Energy Markets Start The Week Torn Between Tight Supply And Peace Rumors

It’s a mixed bag for energy markets Monday morning, after another volatile Sunday night session that saw a $7 swing in oil prices and 27 cent swing for ULSD. After a weekend filled with dramatic headlines, energy markets started out the overnight session with more buying, only to see those gains wiped out this morning following more rumors of progress on a ceasefire deal.

OPEC & Friends agreed to increase their TARGET oil production rates by 206mb/day starting in May over the weekend. That target is even more theoretical than usual given that most of the countries in the 8 country agreement have been forced to dramatically cut back their output due to the wars in Iran and Ukraine. Even if the targeted increase happened in May, the 200mb/day equates to less than 2% of the net volume that’s not currently moving due to the wars.

Timing is everything: It was widely noted that WTI settled above Brent for the first time in years last week, but that headline is misleading as the prompt WTI contract is still a May timing, while Brent is already rolled to June. Comparing the two June contracts shows the waterborne Brent contract still commands a $12/barrel premium. A similar phenomenon is playing out in cash markets around the world as buyers are desperate to find physical barrels near term, and is a major reason why we’re seeing USGC diesel trade at a rare premium to ULSD futures, in addition to the record premiums for West Coast barrels.

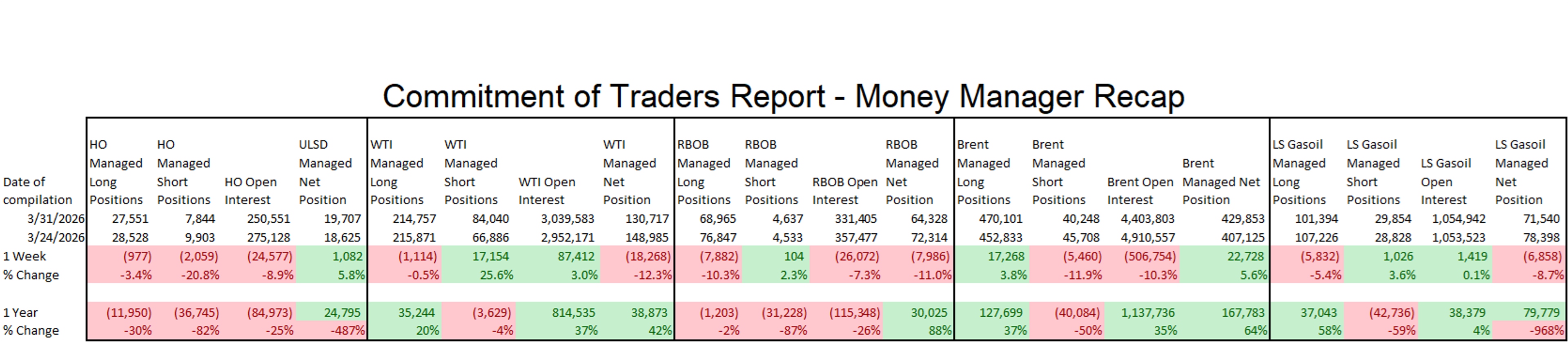

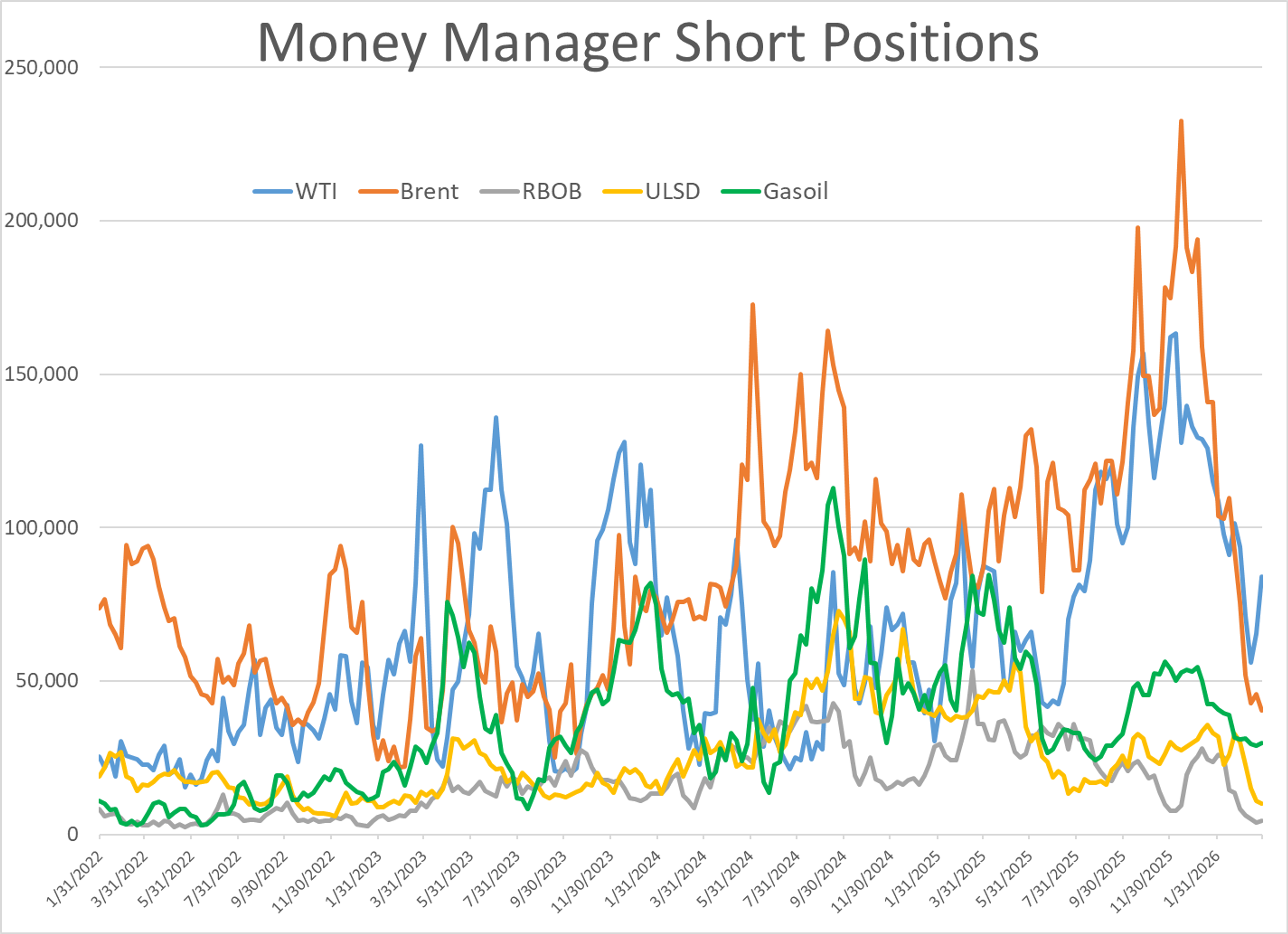

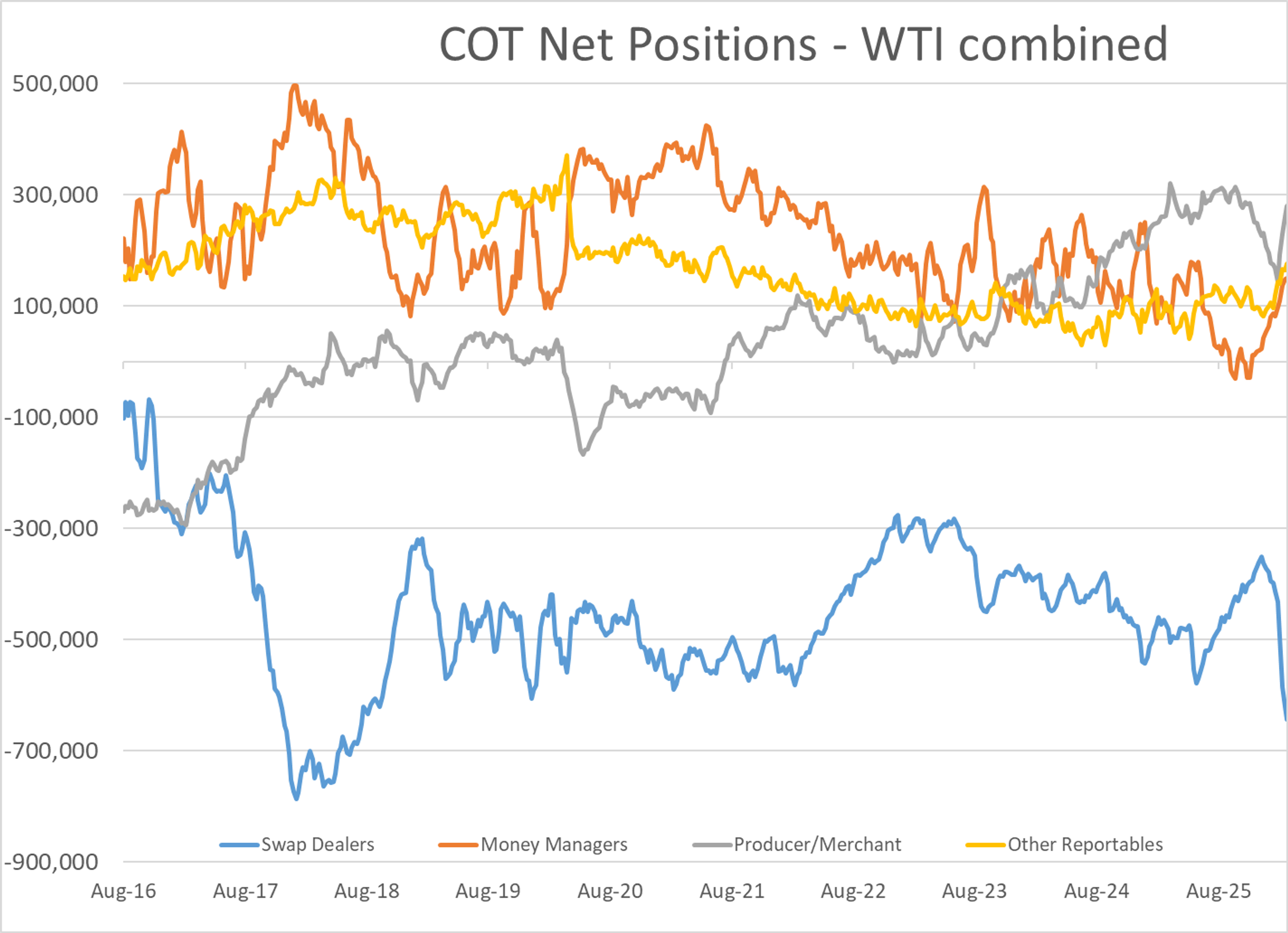

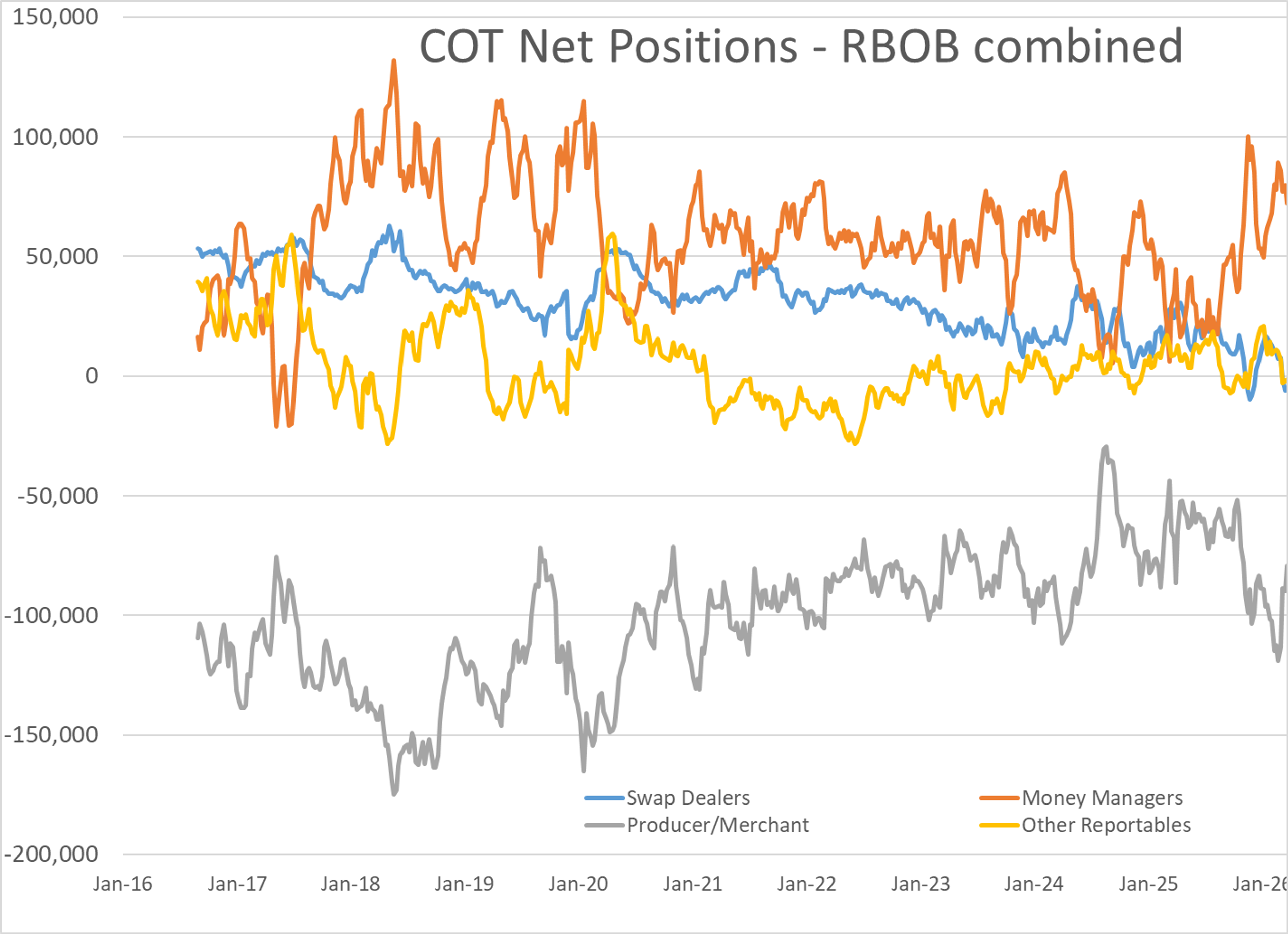

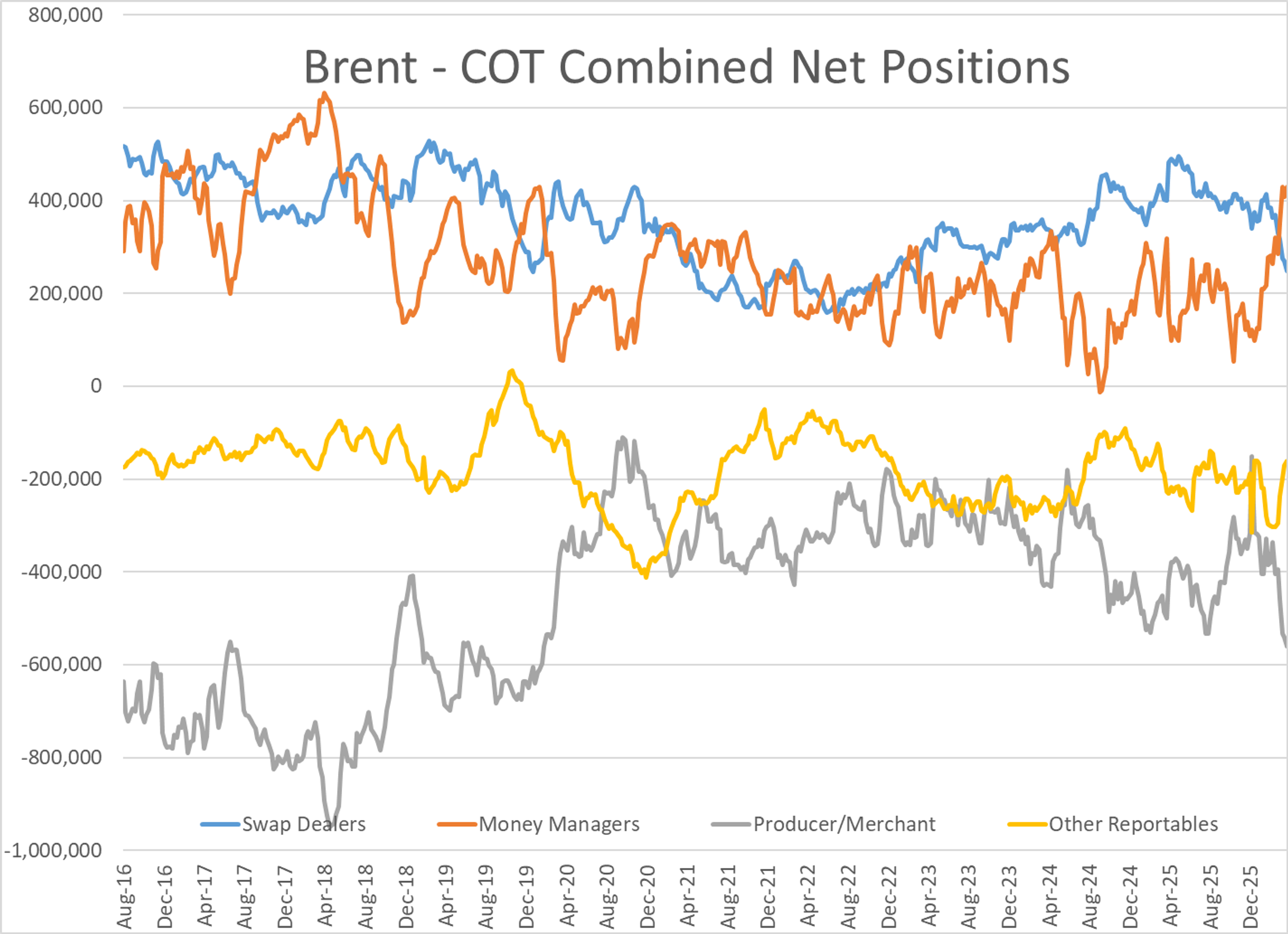

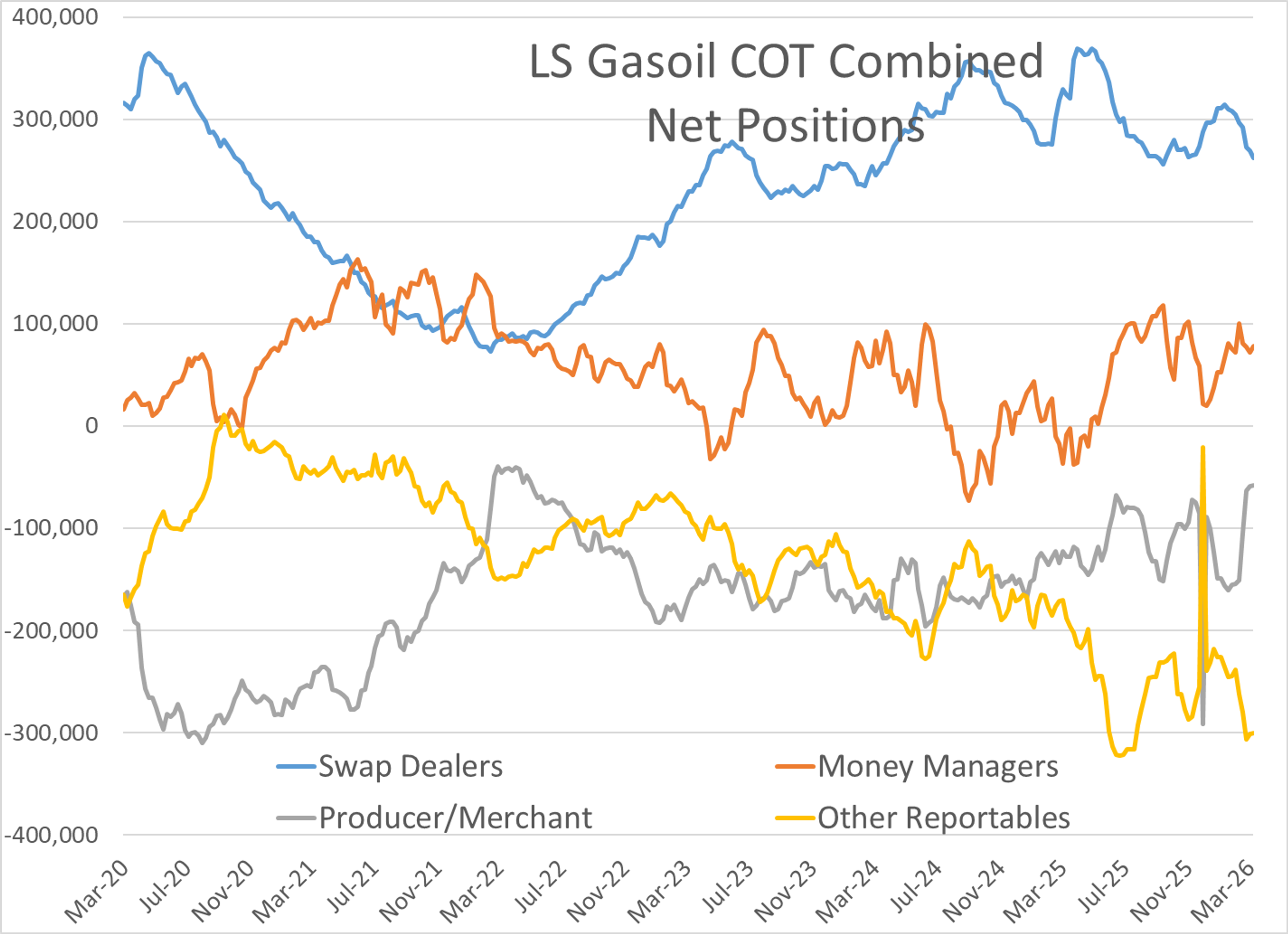

Money managers continue to have mixed reactions to the recent volatility. Last week’s CFTC report (with data as of Tuesday) showed decreases in large speculative length in WTI, RBOB and Gasoil contracts while Brent crude and ULSD contracts saw modest increases.

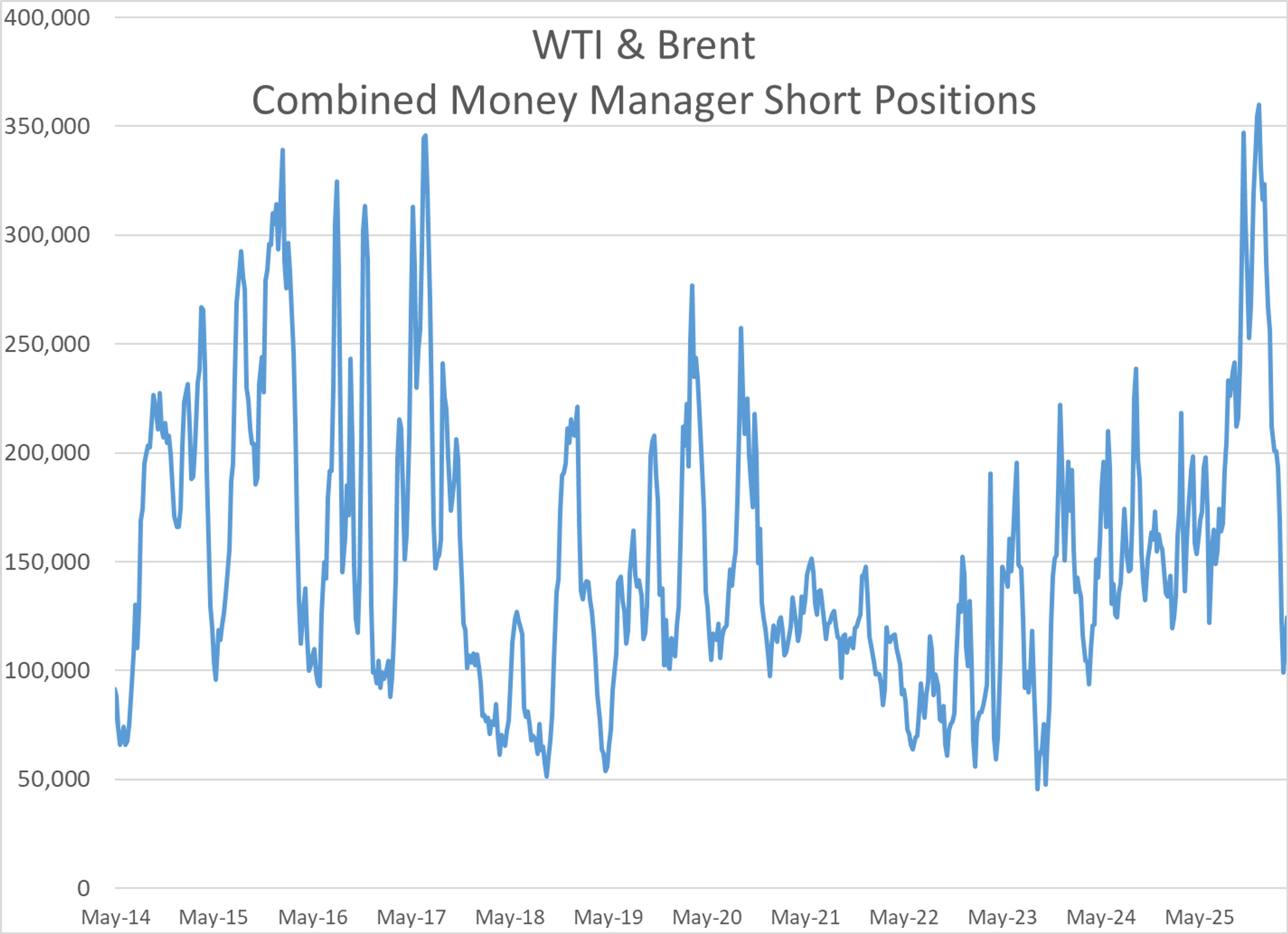

The total amount of large speculative money betting on higher Brent crude prices reached its highest level since January 2020 (before we knew what COVID was) last week, while open interest in the Brent contract surged to an all-time high.

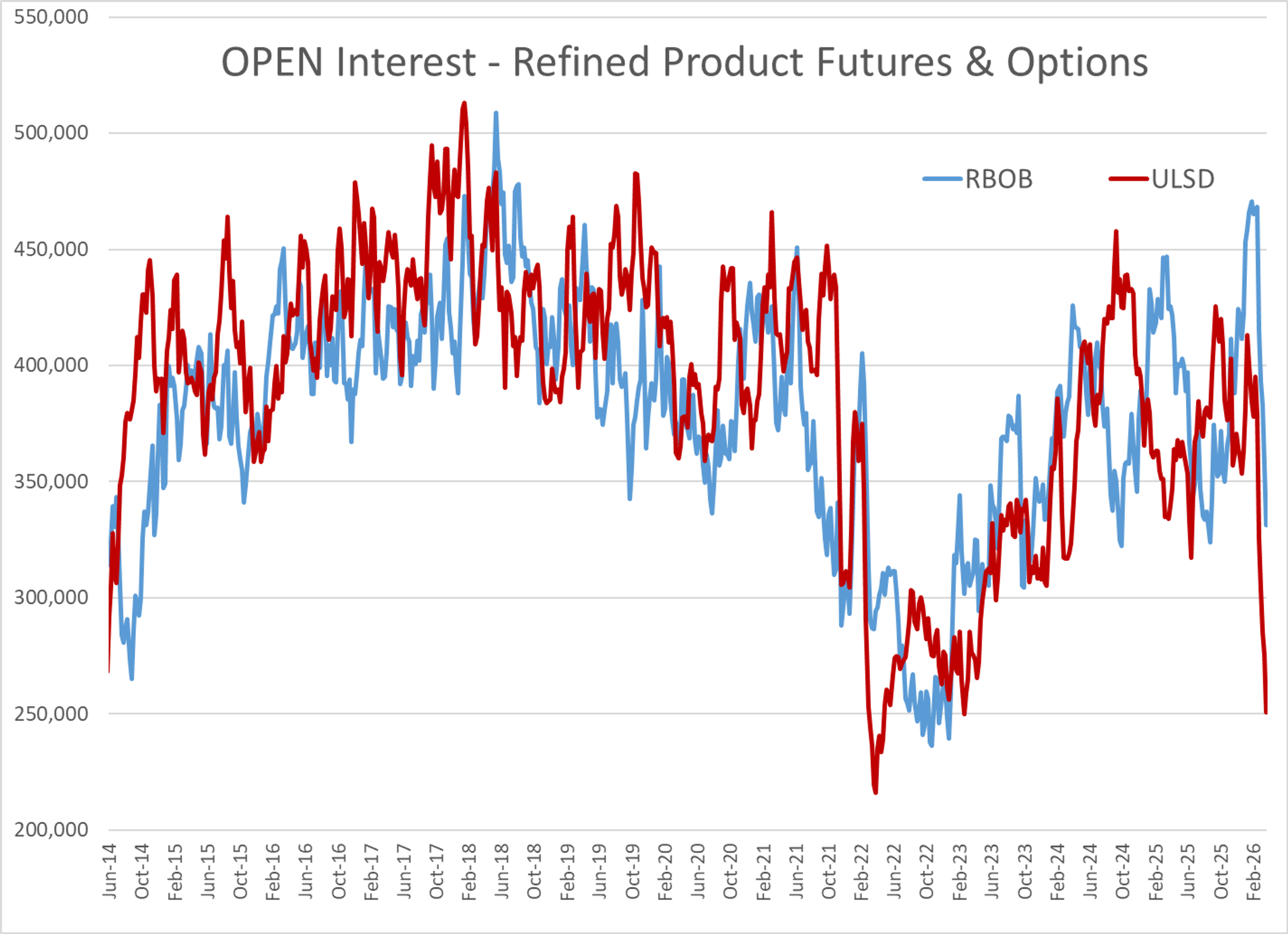

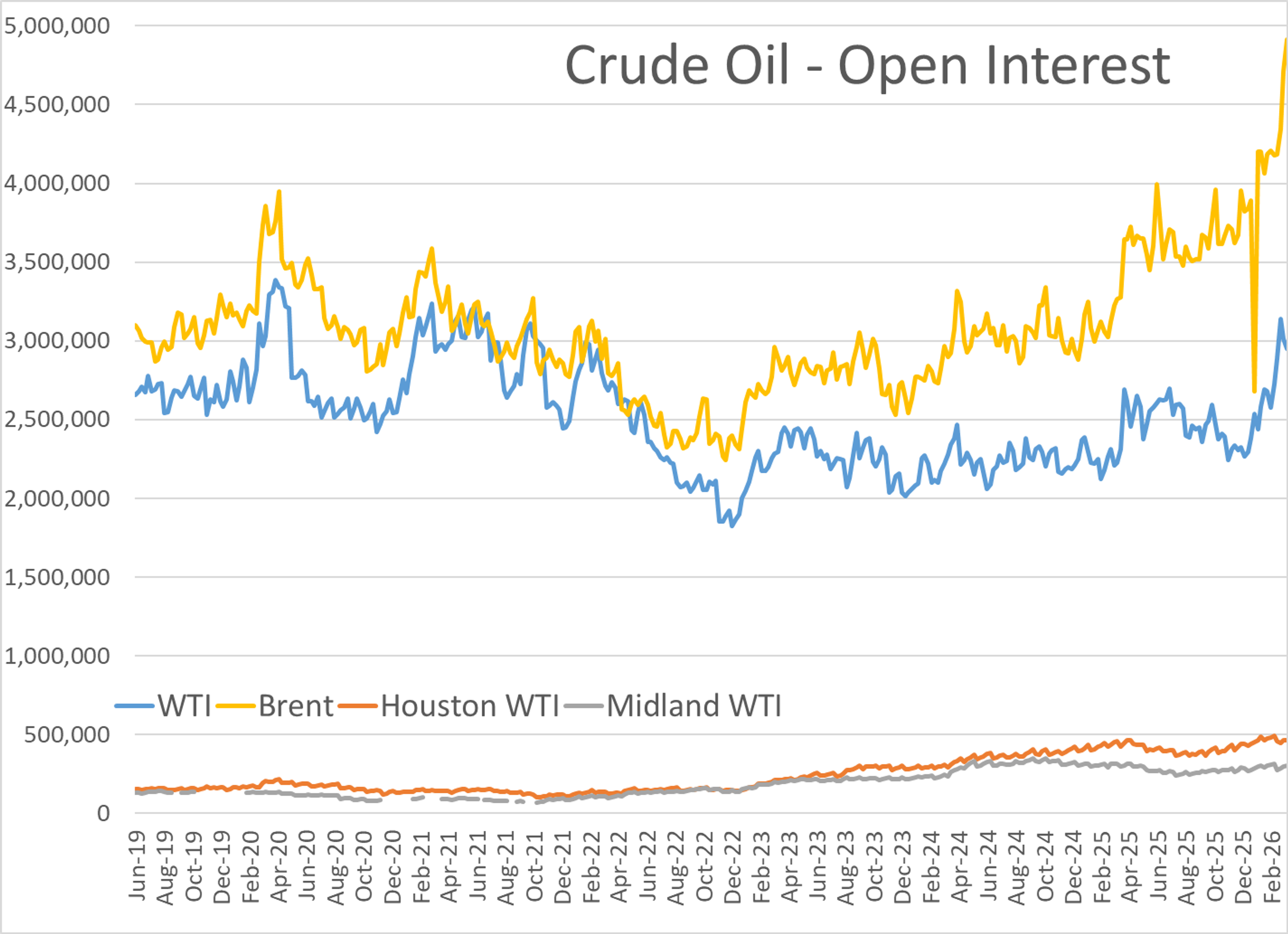

On the flip side, open interest in refined product futures and options has plummeted in recent weeks with total outstanding volumes in ULSD reaching a 3 year low as the CME’s huge increases in margin requirements ($17k/contract today vs $5k before the war) combines with steep backwardation to force some out of the market.

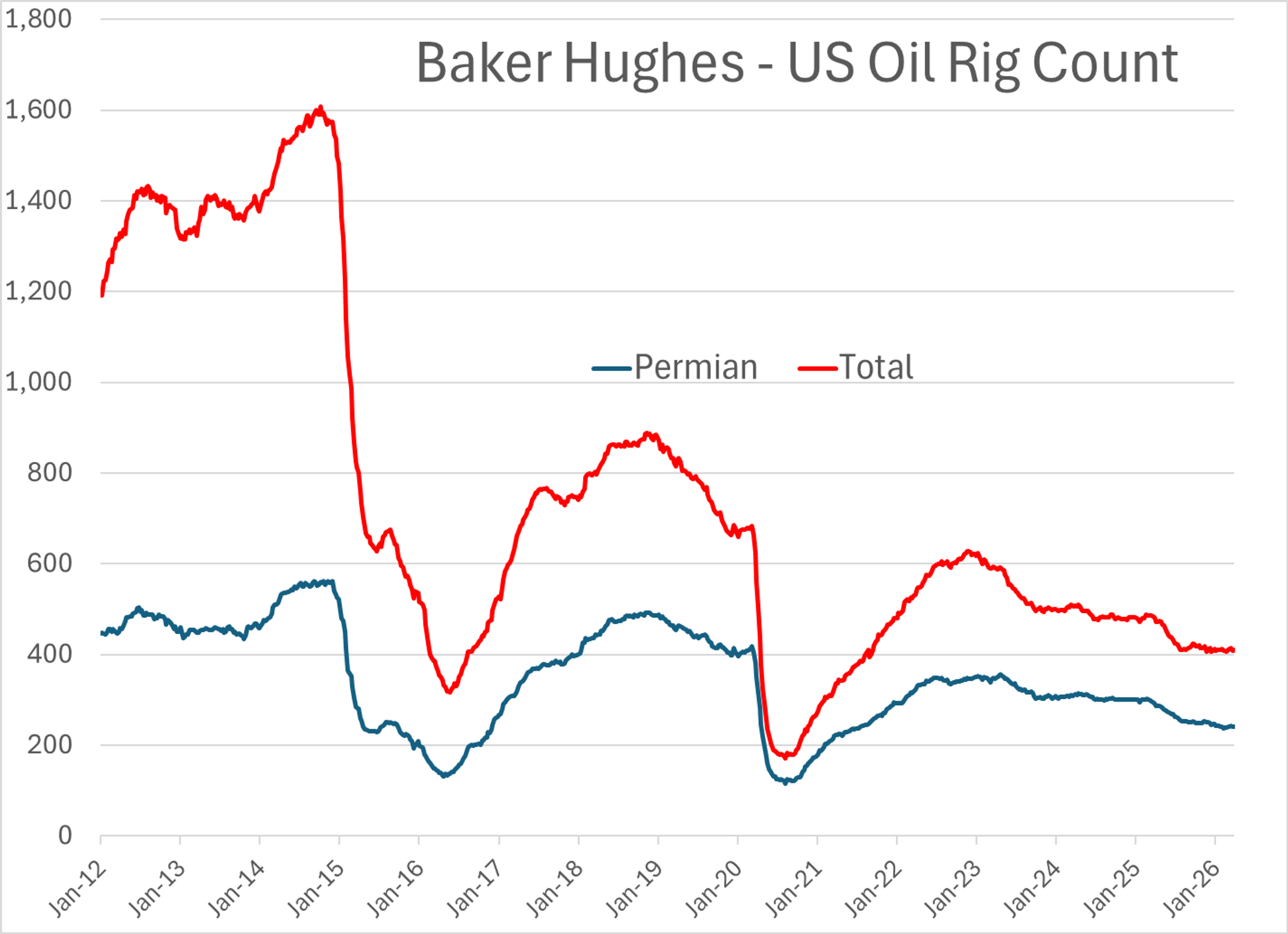

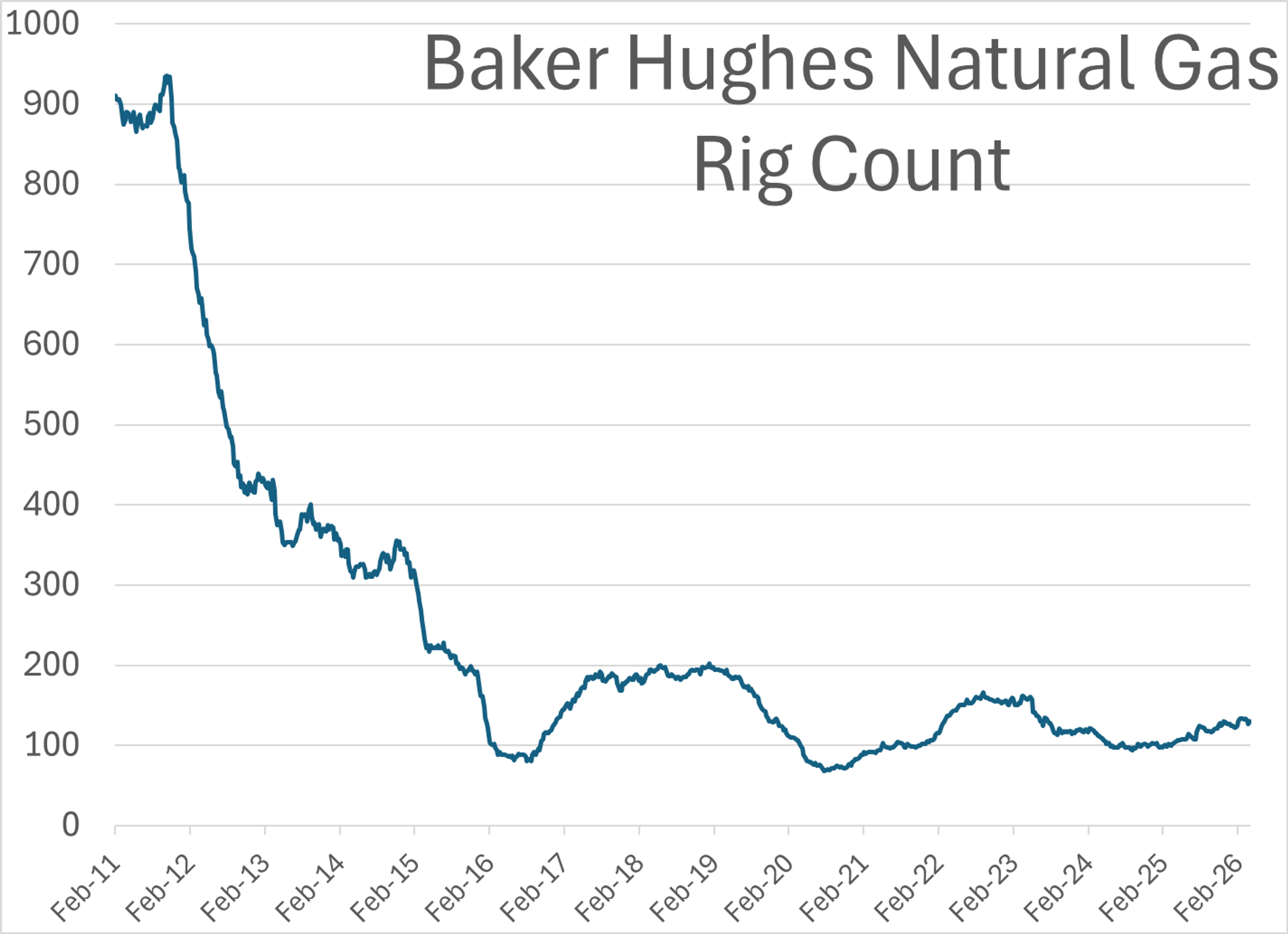

Baker Hughes reported an increase of 2 oil rigs and 3 natural gas rigs drilling in the U.S. last week.

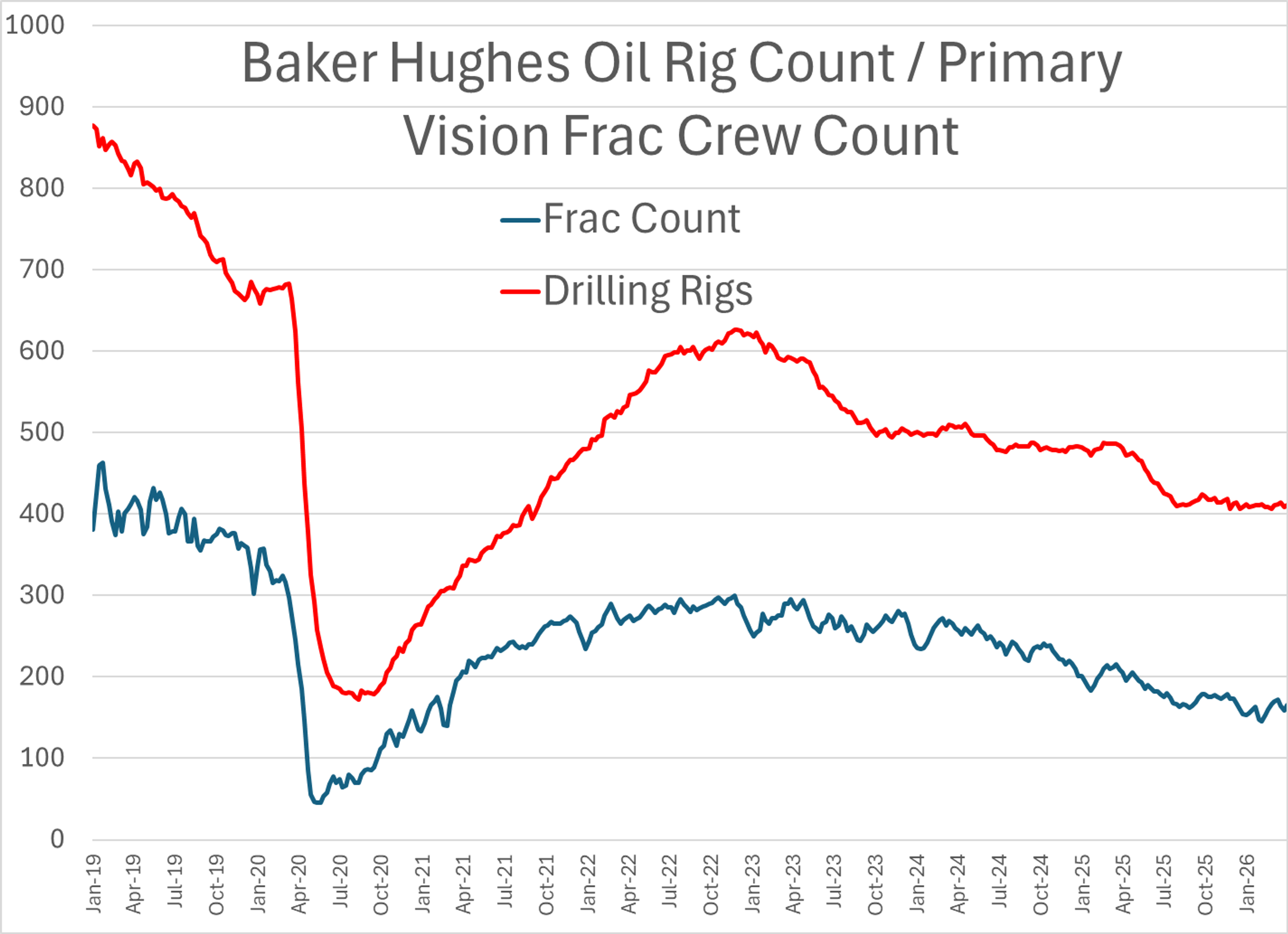

The Primary Vision count of active fracking crews increased by 7 last week, wiping out half of the losses seen in the previous two weeks.

Marathon reported Thursday it was planning a week’s worth of maintenance at the Carson section of its LA-area refining complex. That facility was rumored to have unplanned maintenance issues over the past two weeks that have contributed to the record rally in LA diesel basis values.

Freeport reported an upset at its LNG export facility that forced the shutdown of one of its processing trains over the weekend. The filing with the TCEQ said the unit was restarted after roughly 13 hours. While LNG exports don’t directly impact refined product markets, the world is increasingly clamoring for LNG supplies with 3 of the top 5 exporters (Qatar, Australia and Russia) all experiencing major disruptions in their supply capacity.

Latest Posts

Crude Retreats Ahead Of Holiday Weekend Despite Tight US Inventories

Gluts, Draws, And Disruptions: A Busy Start To July Energy Markets

Week 26 - US DOE Inventory Recap

Tight Inventories And Outages Push Diesel Prices Higher Into June Close

Oil Climbs On Strait Tensions As Cracks Emerge Beneath The Surface

Energy Prices Reverse As Market Shrugs Off Tanker Attack, Focus Shifts To Supply Constraints

Social Media

News & Views

View All

Crude Retreats Ahead Of Holiday Weekend Despite Tight US Inventories

Gluts, Draws, And Disruptions: A Busy Start To July Energy Markets