Energy Markets At An Inflection Point: Prices Fall As Policy Pressure Builds

Energy markets are sliding into the red this morning, with progress in the indirect negotiations between the U.S. and Iran getting credit for much of the pullback, while the record setting 37” of snow dumped on New England didn’t create as much in the way of supply disruptions as it did demand. ULSD futures continue to lead the moves in either direction, with the March contract (that expires tomorrow) down more than a nickel for the day and 12 cents from Tuesday’s high, while the April contract is down close to 3 cents for the day. WTI and Brent crude have both given back $3/barrel from the multi-month highs they set earlier this week.

While petroleum bulls seem to have given up the push higher for now, RIN prices shows no signs of slowing down, rallying sharply to fresh 2.5 year highs this morning near $1.58 for D6 ethanol RINS and $1.65 for D4 bio-mass based RINs as the industry awaits the final RFS ruling for the year with several proposed changes still up in the air. There were reports that the EPA was delivering its final proposal to the White House Wednesday, and rumors are swirling that the EPA will be trading the 50% haircut for imported fuel and feedstocks in exchange for a higher bio-mass-based diesel requirement when the final rule is announced by the end of March.

In addition, An “exclusive” Reuters Rumor report this morning citing 3 unnamed sources suggests the administration is preparing to shift 50% of the small refinery exemption volume to large refiners.

If you’re more into numbers than rumors, read this in depth analysis from Scott Irwin at Farmdoc on the potential impacts to the supply pool from the proposed changes.

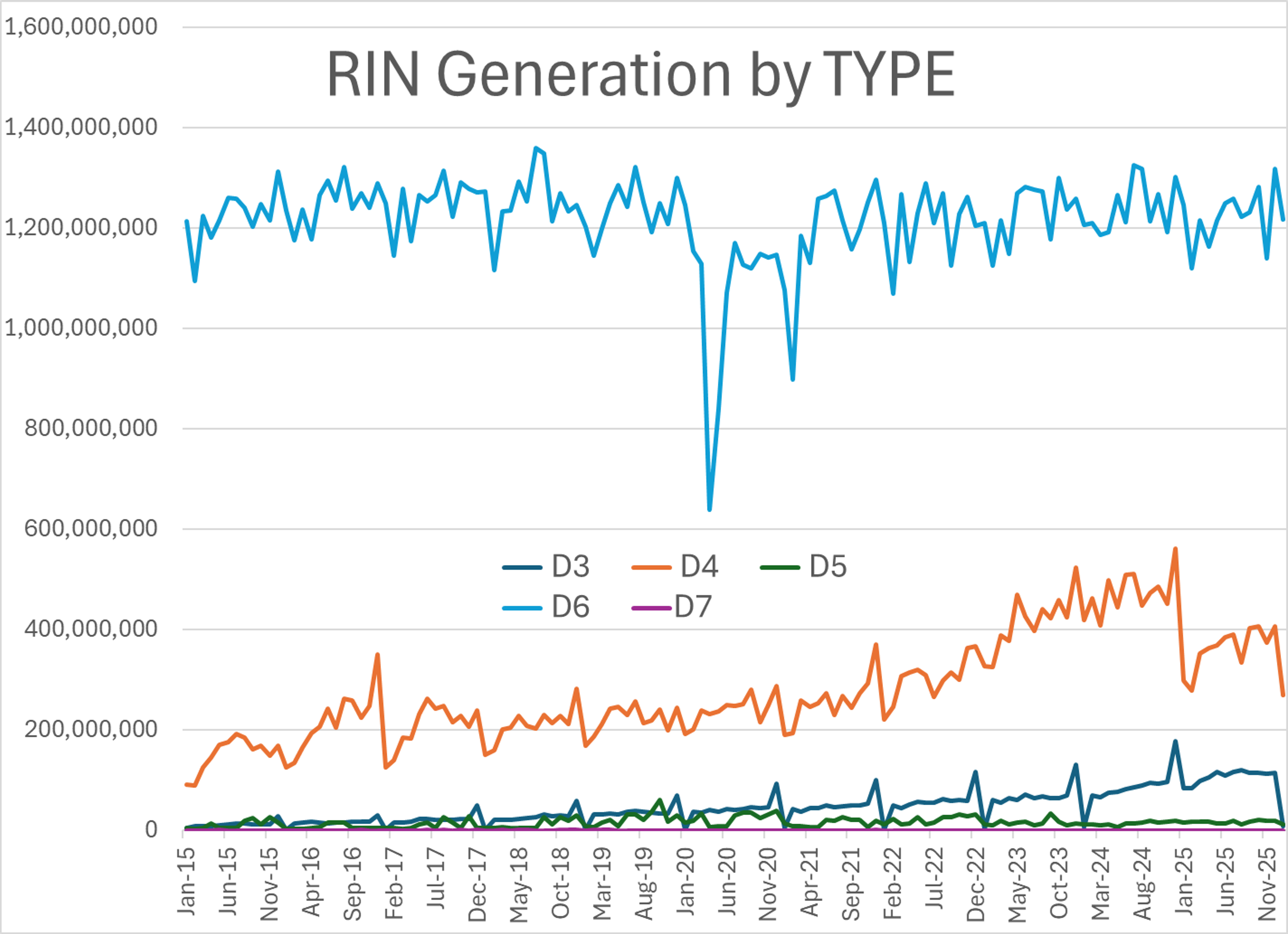

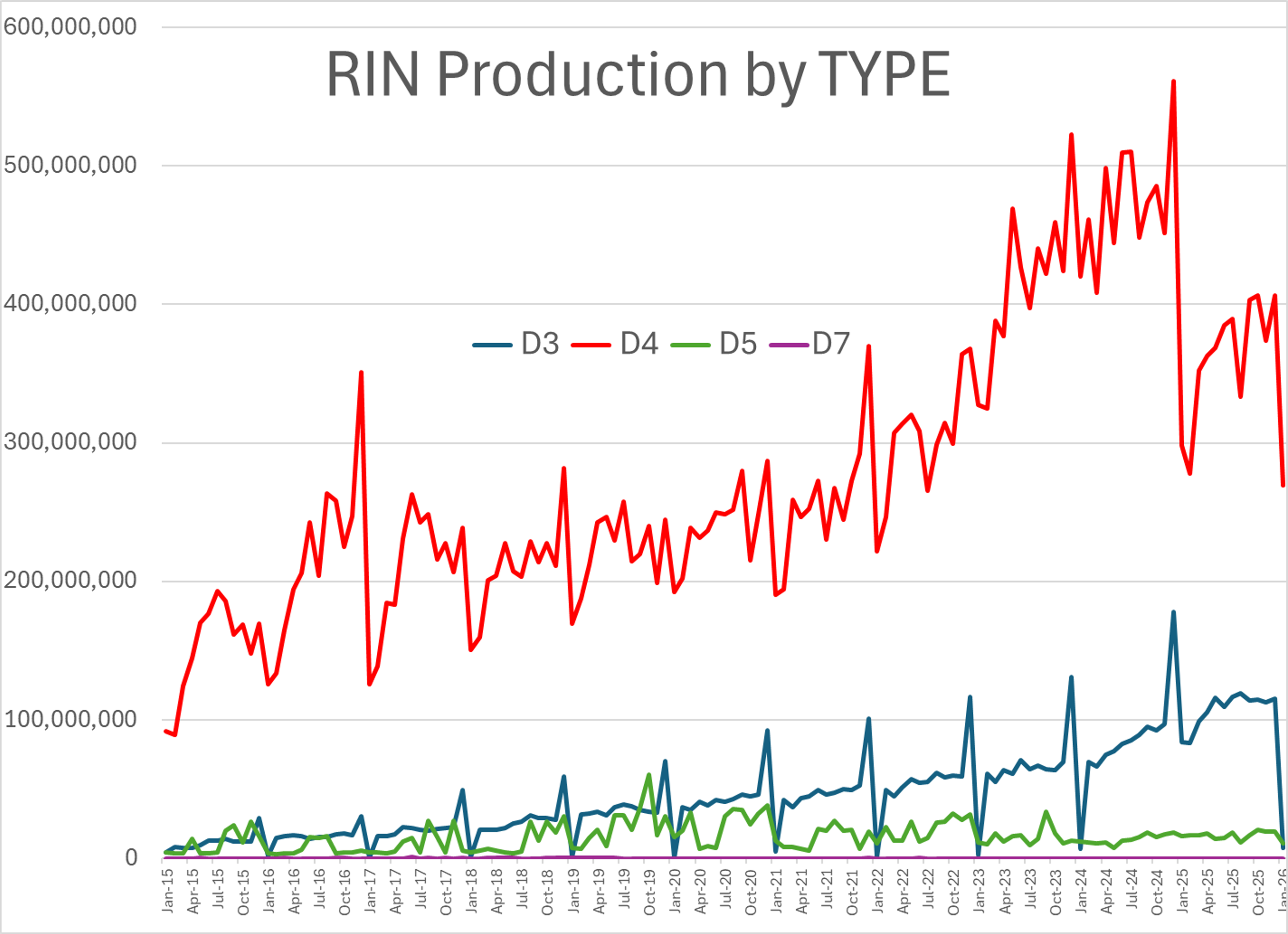

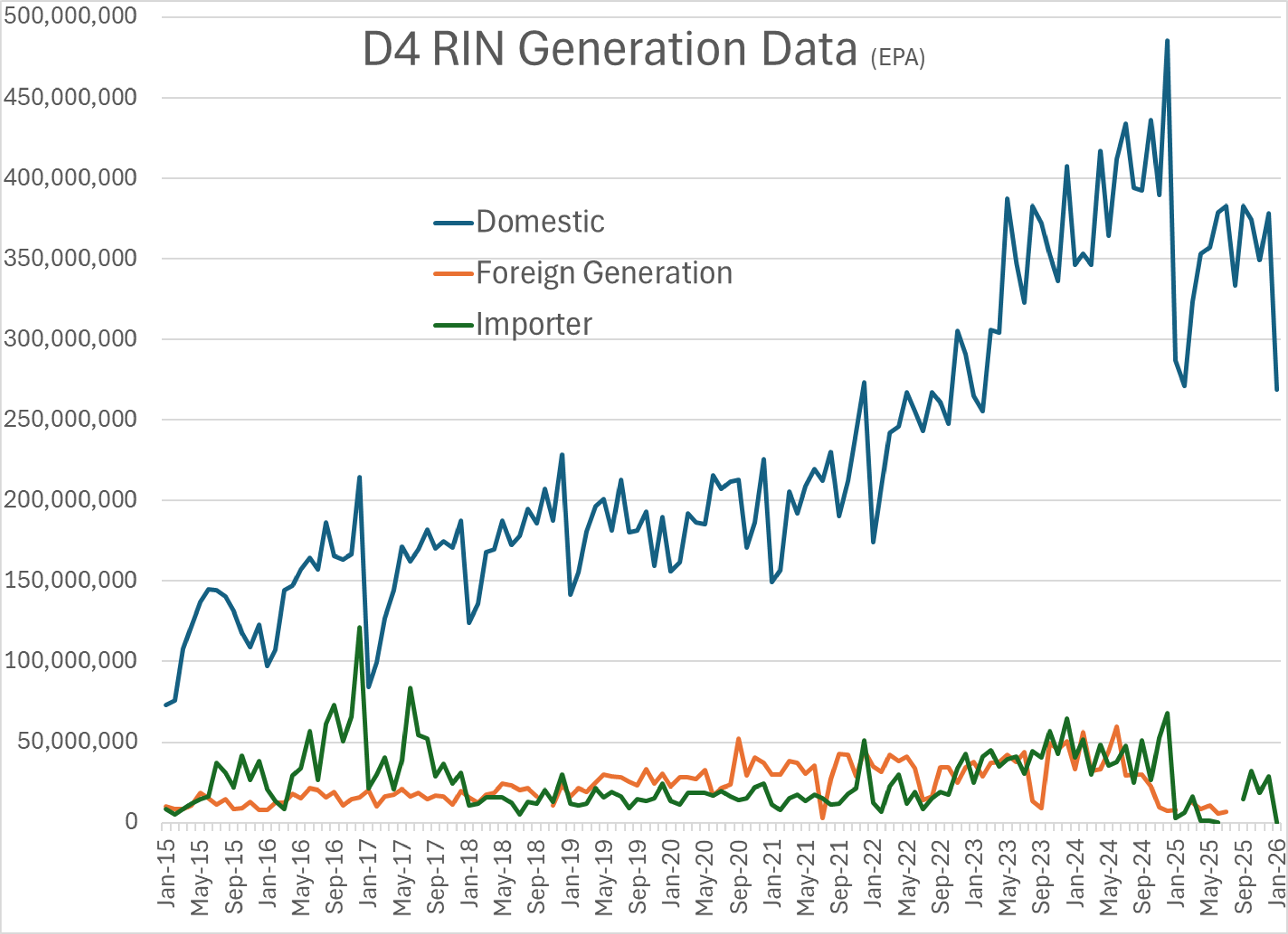

The EPA’s RIN generation data for January showed the lowest D4 RIN generation that we’ve seen in 3.5 years, some of which may be due to heavy maintenance at multiple RD/SAF facilities during the month, but it’s also likely that some producers simply didn’t rush their RINs through the generation process due to the lack of guidance on the law for this year, and we’ll see a big rebound in the upcoming reports.

It’s also worth noting that the RINs generated in January were still using a 1.7 RIN/Gallon ratio for D4 Renewable Diesel, even though the EPA’s proposed rule for 2026 and 2027 lowers that ration to 1.6, which will take roughly 6% of the RINs out of the supply pool even with the same gallons once that rule is finalized.

A day after Flint Hills reported an upset at its Corpus Christi West facility, Citgo reported 2 different upsets in an FCC unit at its 165mb/day Corpus Christi facility, the first occurring Tuesday night and the 2nd Wednesday morning, and both lasting 2 hours. Those upsets appear to be related to the restart of the unit after planned maintenance, so they should not have an impact on regional supplies.

The U.S. treasury is loosening restrictions on oil imports into Cuba, offering a licensing policy that would allow applicants to apply to deliver fuel from Venezuela, which was the primary supplier to the nation prior to this year’s regime overhaul.

Notes from the DOE’s weekly status report: See charts attached.

Crude stocks built substantially with positive import/export flows, and a healthy reduction in refinery runs, but the massive swing in the adjustment factor added the bulk of the 16-million-barrel increase.

Total U.S. refinery runs fell back into the 5-year range for the first time this year with setbacks in PADDs 2 & 5. PADD 2’s 315kbd Marathon Catlettsburg refinery went down with a power outage a couple weeks back which is the likely main culprit in this big reduction, and the relative strength we’ve seen in Chicago basis values lately. The big drop in PADD 5 run rates are likely a combination of the ongoing shutdown of Valero’s Benicia plant and the power outage at the PBF Torrance refinery.

Diesel stocks posted a small build despite the sharp drop in demand as the winter-storm-induced spike came to an end. Imports shot up above their 5-year range, but exports followed for a minimal net impact. PADDs 1 & 2 are still well below seasonal norms while PADD 3 remains at the high end of the seasonal range. PADD 4 posted a new seasonal 5-year high while PADD 5 traditional diesel stocks added almost a million barrels, bouncing off a seasonal low last week to just a couple hundred thousand barrels shy of the 5-year average this week.

Gasoline demand held steady last week but increased imports and decreased exports were wiped out by a decline in production. PADD 5 stocks are hanging about a million barrels under their 5-year average and PADD 1 is right in line with theirs. However, the middle of the country remains flush with product, keeping total U.S. stocks about 8 million barrels over the seasonal 5-year average.

Latest Posts

Energy Markets End A Wild Week With More Questions Than Answers

Middle East Tensions And Russian Export Ban Rock Energy Markets

Week 27 - US DOE Inventory Recap

Energy Markets Face Growing Uncertainty As Conflicts Threaten Oil Flows

Bullish Fundamentals Clash With Bearish Speculation In Global Oil Markets

Gasoline And Diesel Rally Despite Lower Crude Prices

Social Media

News & Views

View All

Energy Markets End A Wild Week With More Questions Than Answers

Middle East Tensions And Russian Export Ban Rock Energy Markets