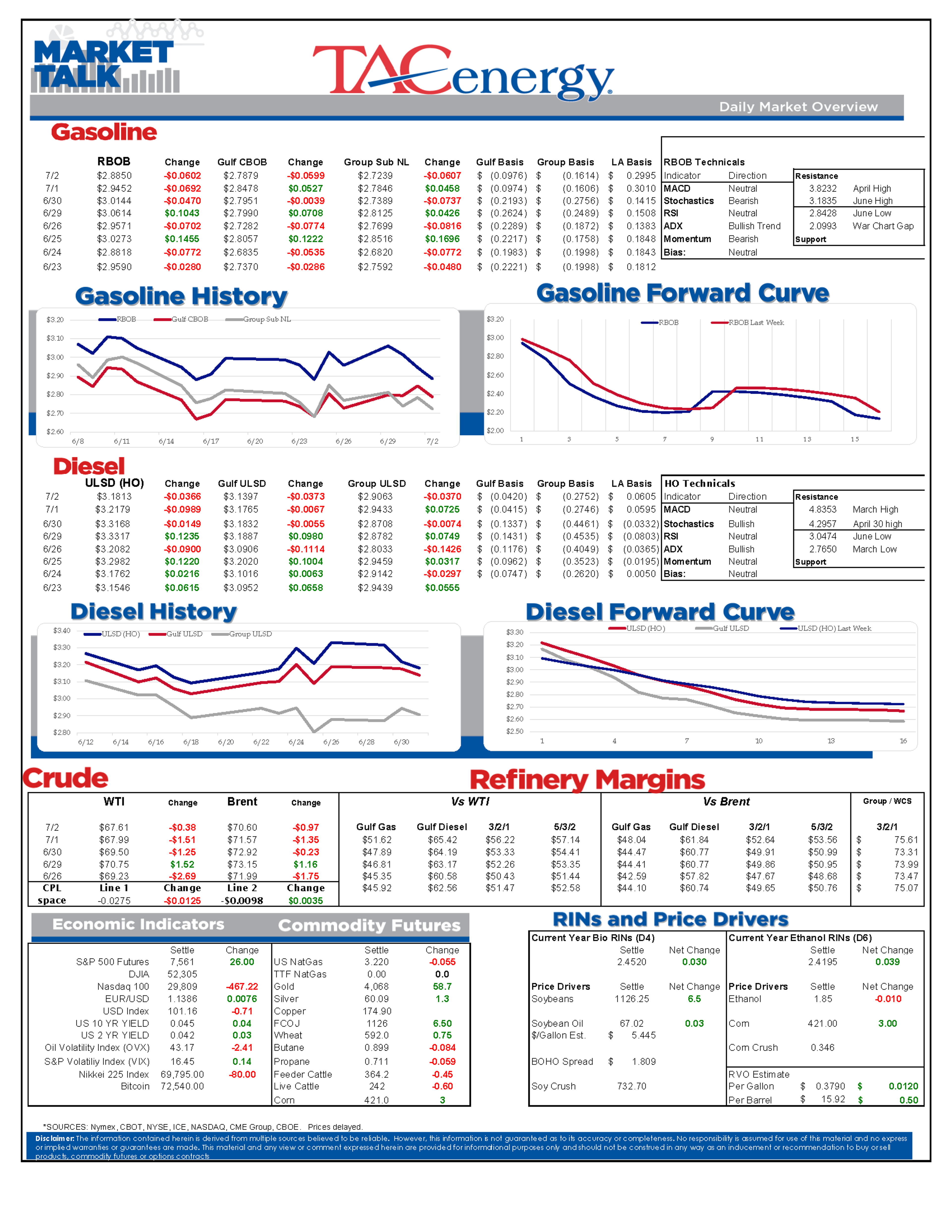

Crude Retreats Ahead Of Holiday Weekend Despite Tight US Inventories

Energy markets are slipping lower as we head into a long weekend in the U.S., as the Middle East belligerents have managed to go 4 whole days without shooting at each other. The U.S. and Iran are said to have agreed to more in-direct talks on the technical nature of the fragile cease-fire agreement, although publicly the two sides remain at odds over how the Strait of Hormuz is actually supposed to work.

WTI traded down to a low of $67.04 overnight, the lowest level since February 27 (the day before the war broke out) which officially closes the gap in the chart left when the market spiked to begin March trading. Refined products have been outperforming crude oil futures for most of the past two weeks thanks to a rash of refinery issues, but RBOB gasoline is leading the slide this morning and is just a few cents away from testing its June lows.

While most offices will be closed in the U.S. tomorrow, futures will trade in an abbreviated session, halting at noon, but won’t post a settlement. Spot markets will not be assessed so formula pricing will carry through until Monday while rack postings may change particularly if there’s a big move in futures in the morning.

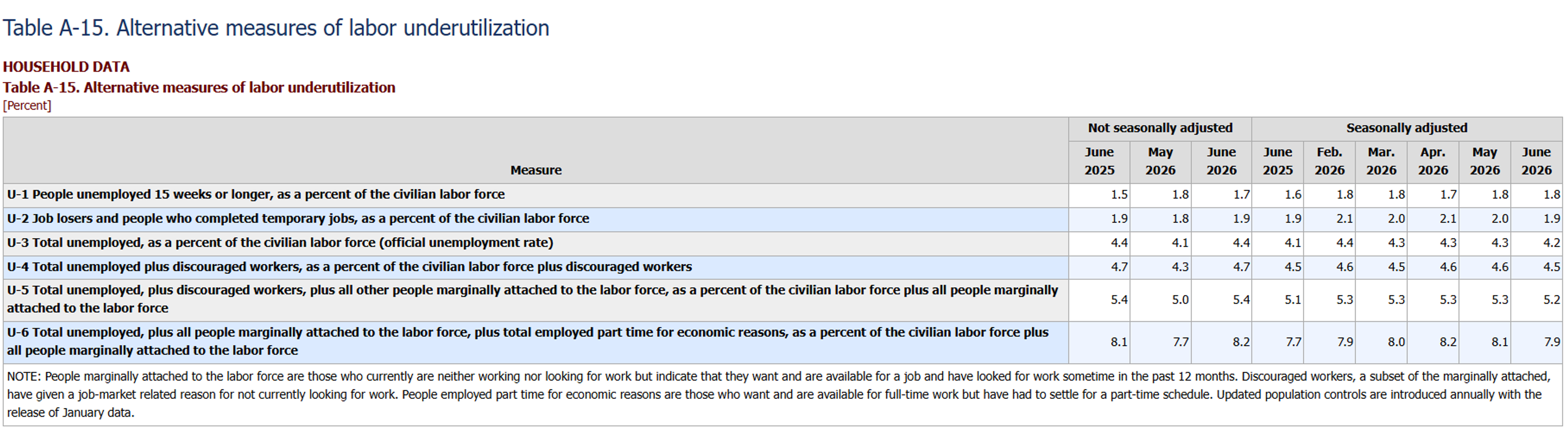

The June jobs report showed a slowdown in hiring activity with the government estimating a 57,000 job increase for June, while the April and May estimates were revised lower by a combined 74,000 jobs. The headline unemployment rate (“U-3”) ticked down by a tenth to 4.2% last month, while the less-manipulated “U-6” unemployment rate ticked down 2 tenths to 7.9%.

Human analysis of the DOE’s weekly report below. Charts and AI analysis are attached.

Crude stocks declined for a 10th straight week with demand for refined products moving above average while imports dropped to a 34-year seasonal low. The draw was tempered by exports falling back into the 5-year range after spending a couple months at seasonal highs, one of which set an all-time high. The SPR sank to a fresh seasonal low leaving total U.S. crude stocks sitting at their lowest levels since 1983, which was less than 6 years from when the SPR took on its first barrels. The big drop in import and export activity for oil and diesel may be temporary due to the severe weather that swept the Gulf Coast two weeks ago, and if that’s the case we should see a large correction in next week’s figures. U.S. crude production is holding near record highs (for any country, ever) and expectations are that output should continue ticking higher following 2 months of slow but steady increases in rig counts and fracking crews.

Refinery runs saw a net increase with large declines in PADDs 1 & 5 being offset by healthy increases in PADDs 3 & 4. PADD 1 slipped from the high end of the range to the bottom over the past two weeks with Monroe Trainer’s being forced offline, then their cat cracker catching fire during their restart attempt, which will remain offline for the next several weeks for repairs. PADD 3 rates climbed to a new seasonal high with Marathon restarting their 160 mb/day cat cracker at the Galveston Bay facility and resuming planned rates last week. PADD 5 slipped to a 6-year low for June after a month of consecutive increases thanks to the PBF Martinez facility finally coming fully back online while PADDs 2 & 4 are operating at seasonal highs. Total U.S. run rates are still tracking just ahead of year ago levels.

Diesel inventories managed to build despite the data suggesting otherwise, aided by export activity falling back below average. PADD level stocks are all still holding below average despite most increasing on the week, with another glut of supply building in PADD 2 after 5 straight weeks of gains which helps explain the arb windows from the middle of the country to the coasts reopening. PADD 5 inventories meanwhile built to a seasonal high when factoring in the latest renewable diesel totals, which helps explain the heavy discounting we’re seeing for RD along the West Coast that’s backing up barrels into other parts of the country. RD inventories (which are still only reported on a delayed monthly basis, not weekly) slipped in PADDs 1, 2, & 4 (although the EIA did not report a figure for PADD 1) while PADDs 3 & 5 hit seasonal highs, leaving the total US about 200,000 barrels shy of the seasonal high set two years ago when the $1/gallon blenders tax credit was still a thing.

Gas stocks declined with demand increasing a week ahead of the holiday weekend while exports shot up to a seasonal high and imports held steady at lows last seen in June of 2020. PADDs 1A & B are hovering right around average levels while PADD 1C (Southeast) dipped below the chart range, keeping total PADD 1 stocks just ahead of 2024’s below average levels. PADDs 2 & 3 are both at seasonal lows with PADD 3 sitting at June 2015 levels. PADDs 4 & 5 are just ahead and just behind year ago levels, respectively, with the total U.S. at a 12-year low for June.

Jet fuel stocks hit another new seasonal high with a big drop in the elevated export levels we’ve seen since mid-March and demand holding around the 5-year average. PADDs 3 and 5 built to seasonal highs while the other three declined, substantially in PADD 4. PADD 1 Jet output dropped substantially due to the downtime at Monroe.

Latest Posts

Gluts, Draws, And Disruptions: A Busy Start To July Energy Markets

Week 26 - US DOE Inventory Recap

Tight Inventories And Outages Push Diesel Prices Higher Into June Close

Oil Climbs On Strait Tensions As Cracks Emerge Beneath The Surface

Energy Prices Reverse As Market Shrugs Off Tanker Attack, Focus Shifts To Supply Constraints

Forward Curves Shift As Energy Markets Adjust To Easing Supply Risks

Social Media

News & Views

View All

Gluts, Draws, And Disruptions: A Busy Start To July Energy Markets

Week 26 - US DOE Inventory Recap