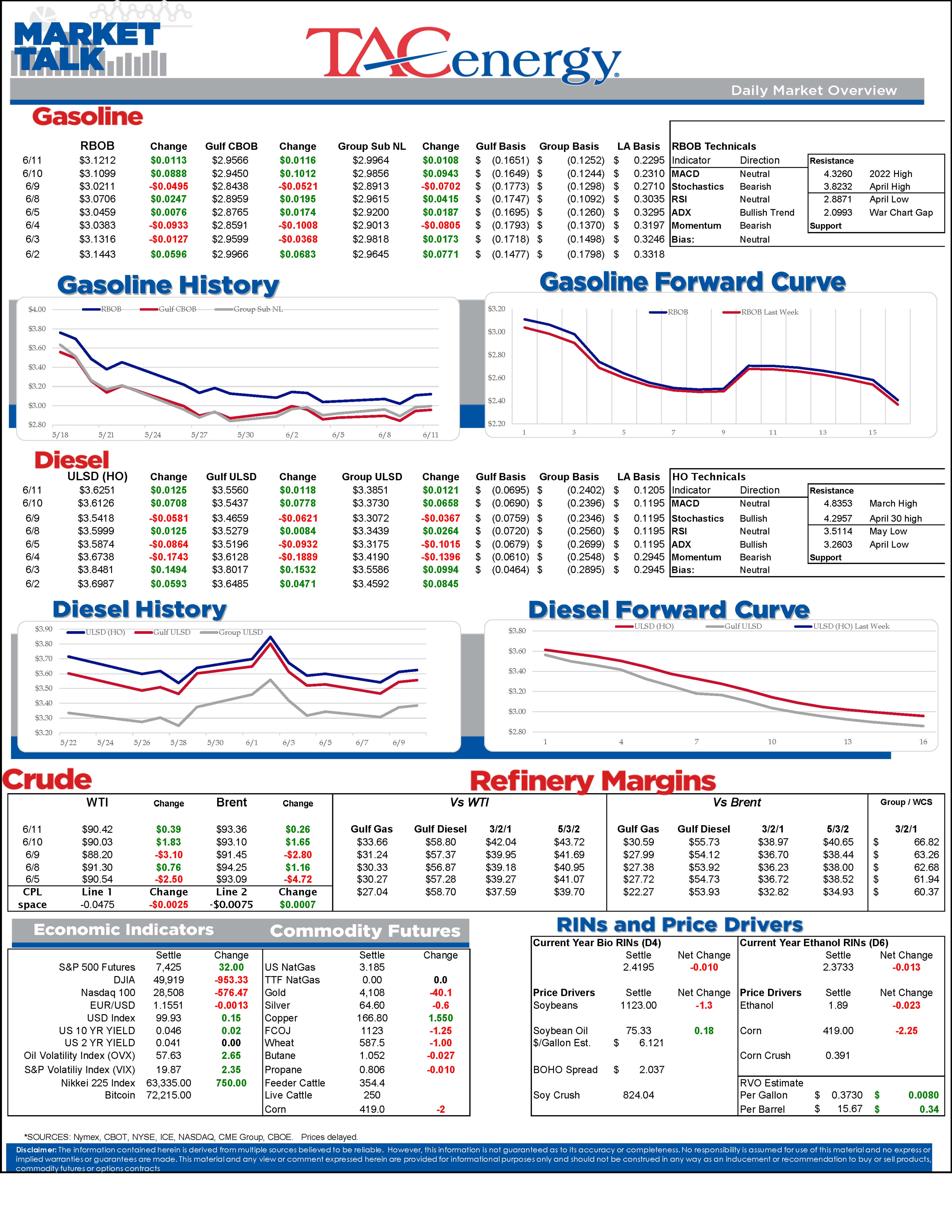

Draws, Disruptions, And A Market That Won’t Break

Energy futures opened modestly higher yesterday before extending gains after the U.S. President threatened to attack Iran again. The rally later cooled on reports the U.S. military “secretly” helped ships transit over 100 million barrels of crude through the Strait last month, with refined products and WTI ultimately settling 2-3% higher on the day. Prices held overnight despite continued military exchanges with gas, diesel, and crude each up less than .5% this morning indicating traders have the potential for ongoing conflict priced into their risk premiums.

OPEC's June Monthly Oil Market Report is out and once again manages to cover the global oil market without mentioning the Strait of Hormuz. The cartel did acknowledge actual production numbers falling roughly 9 million barrels/day below pre-conflict levels, a figure the report attributes to "continued disruptions to crude supply flows" without elaborating further. The group also trimmed its world demand growth forecast for the second straight month, down to 970 mb/day, still well above the EIA and IEA, both of which now expect demand to decline outright this year, leaving OPEC alone among major forecasters in expecting any growth at all.

In less meaningful news: Kpler data shows the first crude carrier since March 1st transited the Strait of Hormuz headed for Europe. The 100+ tankers that have exited the Gulf since the war began — less than a single day's worth of pre-war traffic — went almost entirely to Asia or stayed in the Middle East. While one tanker heading west for the first time in over 3 months is noteworthy, with attacks heating back up (and a $2 million Bitcoin toll for passage), it may prove to be more of an anomaly than a trend.

Human analysis of the DOE weekly report below. AI Analysis is attached along with the weekly charts.

Commercial crude stocks drew for the 7th consecutive week with each PADD now holding below average storage, even with production levels ticking higher. The SPR balance slipped below its 5-year seasonal range to just a couple million barrels over the 40-year lows seen 3 years ago. Imports dropped back below the 5-year range, but exports fell further, although still at seasonal highs. That net increase was wiped away by strong demand for refined products and a large negative balance adjustment.

Refinery runs slowed in PADD 3 but picked up elsewhere for a net increase. PADD 2 popped to a seasonal high with P66’s Ponca City plant returning to planned rates. PADD 5 is still well below its seasonal range, having shut two refineries recently, but PBF Torrance returned from planned maintenance and P66 Ferndale initiated a restart on Friday, which helps explain the falling basis levels in LA and SF over the past week. The total utilization rate hit a 2026 high and U.S. run rates, while lagging behind the previous two years’ seasonal levels, are still at the higher end of the 5-year range.

Diesel stocks declined slightly with the net positive effect of import/exports flows being negated by demand kicking up to a seasonal high. All PADDs are below their 5-year ranges except 2, which is only 165,000 barrels over the seasonal low set last year, with the total country spending a 7th straight week under its 5-year range.

Total gasoline stocks also hit a 7th week running under the 5-year range as increased production was met with an uptick in demand and exports surging to a 2026 high. PADD 4 crept above its 5-year average but is still well below the past two years like all other regions. PADDs 3 & 5 are hanging under their 5-year ranges with PADD 3 sitting ~7 million barrels below average as we head into the driving season.

Despite imports nosediving while exports remain elevated, jet stocks continue to set fresh seasonal highs with U.S. production levels hitting an all-time high last week.

Latest Posts

Energy Futures Cool Off Despite Mounting Geopolitical Uncertainty

Supply Risks Return To Center Stage As Crude Prices Accelerate

Week 29- US DOE Inventory Recap

Fuel Markets Tighten Despite Stable Crude Supply

Week 29- US DOE Inventory Recap

Markets Climb As War And Weather Test Global Fuel Supplies

Social Media

News & Views

View All

Energy Futures Cool Off Despite Mounting Geopolitical Uncertainty

Supply Risks Return To Center Stage As Crude Prices Accelerate