Ceasefire Relief Fuels Equity Rally And Historic Energy Market Reversal

A 2 week cease fire agreement was announced Tuesday night, sparking one of the top 3 sell-offs in history for energy markets.

Refined products are off sharply on the day with ULSD futures leading the slide down around 80 cents/gallon, while RBOB futures are down 40 cents, but both are still roughly $1/gallon above where they were before the war broke out. That remaining risk premium is a reminder that the vast majority of vessels still aren’t transiting the strait of Hormuz as the cease fire plans still need to trickle down to the folks launching the attacks.

There were still attacks reported in Kuwait and the UAE overnight well after the announcement, which the market currently seems to be shrugging off as a delay in communication due to the chaotic leadership structure within Iran, rather than an intentional breach of the ceasefire. An attack on an Iranian oil refinery is a little harder to explain given that it came hours after the announcement and Iran is using that attack as an excuse for its retaliation after the buzzer had sounded.

At this point, it seems like the 2 week cease fire will allow for the thousand or so ships that have been trapped around the Persian Gulf due to the war to get home, but it seems unlikely that vessel traffic that averaged around 130 large ships/day will resume normal operations until a long term plan is put in place. IF we have seen the last of the attacks for this war, the recovery for global fuel markets and supply chains will still likely take most of the year due to the widespread damage to export facilities and insurance premiums so critical to global trade.

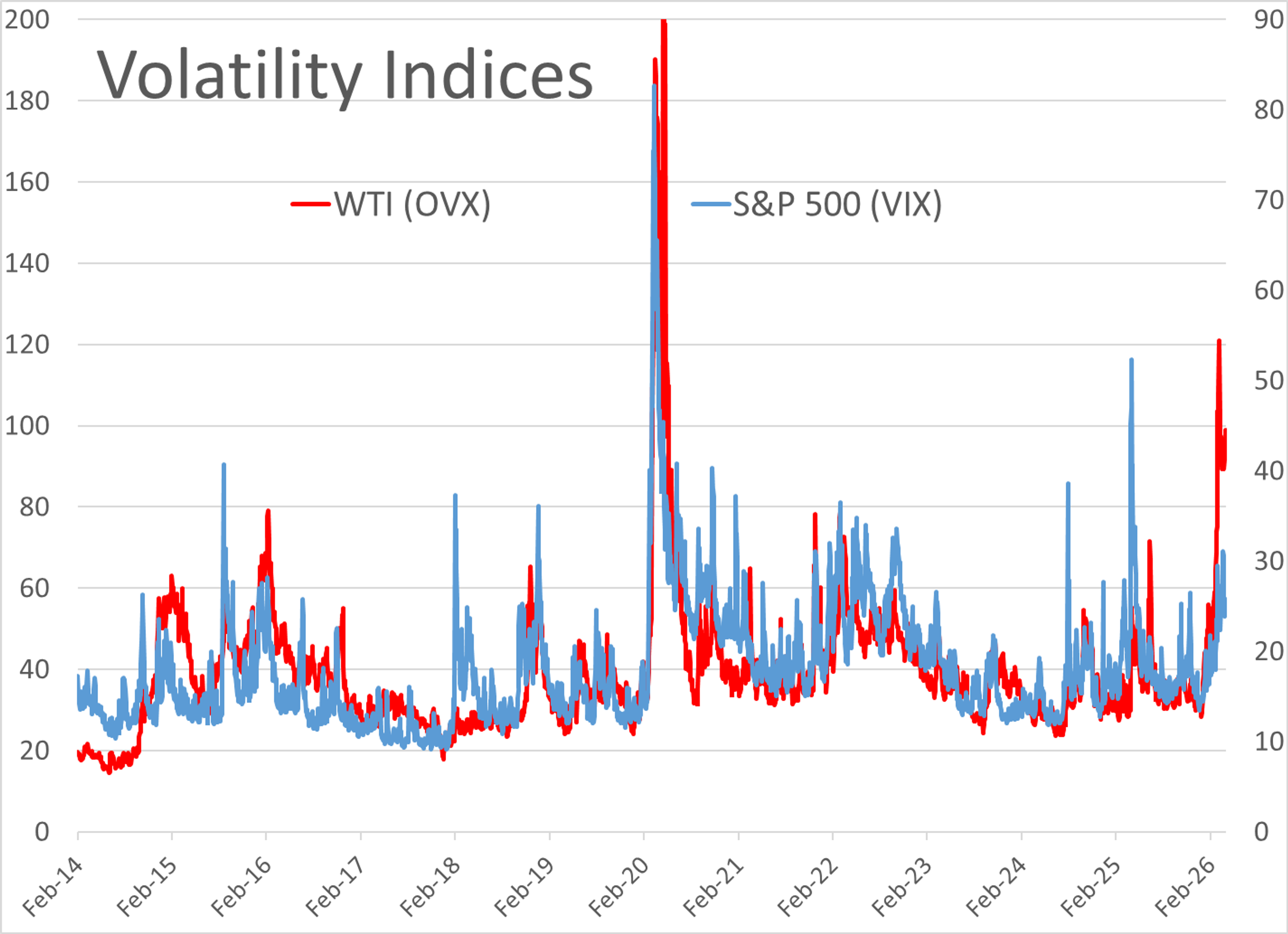

Equity and Energy markets have had a nearly perfect negative correlation since the war broke out, with increasing oil prices pushing stocks lower while today’s slide is coinciding with a huge rally in equity markets as the worst-case scenarios for the global economy and humanity in general seem to be off the table for now.

That’s a mean mean reversion: Even before the pullback in futures, we’ve already seen a sharp snapback in basis differentials in mid-continent markets with Chicago values surging to just a 5 cent discount to May futures Tuesday, after trading at a 70 cent discount last week. Ongoing maintenance at the 173mb/day P66 Wood River IL and the 253mb/day Marathon Robinson IL refineries has been cited for the rally, with the chaos in ULSD calendar spreads contributing heavily to the volatility in differentials as well. Group 3 ULSD remains the cheapest spot market in the country, but it has seen a huge recovery as well with differentials trading 25 cents under May Tuesday after trading at a dollar discount to April last week.

On the flip side, LA diesel basis values have been slipping from the record premiums we saw last week. Values are pegged around a 65 cent premium in LA vs 80 cents last week, while San Francisco spots are still talked closer to an 80 cent premium. Those huge premiums for CARB diesel are driving heavy discounting for Renewable Diesel as producers that survived a brutal 2025 are now racing to take advantage of the record margins made available by spiking diesel prices and RINs holding at 3 year highs. Cash trading is likely to be slim to nonexistent with the huge moves in futures today, but the slide on the board should encourage more reversion trading in basis diffs as well.

Latest Posts

Bullish Fundamentals Clash With Bearish Speculation In Global Oil Markets

Gasoline And Diesel Rally Despite Lower Crude Prices

Crude Retreats Ahead Of Holiday Weekend Despite Tight US Inventories

Gluts, Draws, And Disruptions: A Busy Start To July Energy Markets

Week 26 - US DOE Inventory Recap

Tight Inventories And Outages Push Diesel Prices Higher Into June Close

Social Media

News & Views

View All

Bullish Fundamentals Clash With Bearish Speculation In Global Oil Markets

Gasoline And Diesel Rally Despite Lower Crude Prices