Energy Markets Brace For Unprecedented Supply Shock Amid Global Disruptions

Energy markets are ticking modestly higher to start the week, but are well-off their overnight highs as traders weigh the lack of diplomatic progress that assures a short term supply squeeze at a scale the world has never seen before, against the odds that this shock does long term damage to global fuel demand.

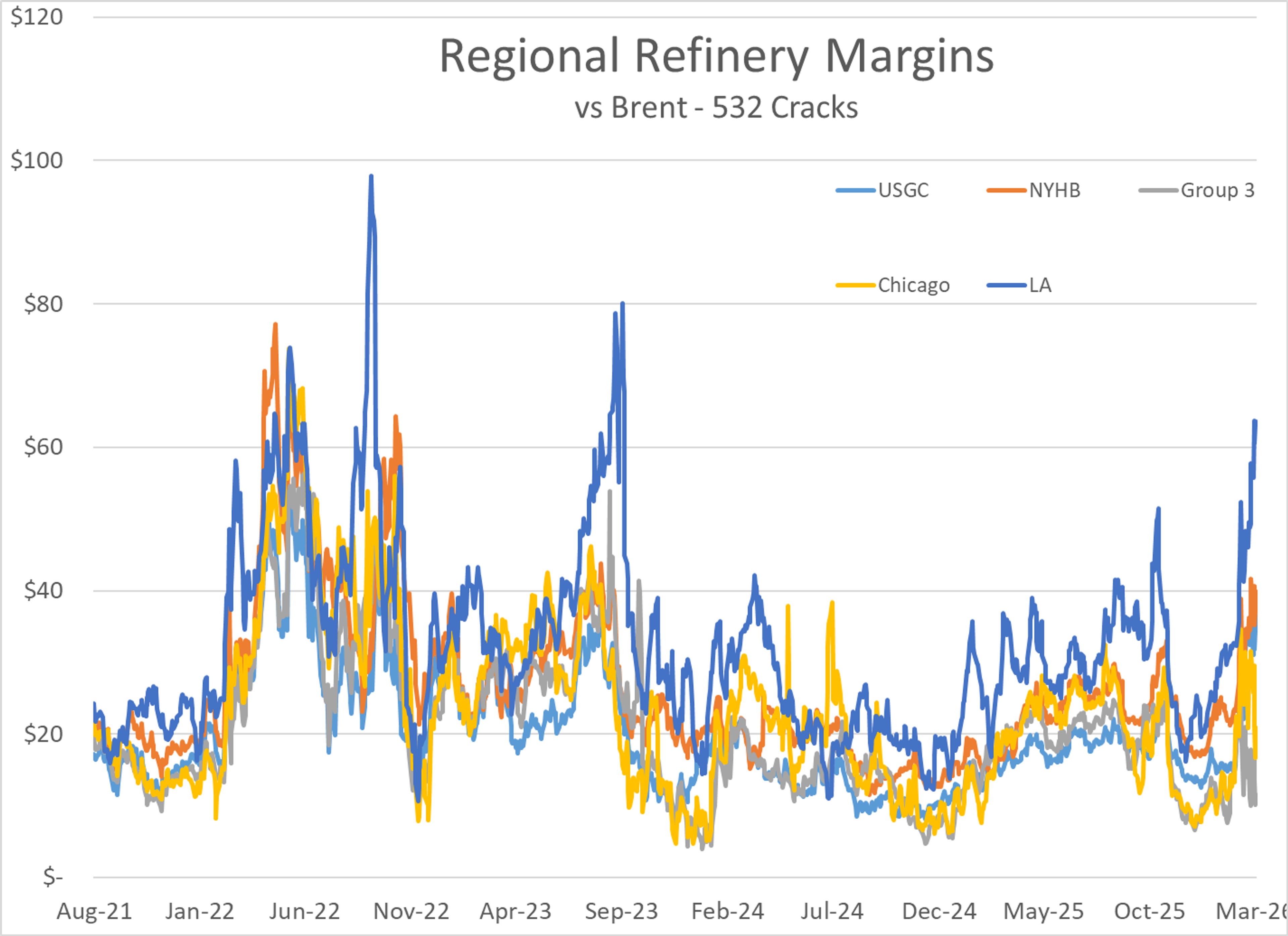

I know a couple companies who may be wishing for a mulligan on their refinery closures: Diesel cracks on the West Coast are approaching $100/barrel as the strength in time and basis spreads puts a huge premium on prompt supplies to supplement desperate countries throughout Asia. Jet fuel differentials are also rallying to record highs as the U.S. becomes a primary supplemental supply option with bidders in Asia and Europe both competing for barrels from the USGC.

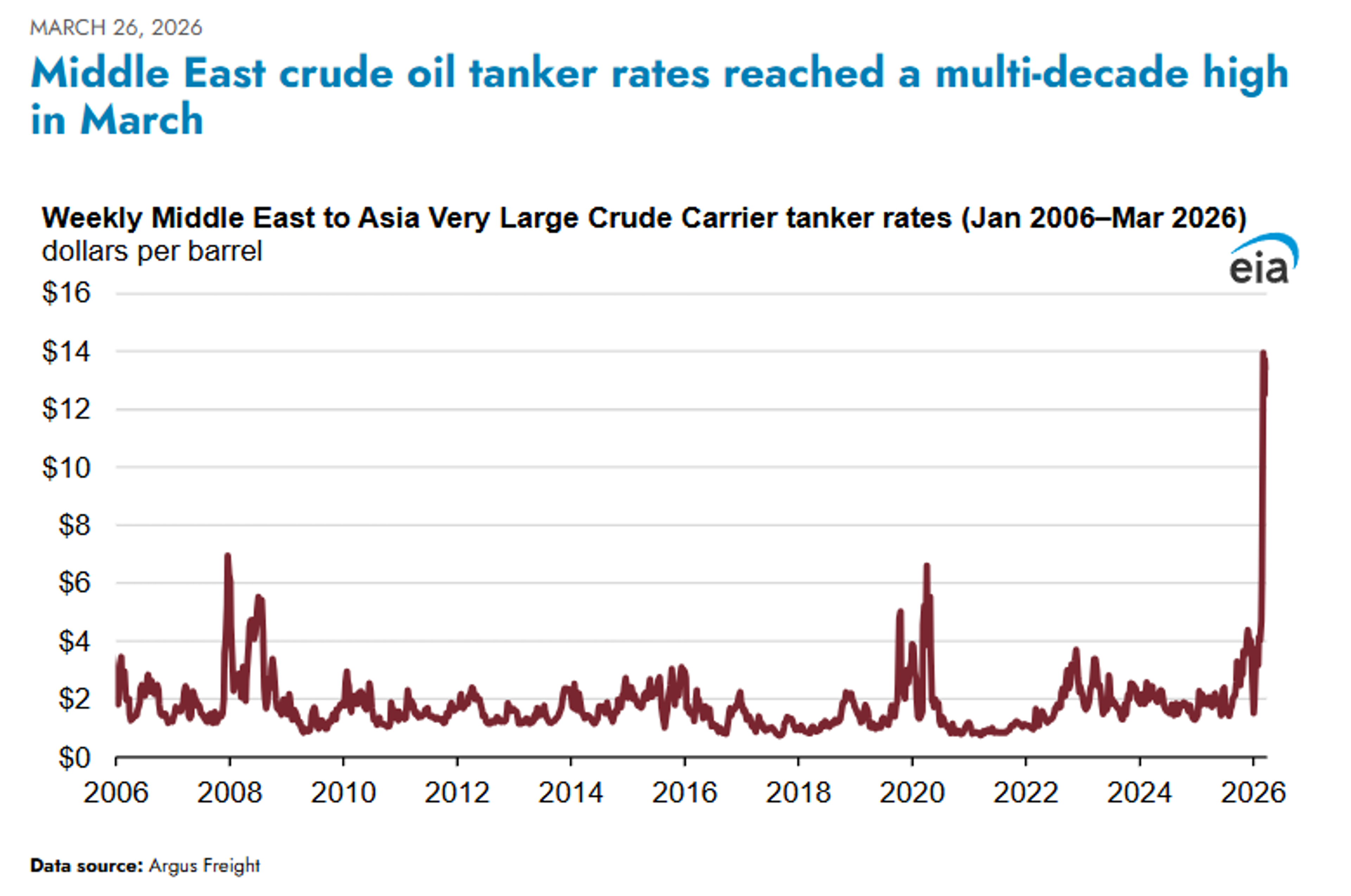

While the U.S. has plenty of refined product export capacity, ship availability is quickly becoming an issue as vessels have to relocate to unusual positions and take longer routes, which is largely negating any positive impacts for domestic markets of the temporary Jones Act waiver.

The EIA this morning highlighted the spike in transportation rates caused by the shutdown of the strait.

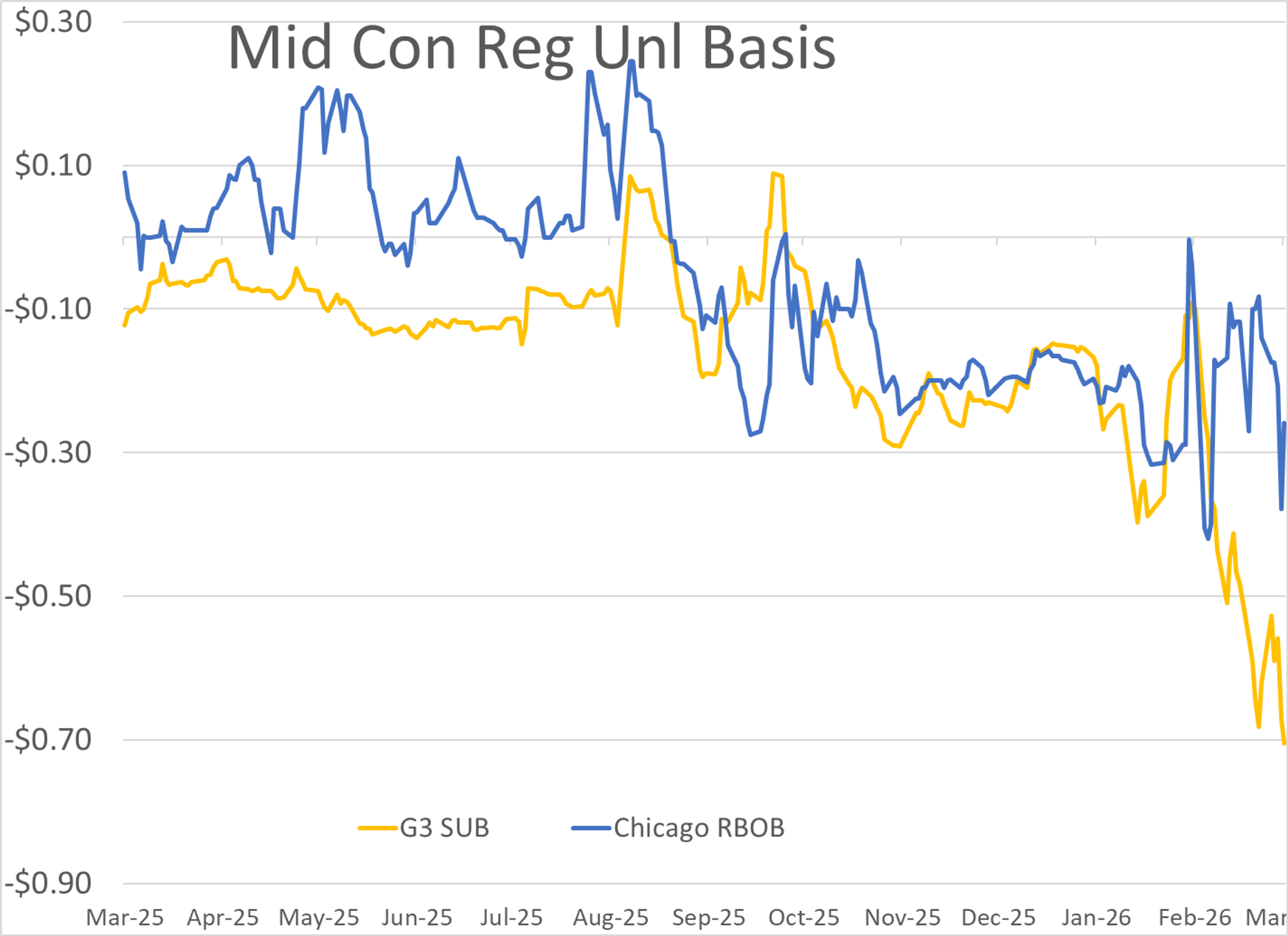

Location, location, location: While coastal markets are seeing no shortage of bidding, the middle of the U.S. continues to see sharply discounted prices as suppliers have few options to move those barrels to higher demand locations. Adding to the challenges, the discounts for Canadian crude oil grades – a key component of profitability for most mid-con refiners – is set to tighten up as more Canadian barrels are bid all the way to the U.S. Gulf Coast to be shipped overseas.

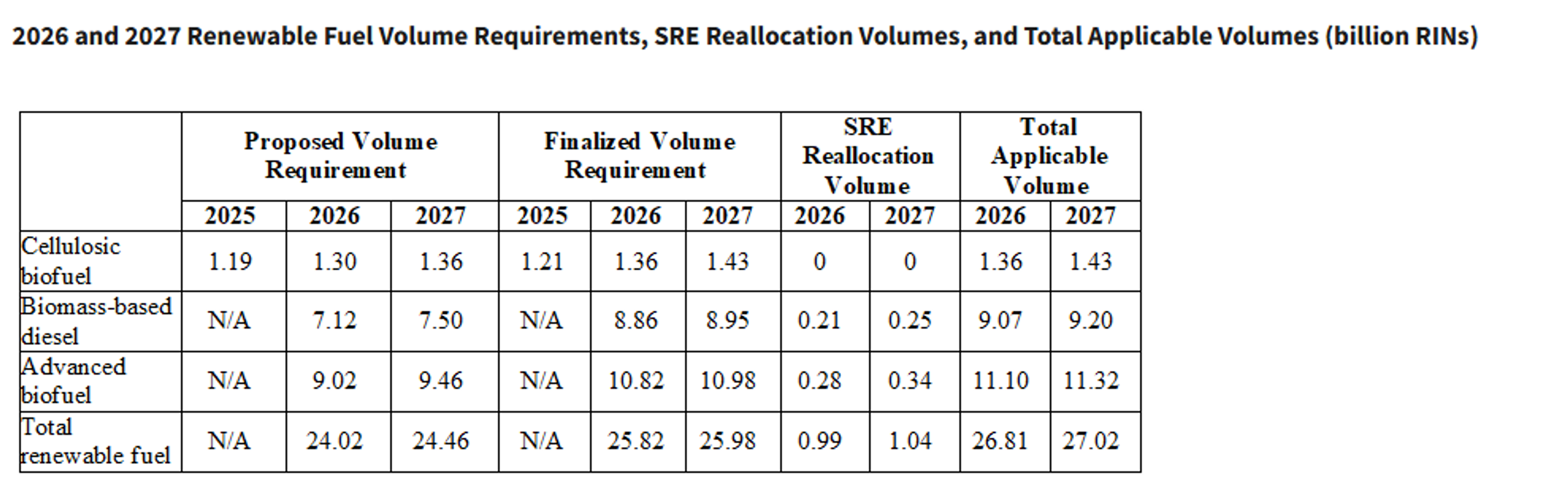

The EPA Friday finally released the final Renewable Fuel Standard policy for 2026 and 2027. The major changes include an increase in bio-mass based diesel requirements (big win for Bio/RD producers) a 70% reallocation of small refinery waiver volumes and a delay in the import penalty until 2028. The new rule also changes the base equivalence value for RD and SAF to 1.5 RINs per gallon, while allowing producers to apply for higher value depending on CI scores, with the rule predicting that most will qualify at a rate of 1.6 RINs/gallon. D4 and D6 RINs had jumped to 3 year highs ahead of the news, and didn’t move a lot after the announcement, although a delay in publishing the full 351 page rule may have contributed to the muted reaction so far.

While the RFS news got the headlines the EPA also announced that it was removing DEF sensor requirements from vehicles due to the huge hassle caused by those sensors malfunctioning. While that ruling doesn’t officially change the DEF usage requirements, it certainly will take away much of the incentive for compliance.

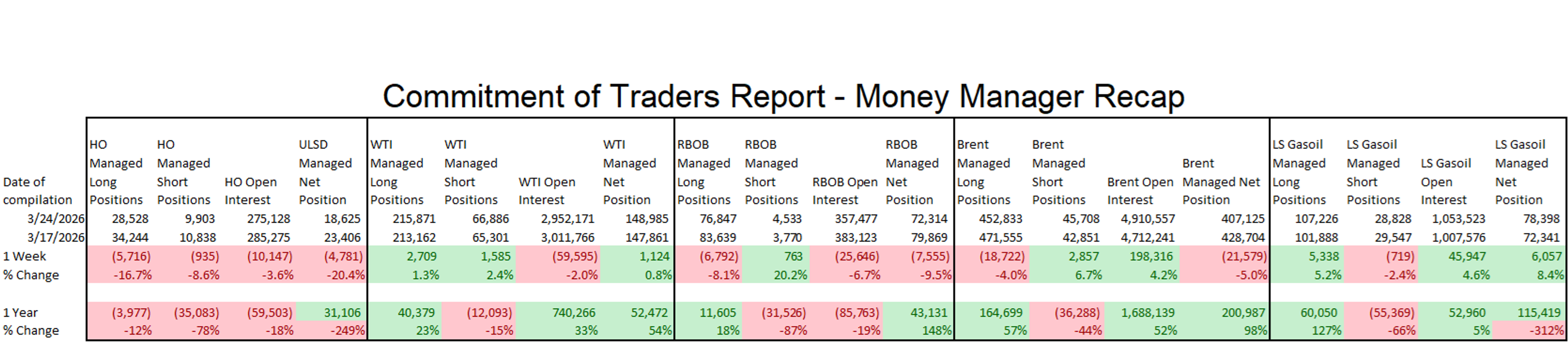

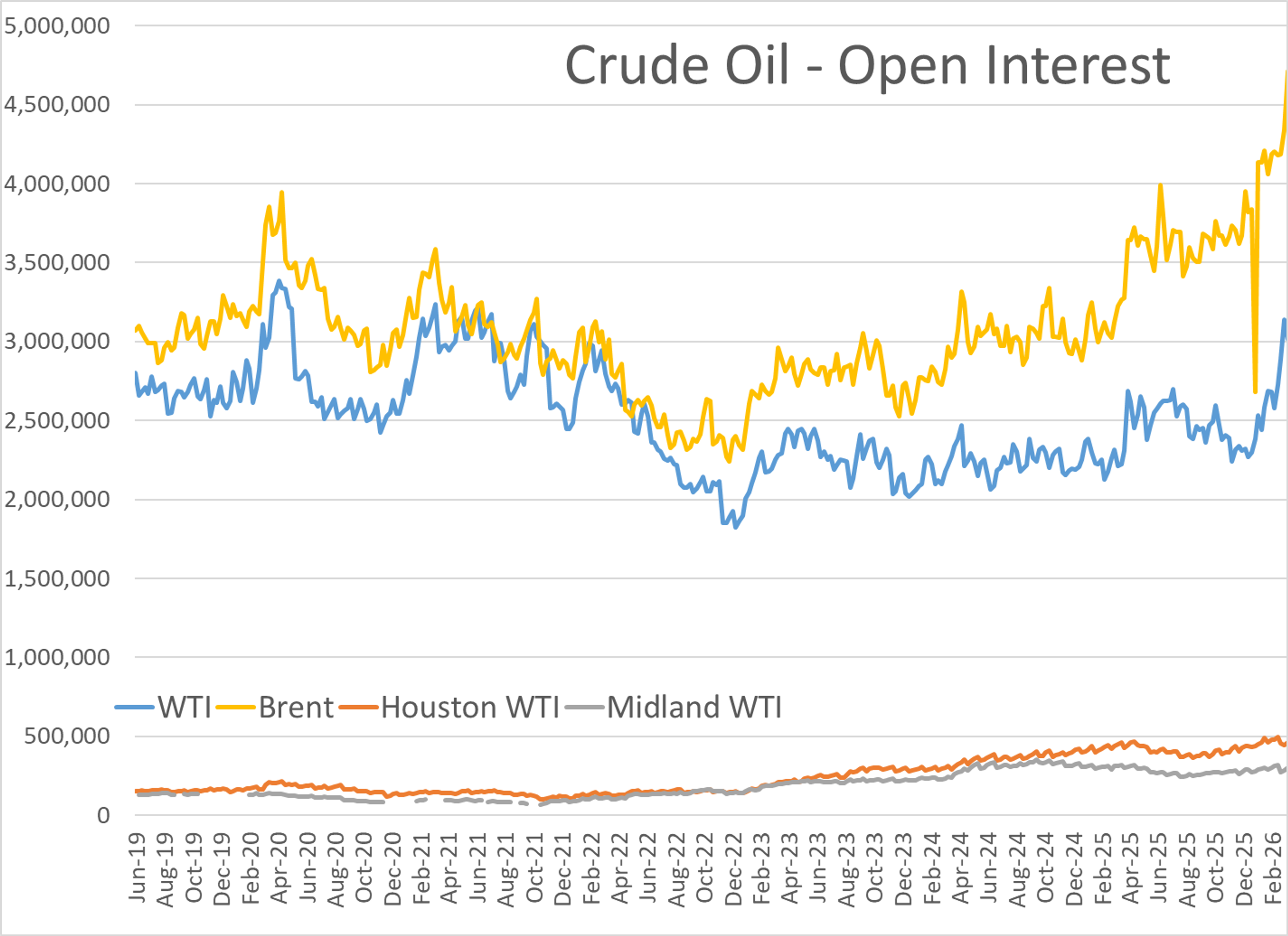

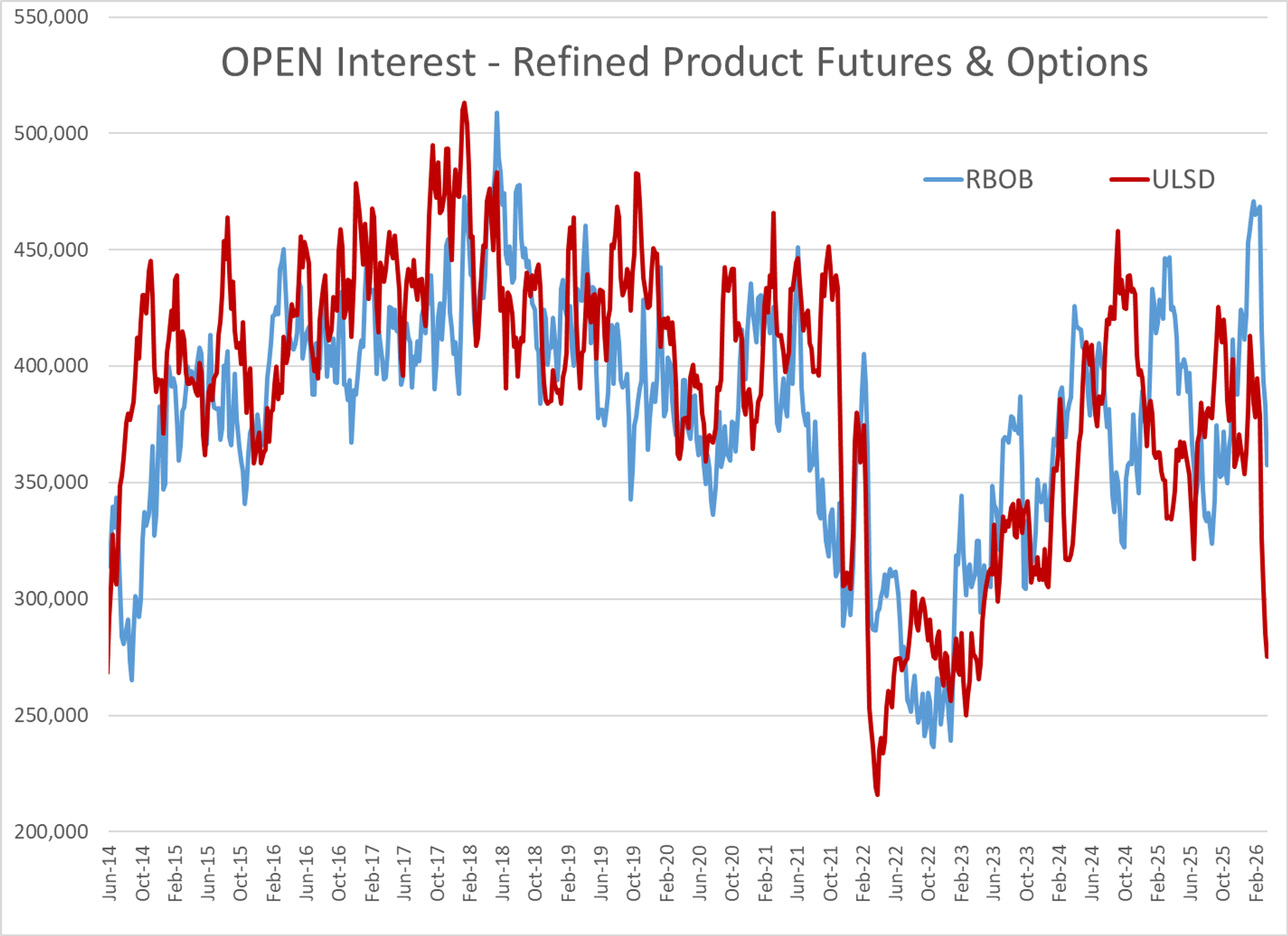

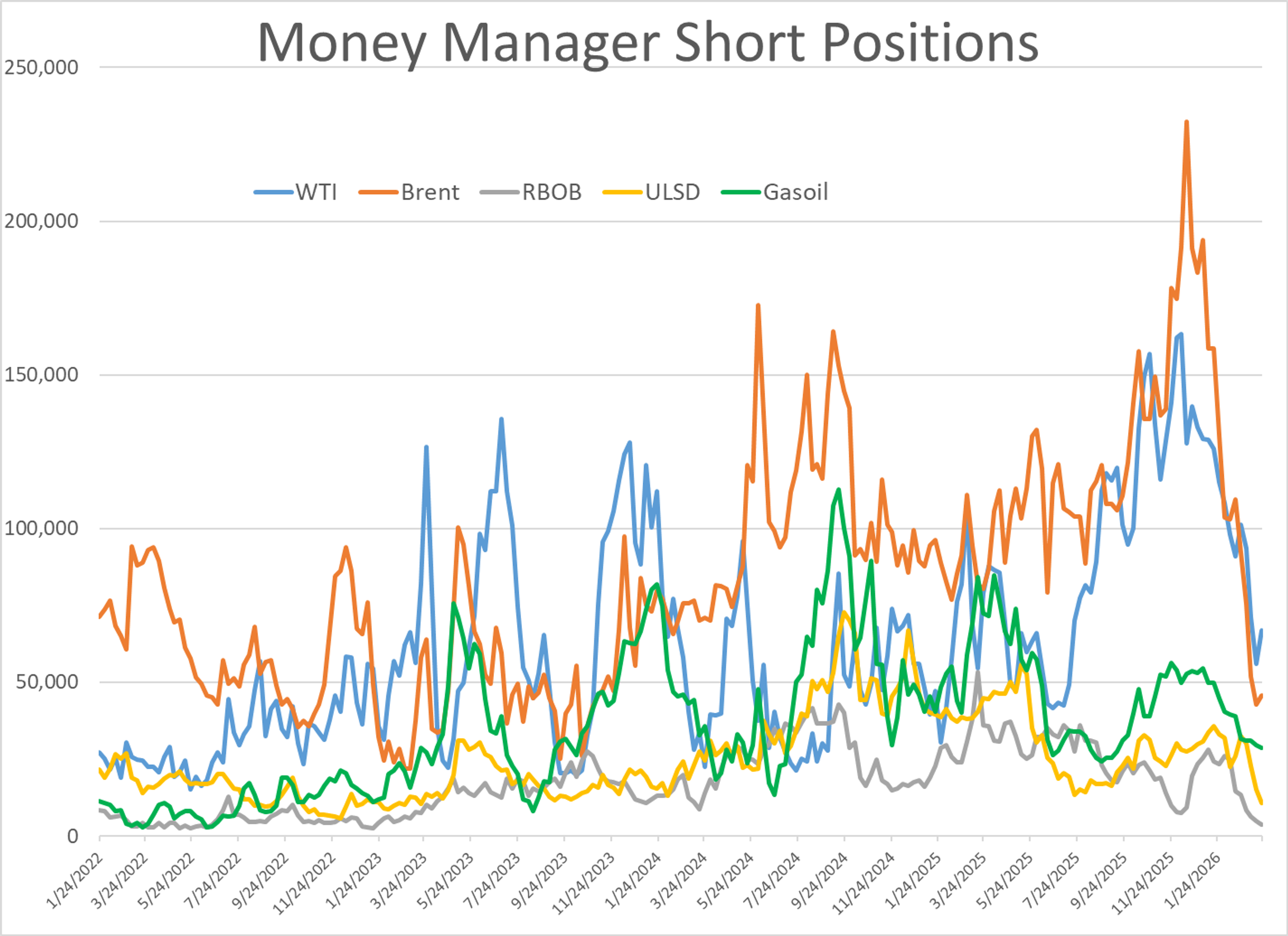

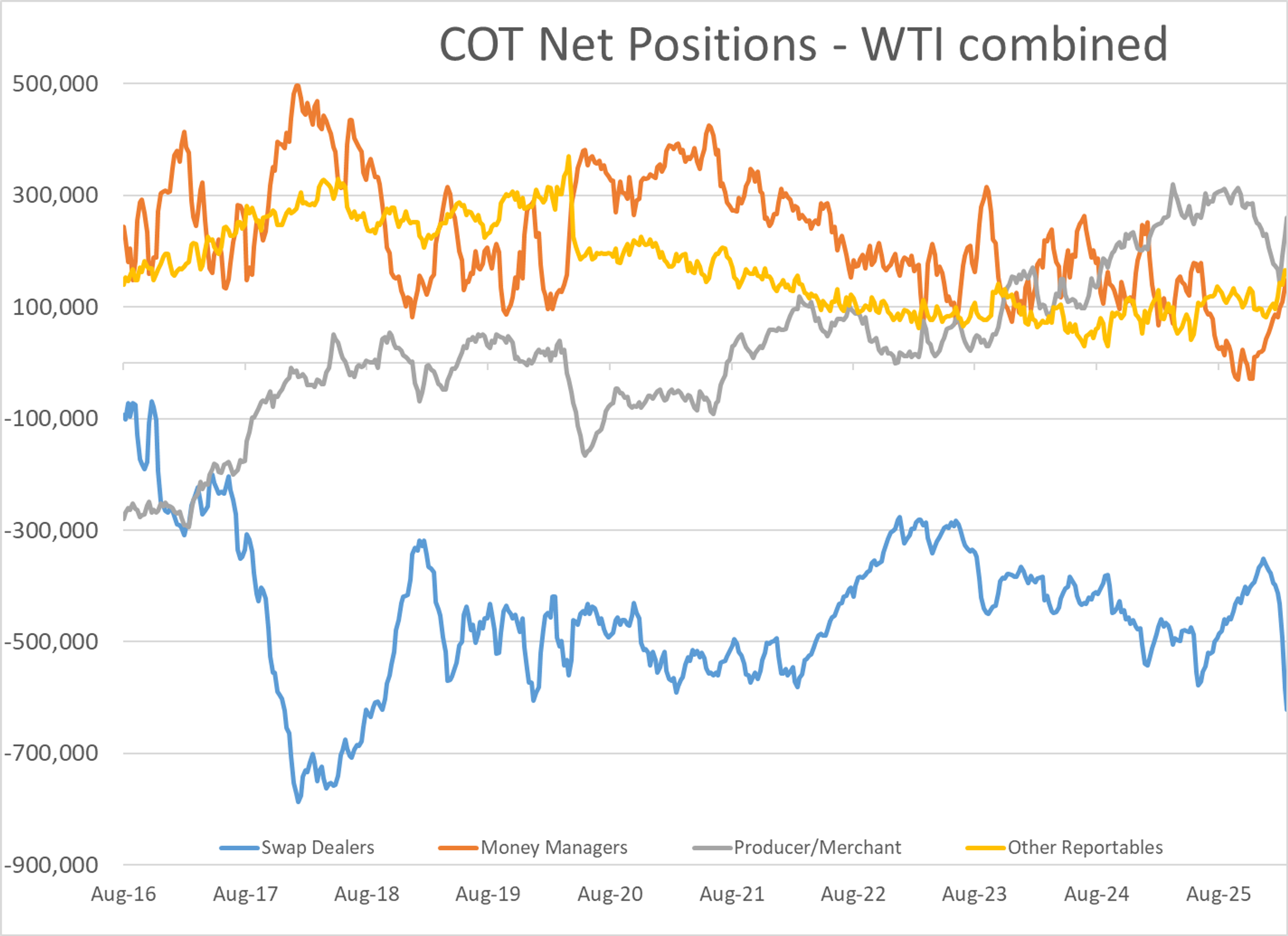

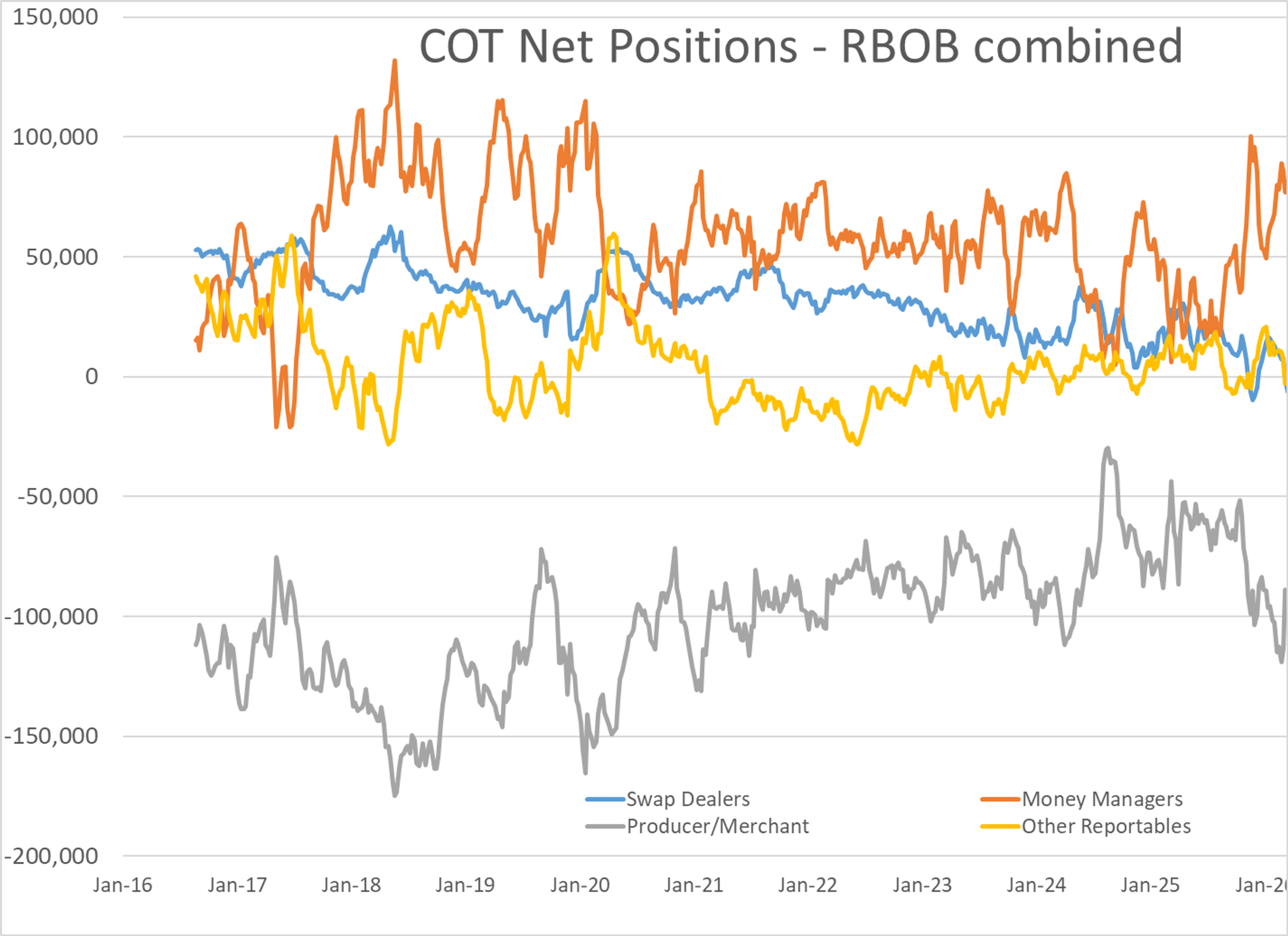

Money managers were a mixed bag last week, reducing length in Brent crude, RBOB and ULSD contracts, while making modest increases to bets on higher prices in WTI and Gasoil. The most notable change since the start of the war has been that volume and open interest in Brent crude has surged (suddenly betting on oil prices is more entertaining than bit-coin and prediction markets) while open interest in refined product contracts has plummeted similar to what we saw in 2022 when a 300% increase in margin requirements from the CME and a spike in volatility made trading too hot to handle for some shippers.

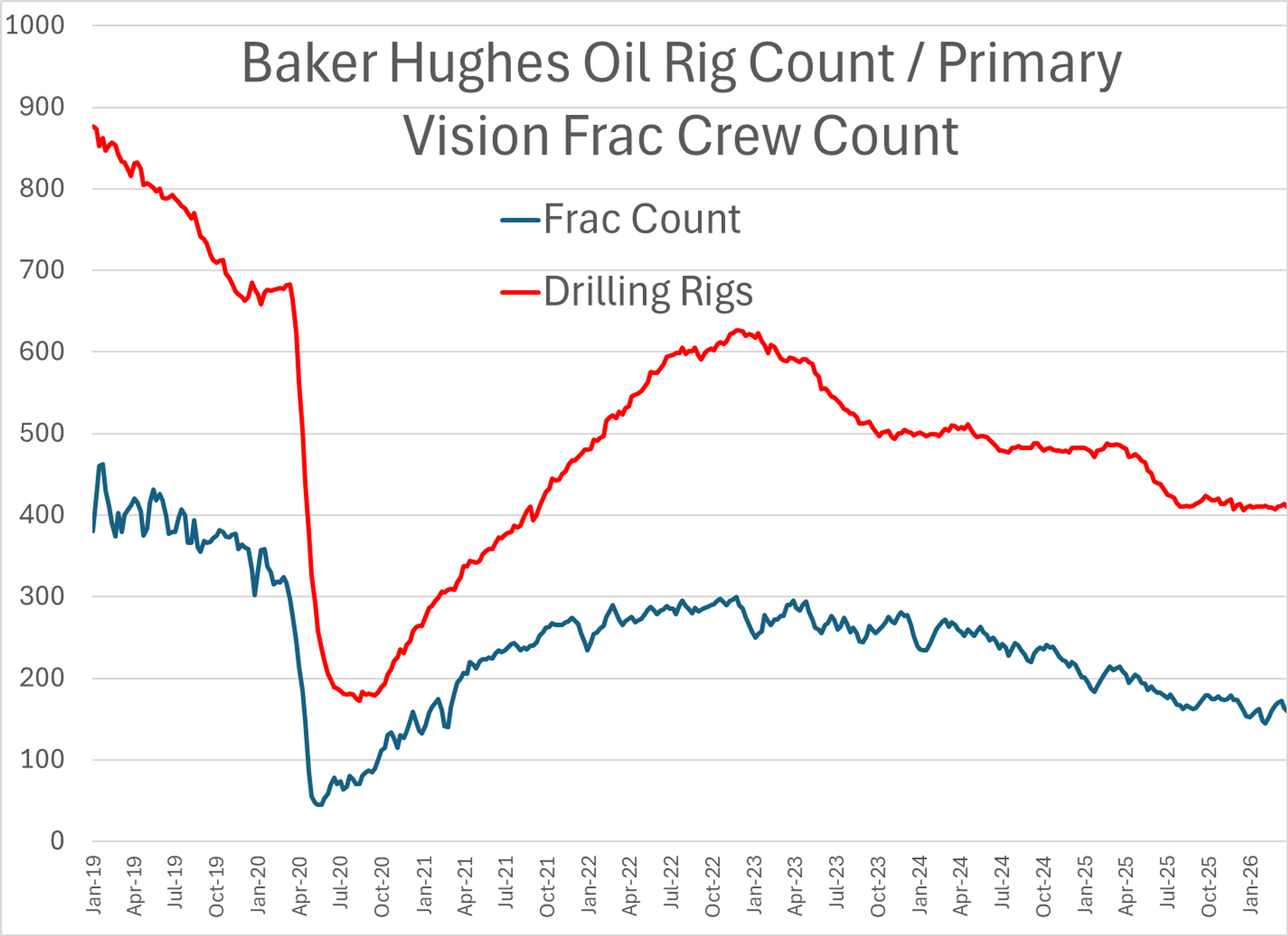

Baker Hughes reported a decrease of 5 oil rigs and 4 natural gas rigs drilling in the U.S. last week, while the Primary Vision count of fracking crews also dropped by 5 on the week.

Latest Posts

Energy Prices Reverse As Market Shrugs Off Tanker Attack, Focus Shifts To Supply Constraints

Forward Curves Shift As Energy Markets Adjust To Easing Supply Risks

Energy Markets Drift Lower Amid Supply Chain Progress

Week 25 - US DOE Inventory Recap

Oil Slides To 3-Month Lows Amid Iran Progress And Renewed Supply Flow

Markets Shrug Off Hormuz Shock As Bears Take Control

Social Media

News & Views

View All

Energy Prices Reverse As Market Shrugs Off Tanker Attack, Focus Shifts To Supply Constraints

Forward Curves Shift As Energy Markets Adjust To Easing Supply Risks