War on Oil? Markets Test The Edge As Supply Risks Mount

War on?

Energy markets were moving modestly lower overnight as the latest exchange of strikes between the U.S. and Iran seemed to be held in check, but have since bounced to modest gains as the U.S. President once again used his social media platform to levy new threats, and suggest more attacks may be coming. This week’s action may prove pivotal as crude and products are testing 3 month lows, with charts suggesting we could see a heavy wave if support near current levels doesn’t hold.

If you’re hoping for lower prices, you can point to Saudi Arabia lowering its price to Asian buyers for a 2nd straight month as demand declines, and reports that traffic through the Strait of Hormuz is actually higher than previously estimated due to numerous ships transiting with their transponders turned off.

If you’re one of many that think the pullback is overdone, you’ll note that Saudi Arabian crude premiums to Asian remain near their highest levels in a decade despite the modest decreases the past 2 months, and that shipping rates through the Strait of Hormuz are still less than 10% of normal, even if you believe the more lofty estimates.

One thing is for sure, the recent pullback in prices coinciding with the record run-up in RIN values has cut into refinery margins in a big way (the RVO is now taking out nearly $16/barrel for domestic production) even as most of the world is still desperate for their output.

Nothing to see here: The API estimated another large drop of 9.1 million barrels of commercial inventories drawn down, despite 7.9 million barrels of oil released from the SPR on the week. Gasoline inventories were estimated to drop by 1.2 million barrels, while distillates increased by 1.3 million barrels. The DOE’s weekly report is due out at its normal time this morning.

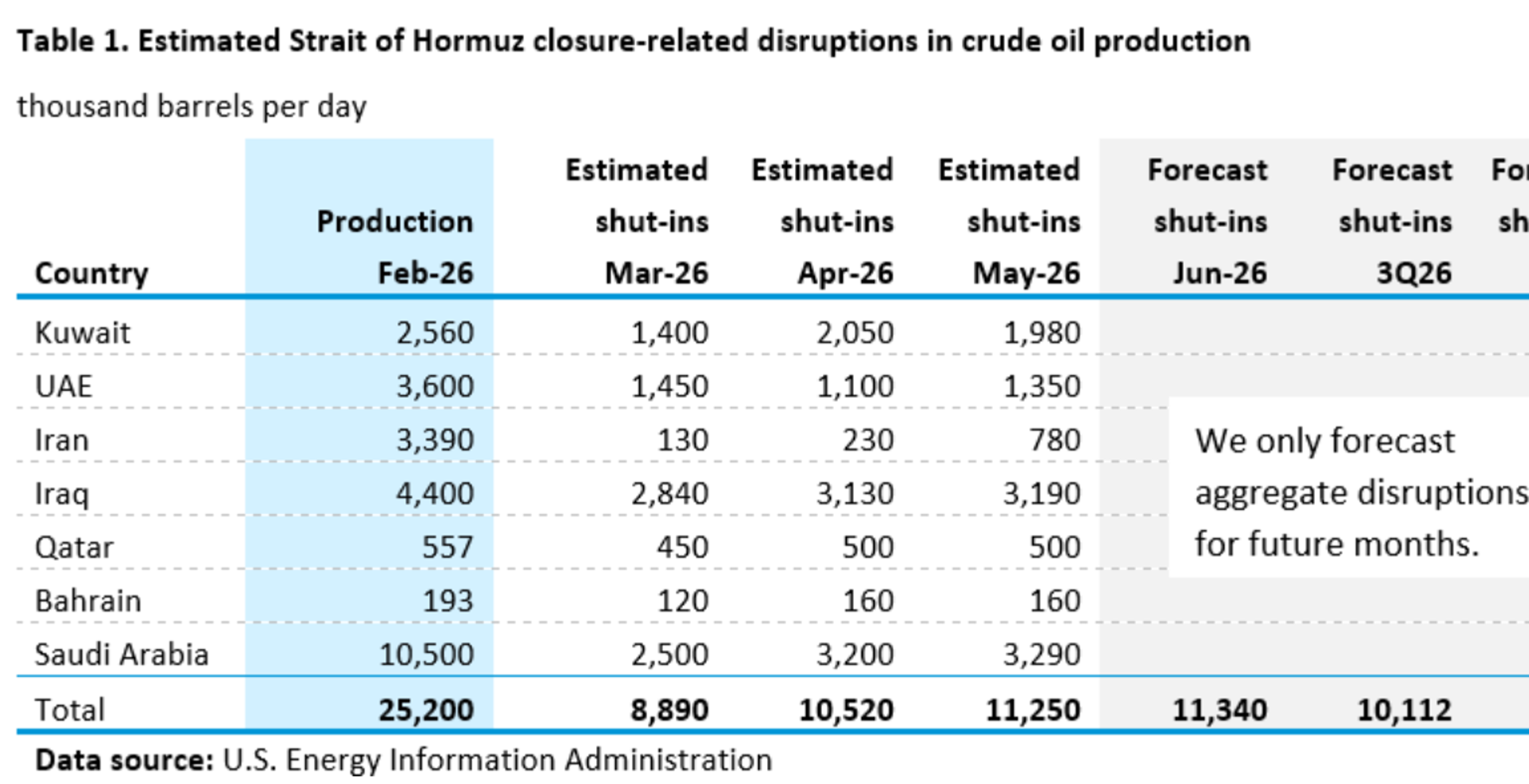

Yesterday the DOE/EIA made a big shift in its outlook for Hormuz in the latest Short Term Energy Outlook, changing its assumption to the Strait remaining “effectively closed in the near term” after multiple forecasts that predicted the strait would open in about a month. The report now suggests that we are unlikely to see traffic get back near normal levels until early 2027. The agency also made a big shift on its demand outlook, changing from previous reports that expected oil demand to continue to grow globally this year to a 1.1 million barrel decrease in consumption, roughly 1% of the global total, as consumers are forced to cut back due to the supply shock.

The EIA expects U.S. oil production to grow to new all-time highs next year and predicts that record petroleum exports from the U.S. will continue in 2026 before easing in 2027. LNG Exports are also forecast to continue their rapid growth as new facilities come online through 2027, but U.S. natural gas prices are predicted to stay relatively muted in the $3.50 range as domestic production continues to grow, thanks in large part to the increase in crude output.

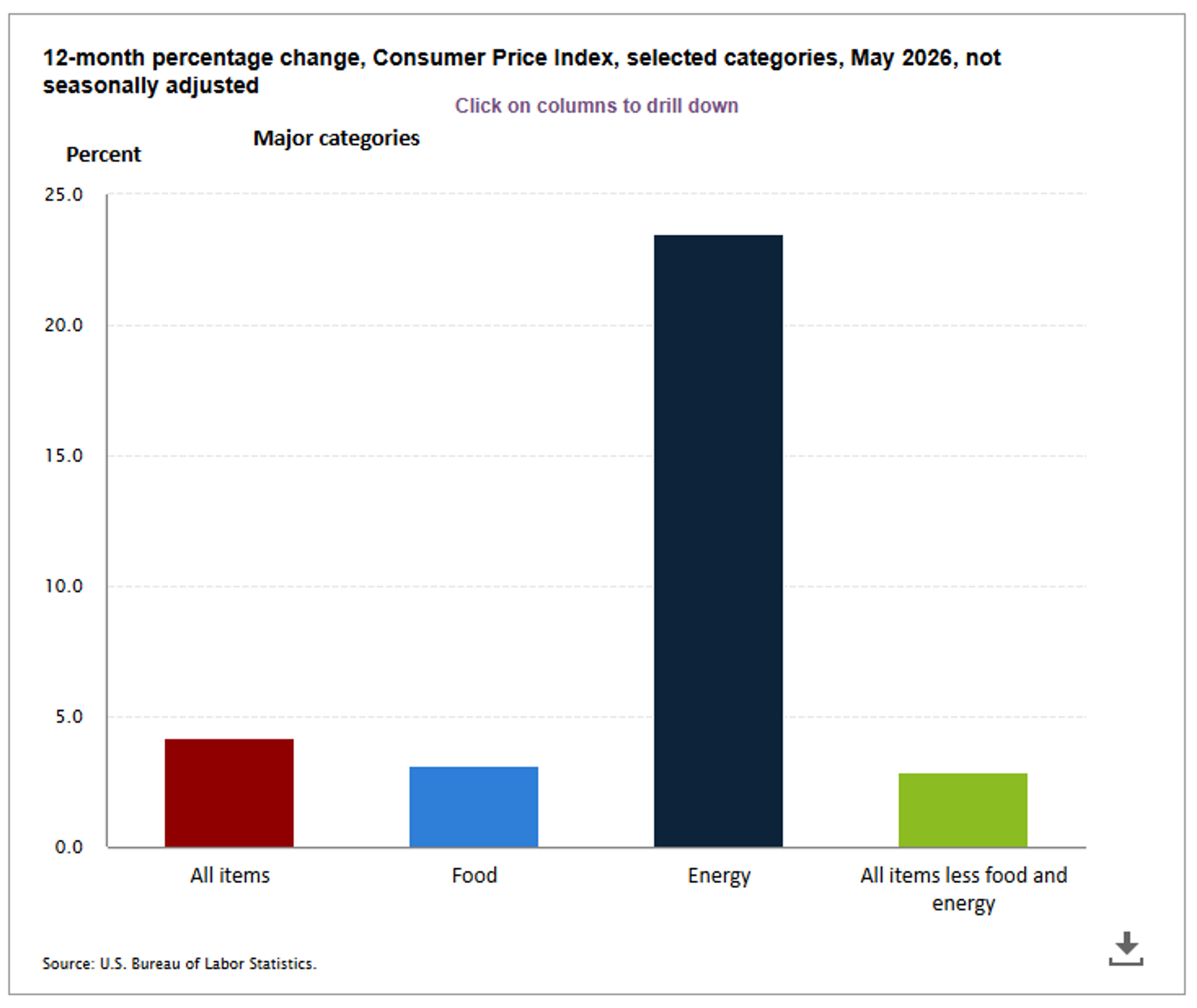

The May CPI report highlighted what you probably already knew: sharply higher gasoline and diesel prices are driving inflation higher across the country, but also noted what those who want lower interest rates don’t want to hear: it’s not just food and energy prices that are holding well above the FED’s 2% inflation target. A 59% year on year increase in Fuel Oil prices and a 40% increase in gasoline prices were the key drivers of CPI increasing by 4.2% over the past 12 months, but all items less food and energy remained stubbornly high at 2.9%.

Latest Posts

Energy Futures Cool Off Despite Mounting Geopolitical Uncertainty

Supply Risks Return To Center Stage As Crude Prices Accelerate

Week 29- US DOE Inventory Recap

Fuel Markets Tighten Despite Stable Crude Supply

Week 29- US DOE Inventory Recap

Markets Climb As War And Weather Test Global Fuel Supplies

Social Media

News & Views

View All

Energy Futures Cool Off Despite Mounting Geopolitical Uncertainty

Supply Risks Return To Center Stage As Crude Prices Accelerate