markets End A Wild Week With More Questions Than Answers

Middle East Tensions And Russian Export Ban Rock Energy Markets

Social Media

News & Views

View All

Gasoline Surges As Global Energy Risks Return

Week 28 - US DOE Inventory Recap